You might also like

- Top Two Ways Corporations Raise CapitalDocument4 pagesTop Two Ways Corporations Raise CapitalSam vermNo ratings yet

- Arrangement of Funds LPSDocument57 pagesArrangement of Funds LPSRohan SinglaNo ratings yet

- FM Module 4 Capital Structure of A CompanyDocument6 pagesFM Module 4 Capital Structure of A CompanyJeevan RobinNo ratings yet

- The Other Questions 22052023Document33 pagesThe Other Questions 22052023Anjanee PersadNo ratings yet

- Report - FonterraDocument19 pagesReport - FonterraK59 DOAN THANH TAMNo ratings yet

- Investment Law - PagesDocument9 pagesInvestment Law - PagesAbhilasha RoyNo ratings yet

- FM Unit 3Document9 pagesFM Unit 3ashraf hussainNo ratings yet

- Notes On Coporate Finance-Raising of Capital 2020 Vol 1-5Document9 pagesNotes On Coporate Finance-Raising of Capital 2020 Vol 1-5Mårkh NaháNo ratings yet

- Finance 1.Document26 pagesFinance 1.Karylle SuarezNo ratings yet

- 3 - Descriptive Questions With Answers (20) DoneDocument13 pages3 - Descriptive Questions With Answers (20) DoneZeeshan SikandarNo ratings yet

- Bus. Finance 2. Final 2.Document9 pagesBus. Finance 2. Final 2.Gia PorqueriñoNo ratings yet

- Entrepreneur: BY Obih, A. O. Solomon PHDDocument27 pagesEntrepreneur: BY Obih, A. O. Solomon PHDChikyNo ratings yet

- Unit Iii-1Document13 pagesUnit Iii-1Archi VarshneyNo ratings yet

- Professional Practices Capital Investment GuideDocument17 pagesProfessional Practices Capital Investment GuideThe Explorers - Your Travel PartnerNo ratings yet

- EquityDocument5 pagesEquityAkansha NarayanNo ratings yet

- What Are Shares? Why Do They Exist? What Is Debt-Equity Ratio (Pros and Cons) ?Document11 pagesWhat Are Shares? Why Do They Exist? What Is Debt-Equity Ratio (Pros and Cons) ?ankdub85No ratings yet

- 7.1. Source of Project FinanceDocument7 pages7.1. Source of Project FinanceTemesgenNo ratings yet

- Financial analysis and funding optionsDocument15 pagesFinancial analysis and funding optionsSuhaib KtNo ratings yet

- Different Types of Business Financing Case Study On: Great Service Cleaning and Maintenance CompanyDocument9 pagesDifferent Types of Business Financing Case Study On: Great Service Cleaning and Maintenance CompanyElias ChembeNo ratings yet

- Capital Structure DefinitionDocument15 pagesCapital Structure DefinitionVan MateoNo ratings yet

- Capital StructureDocument57 pagesCapital StructureRao ShekherNo ratings yet

- Raising Funds Through EquityDocument20 pagesRaising Funds Through Equityapi-3705920No ratings yet

- Sources and Uses of Short-Term and Long-Term FundsDocument7 pagesSources and Uses of Short-Term and Long-Term FundsSyrill Cayetano0% (1)

- BFIN300 Full Hands OutDocument46 pagesBFIN300 Full Hands OutGauray LionNo ratings yet

- Long Term Financing: Types of Equity SharesDocument15 pagesLong Term Financing: Types of Equity SharesTulsi GovaniNo ratings yet

- UNIT-IV-Financing of ProjectsDocument13 pagesUNIT-IV-Financing of ProjectsDivya ChilakapatiNo ratings yet

- Fairfield Institute of Management and Technology: Debt FinancingDocument11 pagesFairfield Institute of Management and Technology: Debt FinancingDhroov BalyanNo ratings yet

- Gayda KateDocument12 pagesGayda KateJessa GallardoNo ratings yet

- Assignment Unit VIDocument21 pagesAssignment Unit VIHạnh NguyễnNo ratings yet

- Lecture - Sources of FinanceDocument27 pagesLecture - Sources of FinanceNelson MapaloNo ratings yet

- E8 Business FinanceDocument8 pagesE8 Business FinanceTENGKU ANIS TENGKU YUSMANo ratings yet

