You might also like

- Easy Online Loans in The Philippines With Fast Approval - AllTheBestLoansDocument21 pagesEasy Online Loans in The Philippines With Fast Approval - AllTheBestLoansEddie C. Resurreccion Jr.No ratings yet

- Option Greek - The Option GuideDocument6 pagesOption Greek - The Option GuidePINALNo ratings yet

- Accounting Instructions 3Document1 pageAccounting Instructions 3Ely DanelNo ratings yet

- 15 Illustrating The Nature of Bivariate DataDocument27 pages15 Illustrating The Nature of Bivariate DataLerwin Garinga75% (8)

- Chicken Business PlanDocument16 pagesChicken Business PlanmschotoNo ratings yet

- Study Habits of Grade 11 and 12 Abm Students in Taal Senior High SchoolDocument26 pagesStudy Habits of Grade 11 and 12 Abm Students in Taal Senior High SchoolAphol Joyce Mortel67% (3)

- Penyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)Document6 pagesPenyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)ABDUL HALIM BIN A WAHAB MoeNo ratings yet

- CHED-TDP Forms and RequirementsDocument2 pagesCHED-TDP Forms and RequirementsAphol Joyce Mortel0% (1)

- 13 Sps Santos vs. Court of AppealsDocument2 pages13 Sps Santos vs. Court of AppealsMyla RodrigoNo ratings yet

- Exercise Workbook: Smartbooks BasicDocument21 pagesExercise Workbook: Smartbooks BasicAngelica TuazonNo ratings yet

- Dilag Vs Heirs of ResurrecionDocument2 pagesDilag Vs Heirs of ResurrecionMariaNiñaBlessheGravosoNo ratings yet

- Rizal Sa DapitanDocument3 pagesRizal Sa DapitanAphol Joyce MortelNo ratings yet

- Uge2 - ReviewerDocument12 pagesUge2 - ReviewerCharie Mea SalveNo ratings yet

- Definition of Credit and CollectionsDocument5 pagesDefinition of Credit and CollectionsDrew MerezNo ratings yet

- Fitt 2 Handouts 2021Document5 pagesFitt 2 Handouts 2021nhicabonit7No ratings yet

- Features common to all forecasts and elements of a good forecastDocument2 pagesFeatures common to all forecasts and elements of a good forecastRJ DAVE DURUHA100% (1)

- Accounting Assignment 1Document2 pagesAccounting Assignment 1Hamna FarooqNo ratings yet

- Activity Number 5 Elasticity of Demand & SupplyDocument5 pagesActivity Number 5 Elasticity of Demand & SupplyLovely Madrid0% (1)

- Lesson 1-Preliminaries-Nature and Classes of CorporationsDocument10 pagesLesson 1-Preliminaries-Nature and Classes of CorporationsAterg MooseNo ratings yet

- A Manufacturer of Glass Bottles Has Been Affected by CompetitionDocument2 pagesA Manufacturer of Glass Bottles Has Been Affected by CompetitionAmit Pandey0% (1)

- 6726 Revised Conceptual FrameworkDocument7 pages6726 Revised Conceptual FrameworkJane ValenciaNo ratings yet

- Laura Taylor wholesale distributor worksheetDocument3 pagesLaura Taylor wholesale distributor worksheetHope Trinity EnriquezNo ratings yet

- Classroom Discussion 3 - 04172021Document1 pageClassroom Discussion 3 - 04172021LLYOD FRANCIS LAYLAYNo ratings yet

- According To MenesDocument1 pageAccording To MenesSophia BilayaNo ratings yet

- Acctg11 CN 3000 TQ Midterm Exam 1ST Sem 2021-2022Document5 pagesAcctg11 CN 3000 TQ Midterm Exam 1ST Sem 2021-2022Jaya RamirezNo ratings yet

- What Are The Opportunities and Risks of China at The Time of The Case?Document3 pagesWhat Are The Opportunities and Risks of China at The Time of The Case?Adam CuencaNo ratings yet

- I. Learning Activities: Sum of Weights (3+2+1) 6Document6 pagesI. Learning Activities: Sum of Weights (3+2+1) 6Valdez AlyssaNo ratings yet

- Adjusting Entries Discussion and SolutionDocument6 pagesAdjusting Entries Discussion and SolutionGarp BarrocaNo ratings yet

- 1 - Exercises On Relevant Cost 1Document7 pages1 - Exercises On Relevant Cost 1Temesgen AbezaNo ratings yet

- Horizontal Analysis Interpretation PDFDocument2 pagesHorizontal Analysis Interpretation PDFAlison JcNo ratings yet

