You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Marquis de LafayetteDocument7 pagesThe Marquis de Lafayetteapi-361128500No ratings yet

- WARN Trans States AirlinesDocument2 pagesWARN Trans States AirlinesDavid PurtellNo ratings yet

- Sir Roger Vernon ScrutonDocument26 pagesSir Roger Vernon ScrutonZviad MiminoshviliNo ratings yet

- Kami Export - Lucas Perez - Prohibitions WebquestDocument3 pagesKami Export - Lucas Perez - Prohibitions WebquestTactical DogeNo ratings yet

- In The High Court of Judicature at Bombay Criminal Appellate Jurisdiction Criminal Writ Petition No.1238 of 2019Document1 pageIn The High Court of Judicature at Bombay Criminal Appellate Jurisdiction Criminal Writ Petition No.1238 of 2019Prashant Ranjan SinghNo ratings yet

- Ca-G.r. SP No. 14994Document2 pagesCa-G.r. SP No. 14994Net WeightNo ratings yet

- Writing About Academic Labor: Joss WinnDocument15 pagesWriting About Academic Labor: Joss WinnCheshta AroraNo ratings yet

- PELLET 2005 Complementarity of International Treaty Law Customary Law and Non Contractual Law Making PDFDocument8 pagesPELLET 2005 Complementarity of International Treaty Law Customary Law and Non Contractual Law Making PDFაკაკი ბერიძეNo ratings yet

- Contempo Final Quiz 1Document5 pagesContempo Final Quiz 1James Marasigan AmbasNo ratings yet

- Osprey, Men-At-Arms #007 The Black Brunswickers (1973) OCR 8.12Document50 pagesOsprey, Men-At-Arms #007 The Black Brunswickers (1973) OCR 8.12mancini100% (6)

- Incorrect Memorandum Following George Washington University Censure VoteDocument9 pagesIncorrect Memorandum Following George Washington University Censure VoteThe College FixNo ratings yet

- Mike Crites BioDocument2 pagesMike Crites BiowmdtvmattNo ratings yet

- Angela DavisDocument12 pagesAngela DavisRyan Wilbur Jenkins RandolphNo ratings yet

- Teknik Bahasa Humor Komedian Sadana Agung Dan KeteDocument11 pagesTeknik Bahasa Humor Komedian Sadana Agung Dan KeteIlyas Al hafizNo ratings yet

- Punjab Politics and The Wavell Plan: A Note of Critical ReappraisalDocument19 pagesPunjab Politics and The Wavell Plan: A Note of Critical ReappraisalNirmal singhNo ratings yet

- Pawb Technical Bulletin NO. 2013-05: (Caves and Cave Resources Conservation, Management and Protection)Document6 pagesPawb Technical Bulletin NO. 2013-05: (Caves and Cave Resources Conservation, Management and Protection)Billy RavenNo ratings yet

- 360 OS ProgramDocument3 pages360 OS ProgramRapplerNo ratings yet

- Witch Hunting A Gendercide Tool To Subordinate Women: Priyanka BharadwajDocument4 pagesWitch Hunting A Gendercide Tool To Subordinate Women: Priyanka BharadwajSharon TiggaNo ratings yet

- Disadvantages of Globalization and Social ChangeDocument3 pagesDisadvantages of Globalization and Social ChangeSheikh Shahriar Ahmed ShajonNo ratings yet

- AirtelDocument2 pagesAirtelAkansha GuptaNo ratings yet

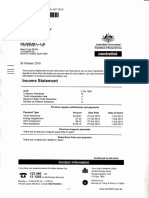

- Income Statement: Llillliltll) Ilililtil)Document1 pageIncome Statement: Llillliltll) Ilililtil)Indy EfuNo ratings yet

- We Have Tailored AfricaDocument12 pagesWe Have Tailored AfricaSetsuna NicoNo ratings yet

- School Form 2 (SF 2) JULYDocument8 pagesSchool Form 2 (SF 2) JULYTinTinNo ratings yet

- Doctrines Justifying Takaful - 1 - 2Document14 pagesDoctrines Justifying Takaful - 1 - 2=paul=No ratings yet

- Lobby Series p1Document1 pageLobby Series p1juliespring123No ratings yet

- Wadie Haddad: A Biography (Wikipedia)Document2 pagesWadie Haddad: A Biography (Wikipedia)XINKIANGNo ratings yet

- Catherine PANKO, Administratrix of The Estate of Margaret R. Barrett, Deceased and John Barrett, Her Husband, Appellants, v. Food Fair Stores, IncDocument2 pagesCatherine PANKO, Administratrix of The Estate of Margaret R. Barrett, Deceased and John Barrett, Her Husband, Appellants, v. Food Fair Stores, IncScribd Government DocsNo ratings yet

- TAITZ V ASTRUE (USDC HI) - 15 - ORDER DENYING PLAINTIFF'S EMERGENCY EX PARTE MOTION FOR EMERGENCY ORDER TO SHOW CAUSE AND - Gov - Uscourts.hid.98529.15.0Document2 pagesTAITZ V ASTRUE (USDC HI) - 15 - ORDER DENYING PLAINTIFF'S EMERGENCY EX PARTE MOTION FOR EMERGENCY ORDER TO SHOW CAUSE AND - Gov - Uscourts.hid.98529.15.0Jack RyanNo ratings yet

- Law, Rhetoric, and Irony in The Formation of Canadian Civil Culture (PDFDrive)Document374 pagesLaw, Rhetoric, and Irony in The Formation of Canadian Civil Culture (PDFDrive)Dávid KisNo ratings yet

- A Collectography of PAD/D by Gregory SholetteDocument15 pagesA Collectography of PAD/D by Gregory SholetteAntonio SernaNo ratings yet