You might also like

- Convertibility of TakaDocument8 pagesConvertibility of Takajashim_urNo ratings yet

- Detailed Invitation For BidDocument1 pageDetailed Invitation For Bidevonik123456No ratings yet

- DividendDocument11 pagesDividendManish KumarNo ratings yet

- Blog Details Declaration and Payment of Dividend 20Document9 pagesBlog Details Declaration and Payment of Dividend 20Abhinay KumarNo ratings yet

- Corporate TaxDocument12 pagesCorporate TaxRaselNo ratings yet

- Foreign Investment in Bangladesh: Section - IDocument3 pagesForeign Investment in Bangladesh: Section - IM Kaderi KibriaNo ratings yet

- Mudarabah Financing AgreementDocument8 pagesMudarabah Financing AgreementEthica Institute of Islamic Finance™100% (2)

- Dividend A Brief NoteDocument7 pagesDividend A Brief NoteaakashagarwalNo ratings yet

- GfetDocument47 pagesGfetRahman JorjiNo ratings yet

- Repatriation of Residual Money Payable To Foreign Shareholders in Case of Winding Up of A CompanyDocument2 pagesRepatriation of Residual Money Payable To Foreign Shareholders in Case of Winding Up of A CompanyAsif AhmadNo ratings yet

- NBFC Registration FeeDocument3 pagesNBFC Registration Feens_solankiNo ratings yet

- Concept of DividendDocument26 pagesConcept of DividendAnant GargNo ratings yet

- MRC Fema Update 5Document2 pagesMRC Fema Update 5mukeashNo ratings yet

- Declaration and Distribution of Dividends by A Company Under Indian LawDocument8 pagesDeclaration and Distribution of Dividends by A Company Under Indian LawHarimohan NamdevNo ratings yet

- Annual Filing Under Companies Act 2013: V Verma & CompanyDocument15 pagesAnnual Filing Under Companies Act 2013: V Verma & CompanyAnonymous rKRfW9SYtNo ratings yet

- Brief Note On Annual Report PDFDocument4 pagesBrief Note On Annual Report PDFMaruko ChanNo ratings yet

- Income Tax ComplianceDocument4 pagesIncome Tax ComplianceJusefNo ratings yet

- Standard Covenant CCDocument3 pagesStandard Covenant CCPriyam MrigNo ratings yet

- Import Bill, Scrutiny, LodgementDocument41 pagesImport Bill, Scrutiny, Lodgementomi0855No ratings yet

- Fema Rbi Org inDocument11 pagesFema Rbi Org inamishtheanalystNo ratings yet

- Setting Up of Branch Office Abroad: Contributed byDocument16 pagesSetting Up of Branch Office Abroad: Contributed byDheeru DheeruNo ratings yet

- Regulations ExportDocument37 pagesRegulations ExportgopalushaNo ratings yet

- Dividend NoteDocument11 pagesDividend NoteSHANNo ratings yet

- Regulatory Provisions Under EcbDocument6 pagesRegulatory Provisions Under EcbAllwyn FlowNo ratings yet

- Corporate TaxDocument17 pagesCorporate TaxVishnupriya RameshNo ratings yet

- Dividend Dividend Dividend Dividend Dividend: BackgrounderDocument23 pagesDividend Dividend Dividend Dividend Dividend: BackgrounderSubrahmanya SringeriNo ratings yet

- SEC Memo 11-08Document9 pagesSEC Memo 11-08Matthew TiuNo ratings yet

- Audit of General Insurance CompaniesDocument20 pagesAudit of General Insurance CompaniesZiniaKhanNo ratings yet

- Accounts and Audit L 18Document10 pagesAccounts and Audit L 18Everything NewNo ratings yet

- Legal, Procedural & Tax Aspects of DividendsDocument18 pagesLegal, Procedural & Tax Aspects of DividendsNavneet Nanda100% (1)

- Step by Step Procedure As in Regards To Incorporation of A Joint Venture Company in BangladeshDocument3 pagesStep by Step Procedure As in Regards To Incorporation of A Joint Venture Company in BangladeshEt CeteraNo ratings yet

- Caro 2020Document10 pagesCaro 2020vishnu tejaNo ratings yet

- Interim-Dividen-2021-22 - TDS-on-dividend-CommunicationDocument4 pagesInterim-Dividen-2021-22 - TDS-on-dividend-CommunicationNimesh PatelNo ratings yet

