You might also like

- Tutorial Sheet 4Document8 pagesTutorial Sheet 4Hhvvgg BbbbNo ratings yet

- Bank Recon DiscussionDocument6 pagesBank Recon DiscussionKrigfordNo ratings yet

- Sol To Bank Recon Problem 1 3Document9 pagesSol To Bank Recon Problem 1 3Michael JimNo ratings yet

- DFD Bank Account FlowDocument1 pageDFD Bank Account FlowRana AhmedNo ratings yet

- Answer Key To Bank Reconciliation Statement 14-12-2021Document53 pagesAnswer Key To Bank Reconciliation Statement 14-12-2021Abdelkadr NurhisenNo ratings yet

- Date Description Input Tax Check No. Cash On Hand Purchases Discount Post. Ref. Cash in BankDocument7 pagesDate Description Input Tax Check No. Cash On Hand Purchases Discount Post. Ref. Cash in BankZaida RectoNo ratings yet

- Accounting Chapter 8 Warren AnswerDocument16 pagesAccounting Chapter 8 Warren AnswerFadhly Azzuhry0% (1)

- Actg14 Activity Group4Document2 pagesActg14 Activity Group4anneNo ratings yet

- Payment Process Request Status ReportDocument1 pagePayment Process Request Status ReportNishant RanaNo ratings yet

- Bank Reconciliation - Solutions To Problem 4 and 5Document2 pagesBank Reconciliation - Solutions To Problem 4 and 5Joana Trinidad100% (1)

- Akuntansi Pengatar Pertemuan Ke 3Document4 pagesAkuntansi Pengatar Pertemuan Ke 3WiwitvlogNo ratings yet

- Organisation's Name Last Day in Financial Year Funds CategoriesDocument40 pagesOrganisation's Name Last Day in Financial Year Funds CategoriesDonSmarts InvestmentsNo ratings yet

- General Journal: Date Description PR Debit CreditDocument14 pagesGeneral Journal: Date Description PR Debit CreditAllen CarlNo ratings yet

- Pa 06 Pay 22112402322Document1 pagePa 06 Pay 22112402322Admin Kuda MasNo ratings yet

- Foundation Acc Full Sol Set 15.11.2021Document245 pagesFoundation Acc Full Sol Set 15.11.2021adityatiwari122006No ratings yet

- LJK JurnalDocument6 pagesLJK JurnalRidho SyafputraNo ratings yet

- 05 May 2020 - (Free) ..CHcMWD92CHM - bg0Fan8Hcxh - Ewx-GQB8AGdyd2Z-cA1xAHFyChl0CHEIcnEJdnQIcQh0cwFzdQpyDHVyCgDocument2 pages05 May 2020 - (Free) ..CHcMWD92CHM - bg0Fan8Hcxh - Ewx-GQB8AGdyd2Z-cA1xAHFyChl0CHEIcnEJdnQIcQh0cwFzdQpyDHVyCgDanny WilsonNo ratings yet

- JurnalDocument7 pagesJurnalLilis ChintiaNo ratings yet

- Check Number Bank Name Amount CurrencyDocument2 pagesCheck Number Bank Name Amount CurrencySreenivas oracleNo ratings yet

- Akun Pengantar Jurnal Ledger Neraca SaldoDocument13 pagesAkun Pengantar Jurnal Ledger Neraca SaldoAdi Al HadiNo ratings yet

- Pangan CompanyDocument18 pagesPangan CompanyWendy Lupaz80% (5)

- Bank Reconciled KBZ MMKDocument2 pagesBank Reconciled KBZ MMKMgKAGNo ratings yet

- Problem 3.1: (Requirement 1) Bank Reconciliation StatementDocument30 pagesProblem 3.1: (Requirement 1) Bank Reconciliation StatementMarvin MarianoNo ratings yet

- Job Sheet KosongDocument33 pagesJob Sheet KosongHatta Rasyida SulaimanNo ratings yet

- Format Jurnal TB - Tasya Aulia 1810102003Document13 pagesFormat Jurnal TB - Tasya Aulia 1810102003TasyaAuliaRahmanNo ratings yet

- Lee Tailors: General Journal Month of June 2020 Date Particulars RefDocument6 pagesLee Tailors: General Journal Month of June 2020 Date Particulars RefRodolfo CorpuzNo ratings yet

- To Record The Purchase of EquipmentDocument13 pagesTo Record The Purchase of EquipmentShane Nayah100% (1)

- E1 - FINACT1 - Proof of CashDocument1 pageE1 - FINACT1 - Proof of CashKevin James Sedurifa OledanNo ratings yet

- Far Module 1 ApolDocument7 pagesFar Module 1 ApolJeraldine DejanNo ratings yet

- September 3, 2020, 730AM Group # 4 Members: Cagape, Patrice Cercado, Geran Jimenez, Angel Quiñanola, Alana Resabal, Mariel Sarmillo, WenzelDocument3 pagesSeptember 3, 2020, 730AM Group # 4 Members: Cagape, Patrice Cercado, Geran Jimenez, Angel Quiñanola, Alana Resabal, Mariel Sarmillo, WenzelAngel Kaye Nacionales JimenezNo ratings yet

