You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Fuck You-1Document9 pagesFuck You-1Trish Hit57% (7)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Bankruptcy Outline - 24 June 2018Document36 pagesBankruptcy Outline - 24 June 2018Ma FajardoNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Loans ReceivableDocument4 pagesLoans ReceivableDianna Dayawon0% (1)

- Form Tenancy in Common AgreementDocument11 pagesForm Tenancy in Common AgreementMikeRosen100% (1)

- Individual Tax Payer - TeachersDocument8 pagesIndividual Tax Payer - TeachersKhervin EvangelistaNo ratings yet

- Uniform Commercial Code (UCC)Document1 pageUniform Commercial Code (UCC)Nelson HarrisNo ratings yet

- SEND Q2 GM Week 1Document37 pagesSEND Q2 GM Week 1wilzl sarrealNo ratings yet

- Group 6 - Zopa Case StudyDocument2 pagesGroup 6 - Zopa Case StudyRahul Kumar100% (2)

- OBC 016 - United Planters Sugar Milling Co., Lnc. v. Court of Appeals - G.R. No. 126890Document23 pagesOBC 016 - United Planters Sugar Milling Co., Lnc. v. Court of Appeals - G.R. No. 126890Maria Anna M LegaspiNo ratings yet

- SWOT Analysis of Asset ClassesDocument7 pagesSWOT Analysis of Asset ClassesShreya BhagavatulaNo ratings yet

- FAR Final Preboard QuestionaireDocument18 pagesFAR Final Preboard Questionaireyzhlansang.studentNo ratings yet

- Analysis On Customer Service Department Activities Of: HBL, Itahari BranchDocument50 pagesAnalysis On Customer Service Department Activities Of: HBL, Itahari BranchSujan BajracharyaNo ratings yet

- Dhaka Bank Term PaperDocument4 pagesDhaka Bank Term Paperafdttqbna100% (1)

- Managerial Economics and Organizational Architecture 5th Edition Brickley Test BankDocument10 pagesManagerial Economics and Organizational Architecture 5th Edition Brickley Test BankChadHallewob100% (13)

- Money and Banking Course OutlineDocument4 pagesMoney and Banking Course OutlineUzair TezanNo ratings yet

- Chapter 03Document39 pagesChapter 03Nor Asma LodeNo ratings yet

- Reit PPT Vornado Realty Trust PresentationDocument42 pagesReit PPT Vornado Realty Trust PresentationDaniel GoytrNo ratings yet

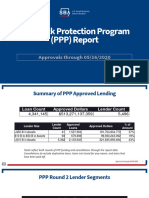

- PPP ReportDocument7 pagesPPP ReportBrittany EtheridgeNo ratings yet

- Richmond RES. 2023-R027 - Res. No. 2023-R027Document176 pagesRichmond RES. 2023-R027 - Res. No. 2023-R027Activate VirginiaNo ratings yet

- Notice of Motion and Motion To Stay Proceedings Pending Outcome of State Court of Appeals With Exhibits 1 and 2Document26 pagesNotice of Motion and Motion To Stay Proceedings Pending Outcome of State Court of Appeals With Exhibits 1 and 2Emanuel McCrayNo ratings yet

- Property 2 NotesDocument16 pagesProperty 2 NotesEmely Almonte100% (1)

- A Study of Capital Structure ManagementDocument94 pagesA Study of Capital Structure ManagementBijaya DhakalNo ratings yet

- Commented Final ResearchDocument49 pagesCommented Final Researchshekur wosen100% (1)

- Apply Principles of Professional PracticeDocument15 pagesApply Principles of Professional PracticeBelay Kassahun100% (2)

- PNB v. Agudelo y GonzagaDocument2 pagesPNB v. Agudelo y GonzagaElle MichNo ratings yet

- Loan Agreement and Promissory Note: Maria Christina E. Gaviola Legforms 3B Atty. CallejaDocument5 pagesLoan Agreement and Promissory Note: Maria Christina E. Gaviola Legforms 3B Atty. CallejaKIARA DANIELLE NAZARIONo ratings yet

- Problems To Be Solved in ClassDocument4 pagesProblems To Be Solved in ClassAlp SanNo ratings yet

- MOI 4.1 Amort and SFDocument11 pagesMOI 4.1 Amort and SFBaekhyun ByunNo ratings yet

- Ibc Research PaperDocument3 pagesIbc Research PaperKHUSHAL MITTAL 1650424No ratings yet

- CERSAI Search Report 200269168172 For Asset Based Search 20 05 2023 07 41 59 975Document4 pagesCERSAI Search Report 200269168172 For Asset Based Search 20 05 2023 07 41 59 975Kshitij KatiyarNo ratings yet