You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- What Is Commercial Banks - Definition, Structure, Functions, Asset Structure, Role, ProblemsDocument15 pagesWhat Is Commercial Banks - Definition, Structure, Functions, Asset Structure, Role, ProblemsdhaiwatNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Exam Schedule Winter 2016Document1 pageExam Schedule Winter 2016Don't SayNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Merrick Bank DepositDocument2 pagesMerrick Bank DepositSeth Alley100% (1)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Chapter-5 Merchant: BankingDocument29 pagesChapter-5 Merchant: BankingaswinecebeNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

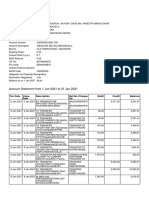

- Sbi Account Jan 2021Document2 pagesSbi Account Jan 2021Manoj GaurNo ratings yet

- Chapter 20 - AnswerDocument12 pagesChapter 20 - Answerwynellamae100% (3)

- A Brief Research On Investment Corporation of BangladeshDocument14 pagesA Brief Research On Investment Corporation of BangladeshShakil NaheyanNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Auditing Theory Overview of The Audit Process With AnswersDocument44 pagesAuditing Theory Overview of The Audit Process With AnswersNikolajay MarrenoNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- C6 Lecture NotesDocument2 pagesC6 Lecture NotesJonathan NavalloNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Manual On Non-Bank InstitutionsDocument888 pagesManual On Non-Bank InstitutionsFatima BagayNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- "Study On Loan and Credit Facility at SDCC Bank, Rourkela ": Summer Internship Project Report OnDocument81 pages"Study On Loan and Credit Facility at SDCC Bank, Rourkela ": Summer Internship Project Report OnASIT EKKANo ratings yet

- Chapter 5 - Audit CompletionDocument47 pagesChapter 5 - Audit CompletionKHÁNH PHAN HOÀNG VÂNNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Negotiable Instrument: Private International LawDocument20 pagesNegotiable Instrument: Private International LawAnkita SinhaNo ratings yet

- BellaDocument17 pagesBellaDeimos DeezNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Fdocuments - in PNB Training ReportdocxDocument87 pagesFdocuments - in PNB Training ReportdocxAviral Pratap Singh KhareNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Invoice Flomih & Vio Bussines SRL: CX Ref: 18911926 Invoice No.: 151140-838 Invoice Date: 29 Nov 2019Document1 pageInvoice Flomih & Vio Bussines SRL: CX Ref: 18911926 Invoice No.: 151140-838 Invoice Date: 29 Nov 2019calinmusceleanuNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Reviewer For Fundamentals of Accounting and Business ManagementDocument4 pagesReviewer For Fundamentals of Accounting and Business ManagementAngelo PeraltaNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Discounted Cash Flow (DCF) Modeling: Case Study: AppleDocument117 pagesDiscounted Cash Flow (DCF) Modeling: Case Study: AppleKarinNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- John Geissinger ResumeDocument2 pagesJohn Geissinger Resumekurtis_workmanNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Tax Invoice:) ) @Ç!! ( Â!!!fJ XSFDocument8 pagesTax Invoice:) ) @Ç!! ( Â!!!fJ XSFAndy BassNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Registration of Mutual FundDocument23 pagesRegistration of Mutual FundmoizizzyNo ratings yet

- Hedge Fund Wisdom: Free Sample IssueDocument85 pagesHedge Fund Wisdom: Free Sample Issuemarketfolly.comNo ratings yet

- Dwnload Full Auditing and Assurance Services A Systematic Approach 9th Edition Messier Solutions Manual PDFDocument36 pagesDwnload Full Auditing and Assurance Services A Systematic Approach 9th Edition Messier Solutions Manual PDFpetrorichelle501100% (15)

- Fraud Risk Assessment: An Empirical AnalysisDocument11 pagesFraud Risk Assessment: An Empirical AnalysisGDPNo ratings yet

- Iowa Turkey Federation PAC - 9743 - ScannedDocument5 pagesIowa Turkey Federation PAC - 9743 - ScannedZach EdwardsNo ratings yet

- Private Equity Model Template For InvestorsDocument12 pagesPrivate Equity Model Template For InvestorsousmaneNo ratings yet

- Nor Hayati Bte IbrahimDocument1 pageNor Hayati Bte Ibrahimyatie9429No ratings yet

- Types of Marine PoliciesDocument3 pagesTypes of Marine PoliciescapmanirajNo ratings yet

- CostDocument3 pagesCostMary CharlesNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- AUB Secretary Certificate TemplateDocument3 pagesAUB Secretary Certificate TemplateSteve Barretto0% (1)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)