- Modelo de Factura Proforma en Inglés para WordDocument1 pageModelo de Factura Proforma en Inglés para WordStar LPNo ratings yet

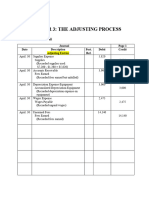

- Chapter 3 The Adjusting Process Template 1Document7 pagesChapter 3 The Adjusting Process Template 1phamhhuonggg5512No ratings yet

- RequestDocument5 pagesRequestfasdfaNo ratings yet

- Sewabill 783744353046Document1 pageSewabill 783744353046Mehidi Hasan ShishirNo ratings yet

- TransactionsDocument1 pageTransactionsjamesmunro49No ratings yet

- PDF 1Document4 pagesPDF 1Umair MaqboolNo ratings yet

- InvoiceDocument1 pageInvoiceWan WeiNo ratings yet

- Invoice Template OrangescrumDocument5 pagesInvoice Template OrangescrumFelicia GhicaNo ratings yet

- Sewabill 783749178911Document1 pageSewabill 783749178911Mehidi Hasan ShishirNo ratings yet

- Uas Pengakun 2Document4 pagesUas Pengakun 2Givania RahmadhaniNo ratings yet

- Exercises - Control AcountsDocument3 pagesExercises - Control AcountsPetrinaNo ratings yet

- Statement of Account1Document1 pageStatement of Account1SophiaNo ratings yet

- Contoh Power Point AkuntansiDocument3 pagesContoh Power Point AkuntansiAi TanahashiNo ratings yet

- TajanaDocument6 pagesTajanasusa.spiroNo ratings yet

- Nandyal Municipality: ReceiptDocument1 pageNandyal Municipality: ReceiptRavi KumarNo ratings yet

- Screenshot 2022-08-15 at 6.48.18 PMDocument23 pagesScreenshot 2022-08-15 at 6.48.18 PMahsanukkakarNo ratings yet

- Total Amount Payable AED 1,238.54: 0116919271 3 Mar 2022 1 Feb 2022 - 28 Feb 2022 5.78954Document23 pagesTotal Amount Payable AED 1,238.54: 0116919271 3 Mar 2022 1 Feb 2022 - 28 Feb 2022 5.78954ahsanukkakarNo ratings yet

- Chapter 2 Problem SolvingDocument20 pagesChapter 2 Problem SolvingJohn LucaNo ratings yet

- Cash Proof of CashDocument4 pagesCash Proof of Cashadriancanlas243No ratings yet

- Chapter 2 - Problem SolvingDocument20 pagesChapter 2 - Problem SolvingMaria Licuanan100% (1)

- Cho Cho's - SarayDocument6 pagesCho Cho's - SarayLaiza Cristella SarayNo ratings yet

- Hensley, - Juan - Jaime SabinesDocument2 pagesHensley, - Juan - Jaime SabinesJuan HensleyNo ratings yet

- Adjusted Cash Balance Per Bank: Accounting Records Bank StatementDocument2 pagesAdjusted Cash Balance Per Bank: Accounting Records Bank StatementDenil LouNo ratings yet

- Special Journal AnswerDocument6 pagesSpecial Journal AnswerHazel DimaanoNo ratings yet

- Job Sheet KosongDocument33 pagesJob Sheet KosongDita Ananda80% (5)

- RDInstallmentReport27 02 2024Document1 pageRDInstallmentReport27 02 2024Himanshu JenaNo ratings yet

- Tin: Taxpayer'S Name: Trade Name: Registered AddressDocument16 pagesTin: Taxpayer'S Name: Trade Name: Registered AddressArah OpalecNo ratings yet

- Cash App Nov 2022 StatementDocument3 pagesCash App Nov 2022 Statementchde795No ratings yet

- BANK RECON MS Excel Discussion NotesDocument2 pagesBANK RECON MS Excel Discussion NotesCamilla Marel D. TABIOS,No ratings yet

- (Oliver)Document1 page(Oliver)renewmachineryNo ratings yet

- Indonesia Tax Info March 2021: Implementing Regulations For Omnibus Law Have Been IssuedDocument18 pagesIndonesia Tax Info March 2021: Implementing Regulations For Omnibus Law Have Been IssuedAbu AfkariNo ratings yet

- Pre-Budget Expenditure UPDATE 2020: October 2020Document37 pagesPre-Budget Expenditure UPDATE 2020: October 2020Abu AfkariNo ratings yet

- Indonesia Individual Income Tax Guide 1Document24 pagesIndonesia Individual Income Tax Guide 1Abu AfkariNo ratings yet

- Trademark Registration in Indonesia Helps Protect The OwnerDocument3 pagesTrademark Registration in Indonesia Helps Protect The OwnerAbu AfkariNo ratings yet