You might also like

- Ucpb V Asgard FactsDocument4 pagesUcpb V Asgard FactsJUAN REINO CABITAC50% (2)

- Capacity To Buy and Sell Art 1489: Read: Mercado Vs EspirituDocument20 pagesCapacity To Buy and Sell Art 1489: Read: Mercado Vs EspirituJUAN REINO CABITACNo ratings yet

- Conditions and WarrantiesDocument11 pagesConditions and WarrantiesJUAN REINO CABITACNo ratings yet

- Smith Kline Beckman Co. V Court of Appeals and Tryco PharmaDocument2 pagesSmith Kline Beckman Co. V Court of Appeals and Tryco PharmaJUAN REINO CABITACNo ratings yet

- CANON KABUSHIKI KAISHA vs. COURT OF APPEALSDocument2 pagesCANON KABUSHIKI KAISHA vs. COURT OF APPEALSJUAN REINO CABITACNo ratings yet

- Good Faith Good Faith Option 1: Purchase Whatever Has Been Built, Planted, or Sown AfterDocument5 pagesGood Faith Good Faith Option 1: Purchase Whatever Has Been Built, Planted, or Sown AfterJUAN REINO CABITACNo ratings yet

- Romero Vs CaDocument12 pagesRomero Vs CaJUAN REINO CABITACNo ratings yet

- Mendoza Vs PeopleDocument2 pagesMendoza Vs PeopleJUAN REINO CABITACNo ratings yet

- Sof TAX 1 Case DigestsDocument18 pagesSof TAX 1 Case DigestsJUAN REINO CABITACNo ratings yet

- People V Tica, G.R. No. 222561Document2 pagesPeople V Tica, G.R. No. 222561JUAN REINO CABITACNo ratings yet

- FUDOT vs. CATTLEYA LAND, Inc., G.R. No. 171008Document1 pageFUDOT vs. CATTLEYA LAND, Inc., G.R. No. 171008JUAN REINO CABITACNo ratings yet

- MARQUEZ vs. DESIERTODocument2 pagesMARQUEZ vs. DESIERTOJUAN REINO CABITACNo ratings yet

- ONATE v. ABROGARDocument2 pagesONATE v. ABROGARJUAN REINO CABITACNo ratings yet

- MACION v. GUIANI - Complete DigestDocument2 pagesMACION v. GUIANI - Complete DigestJUAN REINO CABITACNo ratings yet

- Emilio Tan Et Al. v. Court of Appeals Et Al.Document2 pagesEmilio Tan Et Al. v. Court of Appeals Et Al.JUAN REINO CABITACNo ratings yet

- Makati Tuscany Condominium Corporation v. Court of AppealsDocument3 pagesMakati Tuscany Condominium Corporation v. Court of AppealsJUAN REINO CABITACNo ratings yet

- Pacific Timber Export Corporation v. Court of AppealsDocument3 pagesPacific Timber Export Corporation v. Court of AppealsJUAN REINO CABITACNo ratings yet

- DACANAY, Jr. vs. ASISTIO, G.R. No. 93654Document1 pageDACANAY, Jr. vs. ASISTIO, G.R. No. 93654JUAN REINO CABITACNo ratings yet

- Blue Cross Healthcare Inc. v. OlivaresDocument2 pagesBlue Cross Healthcare Inc. v. OlivaresJUAN REINO CABITACNo ratings yet

- Philippine Health Care Providers, Inc. v. Commissioner of Internal RevenueDocument3 pagesPhilippine Health Care Providers, Inc. v. Commissioner of Internal RevenueJUAN REINO CABITACNo ratings yet

- White Gold Marine Services, Inc. vs. Pioneer InsuranceDocument3 pagesWhite Gold Marine Services, Inc. vs. Pioneer InsuranceJUAN REINO CABITACNo ratings yet

- CANON KABUSHIKI KAISHA vs. COURT OF APPEALSDocument2 pagesCANON KABUSHIKI KAISHA vs. COURT OF APPEALSJUAN REINO CABITACNo ratings yet

- Labor Case DigestDocument9 pagesLabor Case DigestJUAN REINO CABITACNo ratings yet

- Fortune Medicare Inc. v. AmorinDocument3 pagesFortune Medicare Inc. v. AmorinJUAN REINO CABITACNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Cap1 PDFDocument2 pagesCap1 PDFtahlokoNo ratings yet

- 1 RGDGNDocument13 pages1 RGDGNRuth TenajerosNo ratings yet

- AAYUSHIDocument30 pagesAAYUSHIPushkar MahajanNo ratings yet

- ACC 211 Financial Accounting 1-Ekiti AdealuDocument63 pagesACC 211 Financial Accounting 1-Ekiti AdealuShehuNo ratings yet