- Chapter 28 - Gross Profit and Retail Method: ANSWER 28-1Document12 pagesChapter 28 - Gross Profit and Retail Method: ANSWER 28-1Cyrus IsanaNo ratings yet

- Project Management 2Document62 pagesProject Management 2Abdul HaseebNo ratings yet

- Mid Term Assignment 1 On FAR - Journalizing, Posting, and Unadjusted Trial BalanceDocument1 pageMid Term Assignment 1 On FAR - Journalizing, Posting, and Unadjusted Trial BalanceAnne AlagNo ratings yet

- Jhonah Joyce B Lumba ACC111(962) VAT Activity ReportDocument1 pageJhonah Joyce B Lumba ACC111(962) VAT Activity ReportJhoyce LumbaNo ratings yet

- Investagrams Virtual Trading RIVERADocument3 pagesInvestagrams Virtual Trading RIVERACarlo RiveraNo ratings yet

- Defining Legal Terms and Discussing ObligationsDocument5 pagesDefining Legal Terms and Discussing ObligationsCresenciano MalabuyocNo ratings yet

- xACC 213Document10 pagesxACC 213CharlesNo ratings yet

- CfasDocument32 pagesCfasLouiseNo ratings yet

- Week 4 5 ULOc Lets Analyze Activities SolutionDocument3 pagesWeek 4 5 ULOc Lets Analyze Activities Solutionemem resuentoNo ratings yet

- Accounting 101 - Reviewer (TEST QUIZ)Document18 pagesAccounting 101 - Reviewer (TEST QUIZ)AuroraNo ratings yet

- Exam Questionaire in IntermediateDocument5 pagesExam Questionaire in IntermediateJester IlaganNo ratings yet

- Module 5.2 - Sample ExercisesDocument8 pagesModule 5.2 - Sample ExercisesJaimell LimNo ratings yet

- Cfas - Chapter 8: Pas 1 - Presentation of Financial STATEMENTS (Statement of Financial Position)Document2 pagesCfas - Chapter 8: Pas 1 - Presentation of Financial STATEMENTS (Statement of Financial Position)agm25No ratings yet

- Article 2085 2123Document3 pagesArticle 2085 2123Kyootie QNo ratings yet

- Building Excellence in Construction CompaniesDocument9 pagesBuilding Excellence in Construction CompaniesMok MokNo ratings yet

- Why Burundi Remains One of the Poorest CountriesDocument2 pagesWhy Burundi Remains One of the Poorest CountriesThird MontefalcoNo ratings yet

- Chapter 6 - Notes ReceivableDocument5 pagesChapter 6 - Notes ReceivableTurks100% (1)

- MANAGEMENT ACCOUNTING SOLUTIONS CHAPTER 14 RESPONSIBILITY ACCOUNTINGDocument24 pagesMANAGEMENT ACCOUNTING SOLUTIONS CHAPTER 14 RESPONSIBILITY ACCOUNTINGAang GrandeNo ratings yet

- Planning and Budgeting Case StudyDocument3 pagesPlanning and Budgeting Case StudyRichie Donato100% (1)

- Business Cup Level 1 Quiz BeeDocument28 pagesBusiness Cup Level 1 Quiz BeeRowellPaneloSalapareNo ratings yet

- Quick Guide Book On Operations Management With Analytics v2023Document197 pagesQuick Guide Book On Operations Management With Analytics v2023cristiancelerianNo ratings yet

- Pick N' Peel Business Marketing PlanDocument22 pagesPick N' Peel Business Marketing PlanMutevu SteveNo ratings yet

- 2 CFAS Course Assessment A To DDocument4 pages2 CFAS Course Assessment A To DKing SigueNo ratings yet

- SM Quiz1Document4 pagesSM Quiz1Ah BiiNo ratings yet

- FUNDACC1 - Reviewer (Theories)Document12 pagesFUNDACC1 - Reviewer (Theories)MelvsNo ratings yet

- Understanding Financial InstrumentsDocument11 pagesUnderstanding Financial InstrumentsMaria G. BernardinoNo ratings yet

- Condonation or RemissionDocument6 pagesCondonation or RemissionRhon Mhiel RomanoNo ratings yet

- Intacc 3 HWDocument7 pagesIntacc 3 HWMelissa Kayla ManiulitNo ratings yet

- Reclassification of Financial AssetsDocument30 pagesReclassification of Financial AssetsSheila Grace BajaNo ratings yet

- Fundamentals of TransportationDocument5 pagesFundamentals of TransportationsanoNo ratings yet