- Sec Memo 11, s2008Document5 pagesSec Memo 11, s2008aian josephNo ratings yet

- Dividend PolicyDocument16 pagesDividend PolicyDương Thuỳ TrangNo ratings yet

- FEC1 Annex ADocument6 pagesFEC1 Annex Anewuser01No ratings yet

- New Microsoft Office Word DocumentDocument30 pagesNew Microsoft Office Word Documentawais_hussain7998No ratings yet

- Chapter-13: Export: Obligation and Role of AD BanksDocument46 pagesChapter-13: Export: Obligation and Role of AD BanksRaja GopalakrishnanNo ratings yet

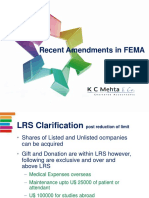

- Recent Amendments in FemaDocument14 pagesRecent Amendments in FemaSarath Kumar Vijaya KumarNo ratings yet

- Cridit Managment: MBA Banking & Finance 3 TermDocument20 pagesCridit Managment: MBA Banking & Finance 3 Term✬ SHANZA MALIK ✬No ratings yet

- 19668ipcc Acc Vol1 Chapter-3Document20 pages19668ipcc Acc Vol1 Chapter-3Vignesh SrinivasanNo ratings yet

- Note of Issue of Fully Convertible DebenturesDocument3 pagesNote of Issue of Fully Convertible DebenturesakhiljindalNo ratings yet

- Adv Aud Final May08Document16 pagesAdv Aud Final May08Fazi HaiderNo ratings yet

- Foreign Currency Convertible Bonds FinalDocument15 pagesForeign Currency Convertible Bonds FinalGautam JainNo ratings yet

- Foreign Exchange Investment Department Bangladesh Bank Head Office DhakaDocument2 pagesForeign Exchange Investment Department Bangladesh Bank Head Office Dhakamirmuiz2993No ratings yet

- Dividend & Accounts of ComplanyDocument38 pagesDividend & Accounts of ComplanySrikant0% (1)

- By Sriram Parthasarathy, Director Prowis Corporate Services Private LTD.Document41 pagesBy Sriram Parthasarathy, Director Prowis Corporate Services Private LTD.riteshsharda767No ratings yet

- Exemption 10AA Notes-1Document9 pagesExemption 10AA Notes-1SanaNo ratings yet

- DividendDocument8 pagesDividendMuzammil LiaquatNo ratings yet

- Declaration of DividendsDocument3 pagesDeclaration of DividendsAnubha DwivediNo ratings yet

- Set OffDocument9 pagesSet OffAditya MehtaniNo ratings yet

- Procedure For BODocument6 pagesProcedure For BOmsn_testNo ratings yet

- Refund Guide For Business Visitors - en - 17 09 2019Document21 pagesRefund Guide For Business Visitors - en - 17 09 2019Islam AdelNo ratings yet

- Bangladesh Company Law Guide BD Chapter PDFDocument16 pagesBangladesh Company Law Guide BD Chapter PDFRafid IshrakNo ratings yet

- Sec Memorandum Circular No. 11 Series of 2008Document3 pagesSec Memorandum Circular No. 11 Series of 2008Miguel Anas Jr.No ratings yet

- Summary of IND As 110 and IFRS 10 Consolidated Financial Statements - Taxguru - inDocument7 pagesSummary of IND As 110 and IFRS 10 Consolidated Financial Statements - Taxguru - inalok kumarNo ratings yet

- Chapter 8 Declaration and Payment of Dividend Lyst3195Document15 pagesChapter 8 Declaration and Payment of Dividend Lyst3195Rambo HereNo ratings yet

- ECM Chapter 6Document51 pagesECM Chapter 6Pooja GujarathiNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- (Norton Critical Edition) Wayne A Meeks - John T Fitzgerald-The Writings of St. Paul - Annotated Texts, Reception and criticism-W.W. Norton (2007) PDFDocument193 pages(Norton Critical Edition) Wayne A Meeks - John T Fitzgerald-The Writings of St. Paul - Annotated Texts, Reception and criticism-W.W. Norton (2007) PDFEllenxevelyn0% (2)

- Cascade Regional Holdings Limited Annual Report Financial Statements 31 December 2019 PDFDocument51 pagesCascade Regional Holdings Limited Annual Report Financial Statements 31 December 2019 PDFVishal RathiNo ratings yet

- Adcc Bafm 4C Strama GRP.2Document4 pagesAdcc Bafm 4C Strama GRP.2TedNo ratings yet

