You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Never Run Out of MoneyDocument22 pagesNever Run Out of MoneyHukleNo ratings yet

- ACCOUNTING FOR PENSIONS AND POSTRETIREMENT BENEFITS ch20 PDFDocument50 pagesACCOUNTING FOR PENSIONS AND POSTRETIREMENT BENEFITS ch20 PDFashandron4everNo ratings yet

- What Is ERE - Early Retirement Extreme WikiDocument5 pagesWhat Is ERE - Early Retirement Extreme Wikiawetia100% (1)

- Sample of Seven Figure PharmacistDocument17 pagesSample of Seven Figure PharmacistVal Marie RodriguezNo ratings yet

- Retirement WorkbookDocument31 pagesRetirement WorkbookRunita ShahNo ratings yet

- Select The Correct Response Correct: Questions Without/pending AnswersDocument19 pagesSelect The Correct Response Correct: Questions Without/pending AnswersPran piyaNo ratings yet

- Select The Correct Response Correct: Questions Without/pending AnswersDocument19 pagesSelect The Correct Response Correct: Questions Without/pending AnswersPran piyaNo ratings yet

- Employee Benefits 03Document11 pagesEmployee Benefits 03Nelva Quinio33% (3)

- Domingo, Raissa Therese Mabini, Jea Angeline B. Reyes, Alliah BelleDocument5 pagesDomingo, Raissa Therese Mabini, Jea Angeline B. Reyes, Alliah BellePran piyaNo ratings yet

- Universal Robina Sugar Milling Corp. vs. CaballedaDocument2 pagesUniversal Robina Sugar Milling Corp. vs. CaballedaAnn MarieNo ratings yet

- Mabini Bsa22 Laboratory Activity 5Document7 pagesMabini Bsa22 Laboratory Activity 5Pran piyaNo ratings yet

- Report 29Document9 pagesReport 29Pran piya100% (1)

- Incentives For Foreign InvestorsDocument2 pagesIncentives For Foreign InvestorsPran piyaNo ratings yet

- Clearer Lab FormatDocument2 pagesClearer Lab FormatPran piyaNo ratings yet

- Report Report 23Document9 pagesReport Report 23Pran piyaNo ratings yet

- Submissions - B-BTAX211 BSA22 1st Sem (2021-2022) - Enabling Assessment - Dealings in Properties and The Withholding Tax System - DLSU-D College - GSDocument3 pagesSubmissions - B-BTAX211 BSA22 1st Sem (2021-2022) - Enabling Assessment - Dealings in Properties and The Withholding Tax System - DLSU-D College - GSPran piyaNo ratings yet

- Case 11Document2 pagesCase 11Pran piyaNo ratings yet

- De La Salle University - Dasmariñas: Mathematics and Statistics DepartmentDocument4 pagesDe La Salle University - Dasmariñas: Mathematics and Statistics DepartmentPran piyaNo ratings yet

- Mabini, Jea Angeline B. BSA16Document3 pagesMabini, Jea Angeline B. BSA16Pran piyaNo ratings yet

- Ea-3 2Document8 pagesEa-3 2Pran piyaNo ratings yet

- Mabini Jea Socio-Anthro PerspectiveDocument3 pagesMabini Jea Socio-Anthro PerspectivePran piyaNo ratings yet

- Mabini, Jea Profit-Maximizing Output and Pricing Decisions in Oligopolistic MarketDocument4 pagesMabini, Jea Profit-Maximizing Output and Pricing Decisions in Oligopolistic MarketPran piyaNo ratings yet

- Mabini Module 5 Enabling AssesmentDocument4 pagesMabini Module 5 Enabling AssesmentPran piyaNo ratings yet

- Mabini Drred Synthesis FinalDocument4 pagesMabini Drred Synthesis FinalPran piyaNo ratings yet

- Research Paper - Retirement Village. Arch362r01-Dp2-Rp - Babiera - Jocel RecaDocument12 pagesResearch Paper - Retirement Village. Arch362r01-Dp2-Rp - Babiera - Jocel RecaJoan BabieraNo ratings yet

- IRLLDocument12 pagesIRLLGurjeet KaurNo ratings yet

- Pre-Competency Checklist: (Formative/Diagnotic Assessment) : Sherwin M. Calinao Bsit-Automotive 3BDocument3 pagesPre-Competency Checklist: (Formative/Diagnotic Assessment) : Sherwin M. Calinao Bsit-Automotive 3BAngelica AycardoNo ratings yet

- Un Pan 92431Document12 pagesUn Pan 92431Farid HilmiNo ratings yet

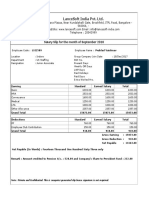

- Prahlad Vaishnav Payslip September 2018Document1 pagePrahlad Vaishnav Payslip September 2018PRAHLAD VAISHNAV100% (1)

- BRTCDocument31 pagesBRTCDahafu DihwotNo ratings yet

- Human Resource Management: Benefits and ServicesDocument12 pagesHuman Resource Management: Benefits and ServicesThơ ĐìnhNo ratings yet

- Module 5 Lesson 3 - CODE OF CONDUCT FOR PUBLIC OFFICIALS AND EMPLOYEESDocument48 pagesModule 5 Lesson 3 - CODE OF CONDUCT FOR PUBLIC OFFICIALS AND EMPLOYEESVIA BAWINGANNo ratings yet

- Assignment 2Document15 pagesAssignment 2Nicolas KuiperNo ratings yet

- Brea ch05 BMM 7e SGDocument91 pagesBrea ch05 BMM 7e SGAshish BhallaNo ratings yet

- 15 Santos vs. Servier Philippines, Inc PDFDocument8 pages15 Santos vs. Servier Philippines, Inc PDFAriel Conrad MalimasNo ratings yet

- Jobs, Jobs, Jobs: Creating More Employment in EuropeDocument57 pagesJobs, Jobs, Jobs: Creating More Employment in EuropeAttila TihanyiNo ratings yet

- CLASS NOTES-Voluntary RetirementDocument11 pagesCLASS NOTES-Voluntary RetirementOnline LecturesNo ratings yet

- FormulaDocument13 pagesFormulaMichBadilloCalanogNo ratings yet

- Social Security CalculatorDocument20 pagesSocial Security CalculatorHamood HabibiNo ratings yet

- Impact of Compensation On Employee's ProductivityDocument45 pagesImpact of Compensation On Employee's ProductivityRamin HamzaNo ratings yet

- Summary of Gsis BenefitsDocument4 pagesSummary of Gsis BenefitsFrank Lloyd CadornaNo ratings yet

- NYC Pension ChartDocument3 pagesNYC Pension ChartrkarlinNo ratings yet

- Interdisciplinary Management Research - IMR IIIDocument518 pagesInterdisciplinary Management Research - IMR IIIEFOS ManagementNo ratings yet

- CIFC Exam Prep Live Webinar Practice Questions 2018 v.2 69276 1 25 2018 1254Document17 pagesCIFC Exam Prep Live Webinar Practice Questions 2018 v.2 69276 1 25 2018 1254Anup KhanalNo ratings yet

- 17 DBM V Manila - S Finest Retirees Assoc PDFDocument19 pages17 DBM V Manila - S Finest Retirees Assoc PDFKriszan ManiponNo ratings yet

- George The Banker Case Study of Career ManagementDocument2 pagesGeorge The Banker Case Study of Career ManagementMohsin Khan100% (1)

- Chapter 5 AnswersDocument13 pagesChapter 5 Answersjanajani2012_3761915100% (1)