- Accounting Chapter 9Document7 pagesAccounting Chapter 9Angelica Faye DuroNo ratings yet

- What Is The Difference Between An Adjunct Account and A Contra AccountDocument1 pageWhat Is The Difference Between An Adjunct Account and A Contra AccountDarlene SarcinoNo ratings yet

- St. Paul University Surigao Surigao City, Philippines: The Problem and Its BackgroundDocument7 pagesSt. Paul University Surigao Surigao City, Philippines: The Problem and Its BackgroundivyNo ratings yet

- Chapter 26 Land and BuildingDocument17 pagesChapter 26 Land and BuildingKendall JennerNo ratings yet

- 9Document10 pages9Maria G. BernardinoNo ratings yet

- INTERMEDIATE ACCOUNTING 1 - MidtermDocument6 pagesINTERMEDIATE ACCOUNTING 1 - Midtermailel isagaNo ratings yet

- 2019 Level 1 CFASDocument8 pages2019 Level 1 CFASMary Angeline LopezNo ratings yet

- Short Term Budgeting UpdatedDocument23 pagesShort Term Budgeting UpdatedNineteen AùgùstNo ratings yet

- Master Budget Framework for Planning and ControlDocument5 pagesMaster Budget Framework for Planning and ControlJeson MalinaoNo ratings yet

- Profit Planning or Budgeting: Control Is The Use of Budget To Control A Firm's ActivitiesDocument30 pagesProfit Planning or Budgeting: Control Is The Use of Budget To Control A Firm's ActivitiesRaven Dumlao OllerNo ratings yet

- Hernandez, Vincent Jaed Semi-Final-Exam-GEd107-04.19.2021Document4 pagesHernandez, Vincent Jaed Semi-Final-Exam-GEd107-04.19.2021Aphol Joyce MortelNo ratings yet

- Batangas State University Internship AgreementDocument4 pagesBatangas State University Internship AgreementAphol Joyce MortelNo ratings yet

- HERNANDEZ, VINCENT JAED C (Pictorial Literacy)Document2 pagesHERNANDEZ, VINCENT JAED C (Pictorial Literacy)Aphol Joyce MortelNo ratings yet

- Honda Safety Driving Center AboutDocument2 pagesHonda Safety Driving Center AboutAphol Joyce MortelNo ratings yet

- BatstateU Implementing Rules & RegulationDocument24 pagesBatstateU Implementing Rules & RegulationKim Hyuna100% (1)

- Hernandez, Vincent Jaed C (Message)Document3 pagesHernandez, Vincent Jaed C (Message)Aphol Joyce MortelNo ratings yet

- Vincent Jaed Hernandez - Article ReviewDocument1 pageVincent Jaed Hernandez - Article ReviewAphol Joyce MortelNo ratings yet

- Group 3 BSA 3103 Semestral OutputDocument12 pagesGroup 3 BSA 3103 Semestral OutputAphol Joyce MortelNo ratings yet

- Hernandez, Vincent Jaed C (PhilHis Act 1)Document1 pageHernandez, Vincent Jaed C (PhilHis Act 1)Aphol Joyce MortelNo ratings yet

- The Documented Essay General Guidelines: Getting StartedDocument5 pagesThe Documented Essay General Guidelines: Getting StartedRafhael PalacNo ratings yet

- Aphol Part 2Document1 pageAphol Part 2Aphol Joyce MortelNo ratings yet

- BSMA Group Accomplishment Report for Business ProposalDocument3 pagesBSMA Group Accomplishment Report for Business ProposalAphol Joyce MortelNo ratings yet

- Henandez, Vincent J C (Job Interview Questions)Document1 pageHenandez, Vincent J C (Job Interview Questions)Aphol Joyce MortelNo ratings yet

- Hernandez, Vincent Jaed C (PhilHis Act 1)Document1 pageHernandez, Vincent Jaed C (PhilHis Act 1)Aphol Joyce MortelNo ratings yet

- Edited by DeaDocument43 pagesEdited by DeaAphol Joyce MortelNo ratings yet

- Activity1 STS - FINALDocument9 pagesActivity1 STS - FINALAphol Joyce MortelNo ratings yet

- Balance Sheet (Accrual Basis)Document1 pageBalance Sheet (Accrual Basis)Aphol Joyce MortelNo ratings yet

- UtilitarianismDocument4 pagesUtilitarianismAphol Joyce MortelNo ratings yet

- Trial Balance: Mortel - BSA 2102 - Hands-On ExercisesDocument2 pagesTrial Balance: Mortel - BSA 2102 - Hands-On ExercisesAphol Joyce MortelNo ratings yet