- Individuals AssignmentDocument7 pagesIndividuals AssignmentQuỳnh NhưNo ratings yet

- 5.2 Alternative Sources of FundsDocument4 pages5.2 Alternative Sources of FundsJerson AgsiNo ratings yet

- Generation and Allocation of FundsDocument2 pagesGeneration and Allocation of FundsTHUNDER STORMNo ratings yet

- Capital Structure and Financing StrategiesDocument29 pagesCapital Structure and Financing StrategiesTalha ChaudharyNo ratings yet

- Coperate FinanceDocument17 pagesCoperate Financegift lunguNo ratings yet

- Financing of Entrepreneurial VentureDocument19 pagesFinancing of Entrepreneurial VentureKshitiz RawalNo ratings yet

- Dividend Investing for Beginners & DummiesFrom EverandDividend Investing for Beginners & DummiesRating: 5 out of 5 stars5/5 (1)

- PMF Unit 5Document10 pagesPMF Unit 5dummy manNo ratings yet

- Sources of FinanceDocument25 pagesSources of FinanceAnand Kumar MishraNo ratings yet

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingFrom EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNo ratings yet

- FinanceDocument68 pagesFinanceAngelica CruzNo ratings yet

- Factors Determining Capital StructureDocument3 pagesFactors Determining Capital StructuretushNo ratings yet

- Unit 5 Financial Management Complete NotesDocument17 pagesUnit 5 Financial Management Complete Notesvaibhav shuklaNo ratings yet

- Capital Structure PlanningDocument5 pagesCapital Structure PlanningAlok Singh100% (1)

- Top 2 Ways Corporations Raise CapitalDocument1 pageTop 2 Ways Corporations Raise CapitalFirdaNo ratings yet

- ResearchDocument5 pagesResearchCherry Amor Venzon OngsonNo ratings yet

- Define Corporate Finance and Its ImportanceDocument80 pagesDefine Corporate Finance and Its ImportanceShanthiNo ratings yet

- Financial ManagementDocument16 pagesFinancial ManagementRahul PuriNo ratings yet

- CF 3rd AssignmentDocument6 pagesCF 3rd AssignmentAnjum SamiraNo ratings yet

- Corporate Finance BasicsDocument27 pagesCorporate Finance BasicsAhimbisibwe BenyaNo ratings yet

- Financial Structure Ratio AnalysisDocument6 pagesFinancial Structure Ratio AnalysisJames Levi Tan QuintanaNo ratings yet

- Corporate Finance Scope Types Startup DecisionsDocument7 pagesCorporate Finance Scope Types Startup DecisionsTanya MalviyaNo ratings yet

- Capital Structure Issues: V. VI. V.1 Mergers and Acquisitions Definition and DifferencesDocument26 pagesCapital Structure Issues: V. VI. V.1 Mergers and Acquisitions Definition and Differenceskelvin pogiNo ratings yet

- BUS5111 - Week 6 Paper - 2022Document8 pagesBUS5111 - Week 6 Paper - 2022Mohammed MounirNo ratings yet

- LONG-TERM CAPITALDocument13 pagesLONG-TERM CAPITALafoninadin81No ratings yet

- Financial ManagementDocument23 pagesFinancial ManagementRiad ChowdhuryNo ratings yet

- Managing Financial Resources and DecisionsDocument18 pagesManaging Financial Resources and DecisionsAbdullahAlNomunNo ratings yet

- Sources of FinanceDocument19 pagesSources of FinanceDavinder SharmaNo ratings yet

- Dividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementFrom EverandDividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementNo ratings yet

- Company Law 2 MANAGEMENTDocument38 pagesCompany Law 2 MANAGEMENTTumwesigyeNo ratings yet

- Company Law EssentialsDocument30 pagesCompany Law EssentialsTumwesigyeNo ratings yet

- Companies Act 2012Document253 pagesCompanies Act 2012Nyeko FrancisNo ratings yet

- Assignment 2021Document21 pagesAssignment 2021TumwesigyeNo ratings yet

- Makerere University Business SchoolDocument4 pagesMakerere University Business SchoolTumwesigyeNo ratings yet

- 2B - 800MWKudgi - Ash Handling Vol I NTPC TenderDocument616 pages2B - 800MWKudgi - Ash Handling Vol I NTPC Tendersreedhar_blueNo ratings yet

