You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 167.SAMELCO-1 Vs CIRDocument11 pages167.SAMELCO-1 Vs CIRClyde KitongNo ratings yet

- 163.perez Vs CTADocument22 pages163.perez Vs CTAClyde KitongNo ratings yet

- 154.CIR Vs BPIDocument7 pages154.CIR Vs BPIClyde KitongNo ratings yet

- 168.cagayan Robina Vs CADocument5 pages168.cagayan Robina Vs CAClyde KitongNo ratings yet

- 150.CIR Vs PDIDocument19 pages150.CIR Vs PDIClyde KitongNo ratings yet

- 151.CIR Vs Asalus CorpDocument7 pages151.CIR Vs Asalus CorpClyde KitongNo ratings yet

- 153.CIR Vs La FlorDocument9 pages153.CIR Vs La FlorClyde KitongNo ratings yet

- 136.talentino Vs EscaladaDocument7 pages136.talentino Vs EscaladaClyde KitongNo ratings yet

- 143.CIR Vs Stanley (Phils.)Document8 pages143.CIR Vs Stanley (Phils.)Clyde KitongNo ratings yet

- 132.fitness by Design Vs CIRDocument6 pages132.fitness by Design Vs CIRClyde KitongNo ratings yet

- 127.CIR Vs PLDTDocument9 pages127.CIR Vs PLDTClyde KitongNo ratings yet

- 124.ANPC Vs BIRDocument7 pages124.ANPC Vs BIRClyde KitongNo ratings yet

- 118.accenture Vs CIRDocument11 pages118.accenture Vs CIRClyde KitongNo ratings yet

- 116.CIR Vs Fireman's Fund InsuranceDocument6 pages116.CIR Vs Fireman's Fund InsuranceClyde KitongNo ratings yet

- The Regular Corporate Income TaxDocument4 pagesThe Regular Corporate Income TaxReniel Renz AterradoNo ratings yet

- Asmt 10 1920Document69 pagesAsmt 10 1920Prashant ZawareNo ratings yet

- Primer On The Tax Amnesty Act of 2007Document8 pagesPrimer On The Tax Amnesty Act of 2007cmv mendozaNo ratings yet

- Self Employed DocumentDocument11 pagesSelf Employed DocumentapproachdirectNo ratings yet

- Notes Class XDocument2 pagesNotes Class XmailinspectoryadavNo ratings yet

- 1Document6 pages1afsalmaulanaNo ratings yet

- 50 Fixed Assets RegisterDocument30 pages50 Fixed Assets RegisterKiran NanduNo ratings yet

- TRAIN LAW Comparative AnalysisDocument2 pagesTRAIN LAW Comparative AnalysisElaine100% (3)

- Income From CompensationDocument10 pagesIncome From Compensationdarlene floresNo ratings yet

- Documents Needed For Capital Gains Tax & Transfer of TitleDocument4 pagesDocuments Needed For Capital Gains Tax & Transfer of TitleBossing NicNo ratings yet

- Od329130352044371100 1Document4 pagesOd329130352044371100 1Strongest AvengerNo ratings yet

- AR Standard PDFDocument2 pagesAR Standard PDFValentina Bernal QuinteroNo ratings yet

- Maccaferri Environmental Solutions Pvt. LTDDocument7 pagesMaccaferri Environmental Solutions Pvt. LTDThangaselviSubramanianNo ratings yet

- SARS Confirmation LetterDocument1 pageSARS Confirmation Letterpmo41973No ratings yet

- SAP Automatic Payment ProgramDocument13 pagesSAP Automatic Payment Programmpsingh1122No ratings yet

- Loan ConfirmationDocument1 pageLoan Confirmationkrishnajhawar100% (4)

- 1701 Annual Income Tax Return: Rogelio D. GonzalesDocument1 page1701 Annual Income Tax Return: Rogelio D. GonzalesJoshua CarzaNo ratings yet

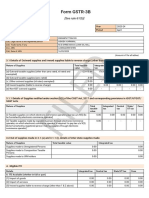

- GSTR3B 09bwbpk7755a1zk 042023Document3 pagesGSTR3B 09bwbpk7755a1zk 042023Ankit JainNo ratings yet

- Coupon Policy - SwiggyDocument3 pagesCoupon Policy - SwiggyOur First JourneysNo ratings yet

- Bar Ops TaxDocument2 pagesBar Ops TaxJan Maxine PalomataNo ratings yet

- 57498bos46599cp6 PDFDocument212 pages57498bos46599cp6 PDFManoj GNo ratings yet

- Account - 11208100007124 Saiyad Akil Zilani: AddressDocument21 pagesAccount - 11208100007124 Saiyad Akil Zilani: AddressAamena BanuNo ratings yet

- $1,500.000.00 Usd (One Million Five Hundred Thousand United State Dollar)Document2 pages$1,500.000.00 Usd (One Million Five Hundred Thousand United State Dollar)VICTOR RAÚL LEÓN MEDINA67% (3)

- GSTR1 Excel Workbook Template V1.5Document92 pagesGSTR1 Excel Workbook Template V1.5OmPrakashRoyNo ratings yet

- Pekao 2808 2022 #0192392357Document7 pagesPekao 2808 2022 #0192392357dfsfds sdfsdfNo ratings yet

- LACDP - Form - Membership - Alternate Appointment 2008-2010Document1 pageLACDP - Form - Membership - Alternate Appointment 2008-2010roblesdemocratNo ratings yet

- TAX QuizzesDocument2 pagesTAX Quizzesnichols greenNo ratings yet

- Energy Credit VoucherDocument1 pageEnergy Credit VoucherRammReads (RammReads)No ratings yet

- Form CST Errors Sno Error Box Description Error Line No Error Box NoDocument12 pagesForm CST Errors Sno Error Box Description Error Line No Error Box NoVivek PatilNo ratings yet

- Disbursements Through Tax Remittance AdviceDocument3 pagesDisbursements Through Tax Remittance AdvicePostbae GaloneNo ratings yet