- Aphol Part 2Document1 pageAphol Part 2Aphol Joyce MortelNo ratings yet

- BookDocument1 pageBookAphol Joyce MortelNo ratings yet

- Detailed SimulationR Evenue CycleDocument12 pagesDetailed SimulationR Evenue CycleAphol Joyce MortelNo ratings yet

- Poverty and Discrimination Deprived Filipinos of Quality EducationDocument3 pagesPoverty and Discrimination Deprived Filipinos of Quality EducationAphol Joyce MortelNo ratings yet

- BookDocument1 pageBookAphol Joyce MortelNo ratings yet

- Case-Digest G. R No L-27906 (Mortel, Aphol Joyce B)Document4 pagesCase-Digest G. R No L-27906 (Mortel, Aphol Joyce B)Aphol Joyce MortelNo ratings yet

- Exercise - Dilutive Securities - AdillaikhsaniDocument4 pagesExercise - Dilutive Securities - Adillaikhsaniaidil fikri ikhsan100% (1)

- Mutual Fund AnalysisDocument53 pagesMutual Fund AnalysisVijetha EdduNo ratings yet

- CFP - SuggestedSolutions - RPEBDocument6 pagesCFP - SuggestedSolutions - RPEBSODDEYNo ratings yet

- BR Act 1949Document25 pagesBR Act 1949dranita@yahoo.comNo ratings yet

- Jurnal PajakDocument43 pagesJurnal PajakIndahNo ratings yet

- M12 Titman 2544318 11 FinMgt C12Document80 pagesM12 Titman 2544318 11 FinMgt C12marjsbarsNo ratings yet

- Distressed Debt InvestingDocument5 pagesDistressed Debt Investingjt322No ratings yet

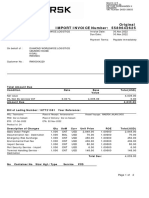

- Original IMPORT INVOICE Number: 5589642625: Total Amount Due Condition Rate Base Value Total (USD)Document2 pagesOriginal IMPORT INVOICE Number: 5589642625: Total Amount Due Condition Rate Base Value Total (USD)AllyNo ratings yet

- Ohb Ar2019Document222 pagesOhb Ar2019Clint LohNo ratings yet

- Journal Entries For PartnershipsDocument11 pagesJournal Entries For PartnershipsRosette Revilala100% (1)

- Financial StatementsDocument2 pagesFinancial StatementsRjoshua PlaylistNo ratings yet

- Case Fair Macro13e Accessible Ppt 05 (Автосохраненный)Document30 pagesCase Fair Macro13e Accessible Ppt 05 (Автосохраненный)Zhanerke NurmukhanovaNo ratings yet

- Oct 2022 Unit 2 QPDocument32 pagesOct 2022 Unit 2 QPKarama OmarNo ratings yet

- J&K Bank - Annual Report 2015-16 PDFDocument212 pagesJ&K Bank - Annual Report 2015-16 PDFKunal AggarwalNo ratings yet

- DIA 22-05 NDOC Fiscal Processes.2Document36 pagesDIA 22-05 NDOC Fiscal Processes.2Sean GolonkaNo ratings yet

- Case Study (ENT530)Document12 pagesCase Study (ENT530)Nur Diyana50% (2)

- FACE - Nov 2012 Vol 5Document32 pagesFACE - Nov 2012 Vol 5UJAccountancyNo ratings yet

- Instruction: Write Your Name and Answer in A Journal/paper. Submit A MAXIMUM OF 6 PICTURES OnlyDocument1 pageInstruction: Write Your Name and Answer in A Journal/paper. Submit A MAXIMUM OF 6 PICTURES Onlyhokage astroNo ratings yet

- Asset Deals, Share Deals and Financing M&AsDocument49 pagesAsset Deals, Share Deals and Financing M&AsAnna LinNo ratings yet

- Busifin Final Period 2021 2022Document46 pagesBusifin Final Period 2021 2022Glenn Mark NochefrancaNo ratings yet

- Fees 2018 - The HillsDocument1 pageFees 2018 - The Hillsvelaphi_nhlapo2936No ratings yet

- DNB Bank in Lithuania overviewDocument9 pagesDNB Bank in Lithuania overviewDonata BrukmanaitėNo ratings yet

- Annual Refresher Program in Teaching (ARPIT) through National Resource Centres (NRCsDocument14 pagesAnnual Refresher Program in Teaching (ARPIT) through National Resource Centres (NRCsthensureshNo ratings yet