- REA Mock Examination With Answer PDFDocument36 pagesREA Mock Examination With Answer PDFDionico O. Payo Jr.100% (2)

- The Kenya Gazette: Published by Authority of The Republic of KenyaDocument20 pagesThe Kenya Gazette: Published by Authority of The Republic of KenyaTony Ras MwangiNo ratings yet

- FL Con Law - Case BriefsDocument23 pagesFL Con Law - Case BriefsassiramufNo ratings yet

- Sales Notes Deposit in General and Its Different Kinds (Art 1962-1967)Document34 pagesSales Notes Deposit in General and Its Different Kinds (Art 1962-1967)LeeJongSuk isLife0% (1)

- PASDA Vs Dimayacyac (G.R. No. 220479 August 17, 2016)Document7 pagesPASDA Vs Dimayacyac (G.R. No. 220479 August 17, 2016)Ann ChanNo ratings yet

- Special Law For RegistrationDocument122 pagesSpecial Law For RegistrationRamesh BharadwajNo ratings yet

- 144 Guzman v. Bonnevie - DIGESTDocument2 pages144 Guzman v. Bonnevie - DIGESTAllen Windel Bernabe100% (1)

- Bellgrove V Eldridge - Michael FilippichDocument33 pagesBellgrove V Eldridge - Michael FilippichasdfajsdkflasjdfklasNo ratings yet

- 2011 Bar ExamDocument139 pages2011 Bar ExamLarry BugaringNo ratings yet

- Progressive Development Corporation vs. Quezon City, GR No. L-36081 Dated April 24, 1989Document5 pagesProgressive Development Corporation vs. Quezon City, GR No. L-36081 Dated April 24, 1989EdvangelineManaloRodriguezNo ratings yet

- Cap 123F - Building (Planning) RegulationsDocument131 pagesCap 123F - Building (Planning) RegulationsjesoneliteNo ratings yet

- TCCI Commercial AppDocument2 pagesTCCI Commercial AppSahba KamalianNo ratings yet

- Room Rental AgreementDocument7 pagesRoom Rental AgreementJeannina RadfordNo ratings yet

- Unlawful Detainer Reply Memo From Taliskier Corp., Vail Resorts in Lease Dispute Litigation With Park City Mountain Resort, April 14, 2014Document36 pagesUnlawful Detainer Reply Memo From Taliskier Corp., Vail Resorts in Lease Dispute Litigation With Park City Mountain Resort, April 14, 2014jasonblevins100% (1)

- (FT) Duremdes - v. - Duremdes20200212-1464-B6yy9Document11 pages(FT) Duremdes - v. - Duremdes20200212-1464-B6yy9Amiel Gian Mario ZapantaNo ratings yet

- Petitioners Vs Vs Respondents Ceferino Padua Law Office The Solicitor General Gonzalez Dimaguila GonzalesDocument9 pagesPetitioners Vs Vs Respondents Ceferino Padua Law Office The Solicitor General Gonzalez Dimaguila GonzalesGabrielle Anne EndonaNo ratings yet

- Document Tenders 201151233736970Document34 pagesDocument Tenders 201151233736970Nafiz JaberNo ratings yet

- Aca Brother Contract of Lease - Doc2Document6 pagesAca Brother Contract of Lease - Doc2Janice Gail BartolomeNo ratings yet

- RR 16-05Document32 pagesRR 16-05matinikki100% (1)

- Cases Ofor Business OrgDocument330 pagesCases Ofor Business OrgHazel Paguio-LastrolloNo ratings yet

- Sales - Cases (prt2)Document64 pagesSales - Cases (prt2)Cinja ShidoujiNo ratings yet

- Be It Enacted by The Senate and The House of Representatives of The Philippines in Congress AssembledDocument3 pagesBe It Enacted by The Senate and The House of Representatives of The Philippines in Congress Assembledkram kolNo ratings yet

- MSA 01 Summer 2022: Iq School of Finance Msa 1 by Sir Ibrahim Iqsf - PKDocument51 pagesMSA 01 Summer 2022: Iq School of Finance Msa 1 by Sir Ibrahim Iqsf - PKgohar azizNo ratings yet

- Agrarian CasesDocument100 pagesAgrarian CasesLorelieNo ratings yet

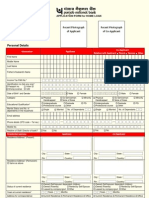

- 21-2012 PNB 1054 - Ann I - Application-Cum-Appraisal-Cum-Sanction For Housing LoanDocument9 pages21-2012 PNB 1054 - Ann I - Application-Cum-Appraisal-Cum-Sanction For Housing Loanrisk_j2546No ratings yet

- Os No. 3930 of 2020 Objections On IADocument4 pagesOs No. 3930 of 2020 Objections On IASameer NaveenaNo ratings yet