You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Discharge of ContractDocument13 pagesDischarge of Contractspark_123100% (4)

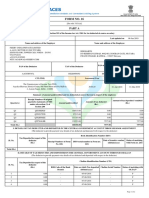

- Form16 Fiserv 2018-19Document8 pagesForm16 Fiserv 2018-19SiddharthNo ratings yet

- Policy On Performance EvaluationDocument5 pagesPolicy On Performance EvaluationSathish Haran100% (1)

- The Five Generic Competitive StrategiesDocument20 pagesThe Five Generic Competitive Strategiesspark_123100% (8)

- Quasi ContractsDocument9 pagesQuasi Contractsspark_123100% (4)

- PQP Vs ISO 9001 Clauses List PDFDocument1 pagePQP Vs ISO 9001 Clauses List PDFVpln Sarma100% (1)

- Full Operations Management 6Th Edition Test Bank Nigel Slack PDF Docx Full Chapter ChapterDocument23 pagesFull Operations Management 6Th Edition Test Bank Nigel Slack PDF Docx Full Chapter Chaptersuavefiltermyr62100% (28)

- External EnvironmentDocument16 pagesExternal Environmentspark_12380% (5)

- Presented By:: Varun Viral Milan Paresh KiritDocument15 pagesPresented By:: Varun Viral Milan Paresh Kiritspark_123No ratings yet

- 12-Mother Teresa BiographtDocument65 pages12-Mother Teresa Biographtspark_123100% (2)

- Transfer of PropertyDocument8 pagesTransfer of Propertyspark_123100% (3)

- Sale of Goods Act, 1930Document15 pagesSale of Goods Act, 1930spark_123100% (7)

- Cement Industry AnalysisDocument55 pagesCement Industry Analysisspark_12396% (54)

- Final TrusteeshipDocument9 pagesFinal Trusteeshipspark_123100% (4)

- Performance of ContractDocument18 pagesPerformance of Contractspark_123100% (6)

- Contingent Contracts-7Document8 pagesContingent Contracts-7spark_123100% (2)

- Sale of Goods Act, 1930Document15 pagesSale of Goods Act, 1930spark_123100% (7)

- The Indian Contract Act, 1872Document20 pagesThe Indian Contract Act, 1872spark_123100% (14)

- CH 03 EXIM POLICY OF INDIADocument20 pagesCH 03 EXIM POLICY OF INDIAspark_12395% (19)

- Aggregations of Manufacturing Based On NACE Rev. 2Document3 pagesAggregations of Manufacturing Based On NACE Rev. 2xdjqjfrxhiivnpNo ratings yet

- Design and Construction of Offshore Concrete Structures: February 2017Document18 pagesDesign and Construction of Offshore Concrete Structures: February 2017Suraj PandeyNo ratings yet

- Effectiveness of Social Media As A Marketing Tool An Empirical StudyDocument9 pagesEffectiveness of Social Media As A Marketing Tool An Empirical StudyJamila Mesha Bautista OrdonezNo ratings yet

- Corpo CasesDocument172 pagesCorpo CasesAliya DulanasNo ratings yet

- Overheads Test (Q)Document13 pagesOverheads Test (Q)Rabia SattarNo ratings yet

- New CORPORATE INTERNSHIP PROJECT REPORT-2 PDFDocument82 pagesNew CORPORATE INTERNSHIP PROJECT REPORT-2 PDFAshok KumarNo ratings yet

- FAP - Jul 2010 - West DownloadDocument79 pagesFAP - Jul 2010 - West Downloadsandip rajpuraNo ratings yet

- Rivera Vs EspirituDocument4 pagesRivera Vs EspirituChingNo ratings yet

- Jawaharlal Nehru Technological University Hyderabad 13mba22 EntrepreneurshipDocument20 pagesJawaharlal Nehru Technological University Hyderabad 13mba22 Entrepreneurshipmba betaNo ratings yet

- Social Entrepreneurship NotesDocument6 pagesSocial Entrepreneurship NotesVeronica BalisiNo ratings yet

- Assignment of CBDocument5 pagesAssignment of CBJAIRAJ SINGH100% (1)

- RPF Contract 2024 FormDocument9 pagesRPF Contract 2024 Formmatimaintenance.npci2024No ratings yet

- Agency Program Coordinator GuideDocument42 pagesAgency Program Coordinator Guidenate mcgradyNo ratings yet

- Banking OmbudsmanDocument66 pagesBanking Ombudsmanmrchavan143No ratings yet

- 08 - Barretto Vs Santa MarinaDocument1 page08 - Barretto Vs Santa MarinaRia GabsNo ratings yet

- SSS CCL Aka PDFDocument18 pagesSSS CCL Aka PDFVikram VickyNo ratings yet

- OSHJ-CoP-01 Risk Management and Control Version 1 EnglishDocument15 pagesOSHJ-CoP-01 Risk Management and Control Version 1 EnglishsajinNo ratings yet

- Operations Management in The Supply Chain Decisions and Cases Schroeder 6th Edition Test BankDocument15 pagesOperations Management in The Supply Chain Decisions and Cases Schroeder 6th Edition Test BankBrent Theiler100% (35)

- Hire Purchase Law RevisedDocument46 pagesHire Purchase Law RevisedBilliee ButccherNo ratings yet

- Entertainment-City-Jan 2019 BRICKWORKDocument6 pagesEntertainment-City-Jan 2019 BRICKWORKPuneet367No ratings yet

- Business Ethics - Module 1Document16 pagesBusiness Ethics - Module 1Rekha Madhu100% (1)

- CH 07Document22 pagesCH 07amir nabilNo ratings yet

- Green Marketing Goes NegativeDocument8 pagesGreen Marketing Goes NegativeFrankNo ratings yet

- Chapter 3Document19 pagesChapter 3Shan P FamularNo ratings yet

- Accounting For Partnership: Basic ConceptsDocument51 pagesAccounting For Partnership: Basic ConceptsVijay ShekarNo ratings yet

- Data Analytics: This Study Resource Was Shared ViaDocument5 pagesData Analytics: This Study Resource Was Shared ViaAmeya SakpalNo ratings yet