- DBP vs CA Land Dispute DecisionDocument3 pagesDBP vs CA Land Dispute DecisionLynlyn Oprenario PajamutanNo ratings yet

- Project On Punjab National BankDocument86 pagesProject On Punjab National BankRohit ChauhanNo ratings yet

- An Internship Report On - ExtraDocument102 pagesAn Internship Report On - ExtraImam Hossain MishorNo ratings yet

- Resi Verification FormatDocument1 pageResi Verification Formatmrgandhi1No ratings yet

- 138 Sta. Maria V HSBC (1951) - MiguelDocument3 pages138 Sta. Maria V HSBC (1951) - MiguelVianca MiguelNo ratings yet

- Renew Your Auto Insurance with PNB General InsurersDocument1 pageRenew Your Auto Insurance with PNB General InsurersDeejay FarioNo ratings yet

- Letter To GovernorDocument3 pagesLetter To GovernorMoneylife FoundationNo ratings yet

- CASE - Araprop V LeongDocument29 pagesCASE - Araprop V LeongIqram MeonNo ratings yet

- Third Party AnnexureDocument2 pagesThird Party AnnexureNavin ChoudharyNo ratings yet

- Credit Transactions Case DigestsDocument226 pagesCredit Transactions Case Digestslouis jansen100% (8)

- Republic Planters Bank Vs CADocument4 pagesRepublic Planters Bank Vs CAMarkJobelleMantillaNo ratings yet

- Thomas Cook India Partners With Mastercard To Launch The Thanks Again Loyalty Programme For The India Market" (Company Update)Document4 pagesThomas Cook India Partners With Mastercard To Launch The Thanks Again Loyalty Programme For The India Market" (Company Update)Shyam SunderNo ratings yet

- Hussain Shahid Thesis, SadiqDocument60 pagesHussain Shahid Thesis, SadiqSadiq SagheerNo ratings yet

- Thanetavanh Ogunrayi (Fannie Mae)Document3 pagesThanetavanh Ogunrayi (Fannie Mae)mohit_kumar5538No ratings yet

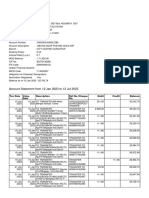

- Account Statement From 12 Jan 2023 To 12 Jul 2023Document10 pagesAccount Statement From 12 Jan 2023 To 12 Jul 2023SouravDeyNo ratings yet

- Cash and Cash Equivalents DefinitionDocument7 pagesCash and Cash Equivalents DefinitionApril NaidaNo ratings yet

- CH 10Document16 pagesCH 10nur maiyissaNo ratings yet

- 02 DBM v. Kolonwel TradingDocument10 pages02 DBM v. Kolonwel TradingCamille CruzNo ratings yet

- Financial System QuestionsDocument25 pagesFinancial System QuestionsJ. KNo ratings yet

- The Global Economic Impact of Private Equity Report 2008Document189 pagesThe Global Economic Impact of Private Equity Report 2008World Economic Forum100% (48)

- HDFC LifeDocument13 pagesHDFC LifeShaqib A KadriNo ratings yet

- Awnot 003 Awxx 6.0Document11 pagesAwnot 003 Awxx 6.0aliNo ratings yet

- The Fuller Method Learn To Grow Your Money Exponentially - V4.0 14 PDFDocument35 pagesThe Fuller Method Learn To Grow Your Money Exponentially - V4.0 14 PDFartlet100% (1)

- Axis Bank AptitudeDocument94 pagesAxis Bank AptitudeladmohanNo ratings yet

- Ketan Parekh Scam FinalDocument20 pagesKetan Parekh Scam FinalMohit3107No ratings yet

- The Financial Services Sector in IndiaDocument4 pagesThe Financial Services Sector in IndiaKhyati PatelNo ratings yet

- Management by Objectives (MBO) - Peter Drucker MBODocument7 pagesManagement by Objectives (MBO) - Peter Drucker MBODebanjan DebNo ratings yet

- 07 Affidavit Cover LetterDocument2 pages07 Affidavit Cover LetterTerry Green100% (3)

- Money MastersDocument53 pagesMoney Masterssoumyabrata dasNo ratings yet