You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (843)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Customer Throughput Summary Report 02 Aug 2021 0524-08-22Document2,959 pagesCustomer Throughput Summary Report 02 Aug 2021 0524-08-22Raj Kothari M75% (4)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Investment Book of Record Competitive Advantage SimCorp PaperDocument14 pagesThe Investment Book of Record Competitive Advantage SimCorp PaperSecular SylhetNo ratings yet

- HL Case StudyDocument27 pagesHL Case StudyJorgeNo ratings yet

- Exam FM QuestioonsDocument102 pagesExam FM Questioonsnkfran100% (2)

- BetterSystemTrader UltimateGuideToTradingBooksDocument180 pagesBetterSystemTrader UltimateGuideToTradingBooksSebastianCalle91% (11)

- b2b PPT FinalDocument26 pagesb2b PPT FinalRaj Kothari MNo ratings yet

- Dual Axis Solar Panel ComponentsDocument11 pagesDual Axis Solar Panel ComponentsRaj Kothari MNo ratings yet

- Design Thinking: Final Presentation Presented By-Raj Kothari M Roll No. - K222Document9 pagesDesign Thinking: Final Presentation Presented By-Raj Kothari M Roll No. - K222Raj Kothari MNo ratings yet

- Cover Letter EYDocument1 pageCover Letter EYRaj Kothari MNo ratings yet

- Declaration For InternshipDocument1 pageDeclaration For InternshipRaj Kothari M100% (1)

- CV - Raj Kothari M 2020Document3 pagesCV - Raj Kothari M 2020Raj Kothari MNo ratings yet

- TanishqBagdi FinanceDocument1 pageTanishqBagdi FinanceRaj Kothari MNo ratings yet

- ShubhamGirishSorte FinanceDocument1 pageShubhamGirishSorte FinanceRaj Kothari MNo ratings yet

- MiteshBambhaniya FinanceDocument1 pageMiteshBambhaniya FinanceRaj Kothari MNo ratings yet

- RajKothariM FinanceDocument1 pageRajKothariM FinanceRaj Kothari MNo ratings yet

- ShivamUpadhyay FinanceDocument1 pageShivamUpadhyay FinanceRaj Kothari MNo ratings yet

- RamGupta FinanceDocument1 pageRamGupta FinanceRaj Kothari MNo ratings yet

- SarthakZaveri FinanceDocument1 pageSarthakZaveri FinanceRaj Kothari MNo ratings yet

- Ri NC 130320 000011Document12 pagesRi NC 130320 000011Raj Kothari MNo ratings yet

- PSB Note Aug'21Document18 pagesPSB Note Aug'21Raj Kothari MNo ratings yet

- PSL Wise Outstanding As On 31-07-21Document372 pagesPSL Wise Outstanding As On 31-07-21Raj Kothari MNo ratings yet

- PSB Note June'21Document30 pagesPSB Note June'21Raj Kothari MNo ratings yet

- Aut Hori Sati On LetterDocument15 pagesAut Hori Sati On LetterRaj Kothari MNo ratings yet

- Norton Homewares Inventory: Product Code Item Description Supplier DepartmentDocument7 pagesNorton Homewares Inventory: Product Code Item Description Supplier DepartmentAshutosh SharmaNo ratings yet

- SeareereDocument13 pagesSeareereRaj Kothari MNo ratings yet

- SVKM'S Nmims: Mukesh Patel School of Technology Management and EngineeringDocument22 pagesSVKM'S Nmims: Mukesh Patel School of Technology Management and EngineeringRaj Kothari MNo ratings yet

- FINMAR - Introduction To Financial Management and Financial MarketsDocument8 pagesFINMAR - Introduction To Financial Management and Financial MarketsLagcao Claire Ann M.No ratings yet

- Chapter 1 STOCKS 101Document4 pagesChapter 1 STOCKS 101Annadelle Dimatulac LeeNo ratings yet

- Ocean ManufacturingDocument5 pagesOcean ManufacturingАриунбаясгалан НоминтуулNo ratings yet

- Banking Awareness EbookDocument13 pagesBanking Awareness EbookPavan HebbarNo ratings yet

- From The President's Desk May - 2015: Private Circulation Only Issue - 96Document8 pagesFrom The President's Desk May - 2015: Private Circulation Only Issue - 96umeshNo ratings yet

- Dec 2002 - AnsDocument14 pagesDec 2002 - AnsHubbak KhanNo ratings yet

- All in One (Akshar)Document16 pagesAll in One (Akshar)tourist.happyexpatsNo ratings yet

- Chapter 2Document27 pagesChapter 2Mohamad SyafiqNo ratings yet

- DownloadDocument2 pagesDownloadNorlaily JohariNo ratings yet

- Consolidated Statement of Financial PositionDocument29 pagesConsolidated Statement of Financial PositionTinashe ZhouNo ratings yet

- Chapter 2 Financail Manegement Chapter II - FSA From Instructor 2024 3rd YearDocument37 pagesChapter 2 Financail Manegement Chapter II - FSA From Instructor 2024 3rd YearTarekegn DemiseNo ratings yet

- Group 2 - Jollibee Foods Corporation 2019 Financial ReportDocument15 pagesGroup 2 - Jollibee Foods Corporation 2019 Financial ReportVenziel Pedrosa0% (1)

- Inventories Quiz NotesDocument7 pagesInventories Quiz NotesMikaella Nicole PechardoNo ratings yet

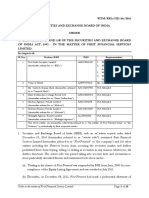

- Sl. No. Noticee/PAN PAN RepresentativesDocument18 pagesSl. No. Noticee/PAN PAN RepresentativesShyam SunderNo ratings yet

- Lecture 15 LevarageDocument50 pagesLecture 15 LevarageDevyansh GuptaNo ratings yet

- Tercera Práctica Calificada - Gestión de Inversiones I - 2019-1 - Preguntas y RespuestasDocument6 pagesTercera Práctica Calificada - Gestión de Inversiones I - 2019-1 - Preguntas y RespuestasMauricio La RosaNo ratings yet

- Bank Capital RegulationDocument57 pagesBank Capital RegulationAshenafiNo ratings yet

- Intermediate Accounting Stice Stice SkousenDocument58 pagesIntermediate Accounting Stice Stice SkousenTornike Jashi100% (1)

- Chapter 1: Overview of Financial Risk ManagmentDocument30 pagesChapter 1: Overview of Financial Risk ManagmentQuynh DangNo ratings yet

- Evolution of Derivatives Market in IndiaDocument4 pagesEvolution of Derivatives Market in IndiaSujeet GuptaNo ratings yet

- Bba Sem Iv All AssignmentDocument5 pagesBba Sem Iv All AssignmentYogeshNo ratings yet

- AFAR2 - Chapter 1 - Buscom OutlineDocument9 pagesAFAR2 - Chapter 1 - Buscom OutlineeiaNo ratings yet

- Wealth ManagementDocument4 pagesWealth ManagementvimmakNo ratings yet

- Assignment 1Document14 pagesAssignment 1Ibrar AnsarNo ratings yet

- Consolidation MCQSDocument7 pagesConsolidation MCQSvyom rajNo ratings yet

- Case Study FMDocument4 pagesCase Study FMasdeNo ratings yet