- Assessment Cover Sheet: Student Must Fill This SectionDocument49 pagesAssessment Cover Sheet: Student Must Fill This SectionParash RijalNo ratings yet

- February 2019: AWS Elating To Maintenance of Wife in IndiaDocument46 pagesFebruary 2019: AWS Elating To Maintenance of Wife in IndiaSHUBHAM RAJNo ratings yet

- Lease Agreement - Triparty Draft VenusDocument16 pagesLease Agreement - Triparty Draft VenusthiruNo ratings yet

- Multi Choice Questions On Income Approach K. C. Jhavar, Btech, Mba, Mval (Re) Retd. Asst. Gen. Manager, Erst S. B. Indore Govt. Regd. ValuerDocument8 pagesMulti Choice Questions On Income Approach K. C. Jhavar, Btech, Mba, Mval (Re) Retd. Asst. Gen. Manager, Erst S. B. Indore Govt. Regd. ValuerAnirban DeyNo ratings yet

- Corporate Budget Circular No 23Document7 pagesCorporate Budget Circular No 23Tesa GDNo ratings yet

- Delete Blank Rows in Excel - Easy Excel TutorialDocument5 pagesDelete Blank Rows in Excel - Easy Excel TutorialJamalodeen MohammadNo ratings yet

- Application Form - Credit Transfer-2Document2 pagesApplication Form - Credit Transfer-2Husna ZakariaNo ratings yet

- Dr. Ram Manohar Lohiya National Law University 2020-2021Document13 pagesDr. Ram Manohar Lohiya National Law University 2020-2021Anshumaan JaiswalNo ratings yet

- 43 - People V Lol-Lo and SarawDocument2 pages43 - People V Lol-Lo and Sarawnikol crisangNo ratings yet

- Prudential Bank Vs IACDocument7 pagesPrudential Bank Vs IAC001nooneNo ratings yet

- The Cradle of The RepublicDocument305 pagesThe Cradle of The RepublicOpenEye100% (3)

- Decision: Kuroda v. Jalandoni, G.R. No. L-2662, March 26, 1949Document18 pagesDecision: Kuroda v. Jalandoni, G.R. No. L-2662, March 26, 1949Aliyah SandersNo ratings yet

- NFL Drug Complaint UnredactedDocument155 pagesNFL Drug Complaint UnredactedDeadspinNo ratings yet

- Achin H Sheth: Career ObjectiveDocument3 pagesAchin H Sheth: Career ObjectiveJigar SoniNo ratings yet

- Philosophy & Religious Studies IGCSE NotesDocument23 pagesPhilosophy & Religious Studies IGCSE Notesincognitowl50% (2)

- Daily Nation July 15th 2014Document96 pagesDaily Nation July 15th 2014jorina807No ratings yet

- Mun ManifestoDocument55 pagesMun ManifestoMaria Jesus Salazar MoralesNo ratings yet

- GlobalNews - Staff Personalities - Elizabeth McSheffreyDocument18 pagesGlobalNews - Staff Personalities - Elizabeth McSheffreykelvinkinergyNo ratings yet

- The SAT's Top 1000 Vocabulary Words ADocument2 pagesThe SAT's Top 1000 Vocabulary Words Ayeo pinoNo ratings yet

- Online Hate Speech Essay Competition Runner UpDocument12 pagesOnline Hate Speech Essay Competition Runner UpNuno CaetanoNo ratings yet

- Analysis-Of-Financial-Statements-Of-Jio A51Document62 pagesAnalysis-Of-Financial-Statements-Of-Jio A51rohit bhoirNo ratings yet

- BOARD RESO-dole Appeal BondDocument2 pagesBOARD RESO-dole Appeal BondLieca AmbolNo ratings yet

- IPCR JAN-JUN 2018-Inventory SectionDocument143 pagesIPCR JAN-JUN 2018-Inventory SectionMathan LuceroNo ratings yet

- Elearning-Chapter 6-Cross Border TransportDocument74 pagesElearning-Chapter 6-Cross Border Transportkhine zin thawNo ratings yet

- Sale of Goods .Document24 pagesSale of Goods .Goodman supremacyNo ratings yet

- Objective Type (OMR Valuation) (Please See Syllabus On The Last Page)Document2 pagesObjective Type (OMR Valuation) (Please See Syllabus On The Last Page)Ninson KMNo ratings yet

- Requirements in B.S. Pmi BoholDocument2 pagesRequirements in B.S. Pmi BoholNorwin Alcaide50% (2)