You might also like

- International Public Sector Accounting Standards Implementation Road Map for UzbekistanFrom EverandInternational Public Sector Accounting Standards Implementation Road Map for UzbekistanNo ratings yet

- Ifactransitiontoaccrual PDFDocument250 pagesIfactransitiontoaccrual PDFFryd PurabNo ratings yet

- CN 2021-0010Document84 pagesCN 2021-0010KrissaNo ratings yet

- IPSASB ED 47financial StatementsDocument48 pagesIPSASB ED 47financial StatementsMarian GrajdanNo ratings yet

- Basis-To-ed CF May 2015Document134 pagesBasis-To-ed CF May 2015studentul1986No ratings yet

- Ifric Update November 2015Document9 pagesIfric Update November 2015Neji HergliNo ratings yet

- (Latest) TOPIC 6 SPECIAL ISSUES IN FINANCIAL REPORTINGDocument65 pages(Latest) TOPIC 6 SPECIAL ISSUES IN FINANCIAL REPORTINGMuadz KamaruddinNo ratings yet

- ICAP TRsDocument45 pagesICAP TRsSyed Azhar Abbas0% (1)

- 5.6.9. ISA 710 Comparative Information DefDocument26 pages5.6.9. ISA 710 Comparative Information DefYessenia Elena Gonzalez MagallanesNo ratings yet

- Conceptual Framework Accounting SystemDocument13 pagesConceptual Framework Accounting SystemYes ChannelNo ratings yet

- SECTIONAL INDEX OF TECHNICAL RELEASESDocument37 pagesSECTIONAL INDEX OF TECHNICAL RELEASESHamza ShahidNo ratings yet

- ED SME ConclusionDocument49 pagesED SME ConclusionRadikaAqlanNo ratings yet

- IFRS 9 Financial InstrumentsDocument38 pagesIFRS 9 Financial Instrumentssaoodali1988No ratings yet

- HedgeAcct ED Dec10Document65 pagesHedgeAcct ED Dec10vdhienNo ratings yet

- FrameworkDocument3 pagesFrameworkVola AriNo ratings yet

- IPSAS 32 Service ConcessionDocument63 pagesIPSAS 32 Service ConcessionEmmaNo ratings yet

- The Conceptual Framework For Financial: ReportingDocument32 pagesThe Conceptual Framework For Financial: Reportingmoynul islamNo ratings yet

- 10th Iacc Workshop The Public Sector Committees Standards ProjectlDocument26 pages10th Iacc Workshop The Public Sector Committees Standards ProjectladriolibahNo ratings yet

- Ind AS Alert: Marching Towards Better Reporting StructureDocument1 pageInd AS Alert: Marching Towards Better Reporting StructureKAJALINo ratings yet

- IFRS 17 Presentation " Accounting Treatment": July 2020Document66 pagesIFRS 17 Presentation " Accounting Treatment": July 2020benslama amelNo ratings yet

- IFRS 17 Assets For Acquisition Cash Flows: Explanatory ReportDocument34 pagesIFRS 17 Assets For Acquisition Cash Flows: Explanatory ReportWubneh AlemuNo ratings yet

- IFRS Overview ConferenceDocument12 pagesIFRS Overview ConferenceYagnesh DesaiNo ratings yet

- Ipsas 5-Borrowing Costs: AcknowledgmentDocument13 pagesIpsas 5-Borrowing Costs: Acknowledgmentriska putri utamiNo ratings yet

- E-Technical Update Nov2009Document14 pagesE-Technical Update Nov2009Atif RehmanNo ratings yet

- Insurance ContractsDocument88 pagesInsurance ContractsrmonangpsphmuntheNo ratings yet

- 2003 PR On ImprovementsDocument6 pages2003 PR On ImprovementsKreshen ShunmugamNo ratings yet

- IPSASB CP - Elements Recognition Phase - 2Document68 pagesIPSASB CP - Elements Recognition Phase - 2Vaike ChrisNo ratings yet

- 1204 - Invitation To Comment DRAFT For SMEIG Review - Sanath FernandoDocument74 pages1204 - Invitation To Comment DRAFT For SMEIG Review - Sanath FernandoSanath FernandoNo ratings yet

- Iaasb Isa 810 RevisedDocument31 pagesIaasb Isa 810 RevisedGlenn TaduranNo ratings yet

- Iaasb Ed Isae 3420 - Pro FormasDocument40 pagesIaasb Ed Isae 3420 - Pro FormasSergio Iván Giraldo GarcíaNo ratings yet

- E-Technical Update Jan2010Document11 pagesE-Technical Update Jan2010shakiraliqureshiNo ratings yet

- ED-CON 8-Conceptual Framework For Financial Reporting-Chap 4Document48 pagesED-CON 8-Conceptual Framework For Financial Reporting-Chap 4Jairo Mendez MoraNo ratings yet

- ISA 320 and 450Document25 pagesISA 320 and 450Lara MaderazoNo ratings yet

- E TechnicalDocument6 pagesE Technicalkhurram_66No ratings yet

- Ap12c Ias16 Property Plant EquipmentDocument22 pagesAp12c Ias16 Property Plant EquipmentyoussefNo ratings yet

- 2021 Public Input Complete Monograph Revised 12-14-2021 Reduced File SizeIIDocument1,270 pages2021 Public Input Complete Monograph Revised 12-14-2021 Reduced File SizeIIRodel AlmohallasNo ratings yet

- 550PBE-IAS-12-Jan16-IASB-191466.1Document27 pages550PBE-IAS-12-Jan16-IASB-191466.1Onwuchekwa Chidi CalebNo ratings yet

- IASB Update - February 2010Document6 pagesIASB Update - February 2010JCPAJONo ratings yet

- ISA (UK and Ireland) 706 Revised October 2012Document14 pagesISA (UK and Ireland) 706 Revised October 2012Josiah MwashitaNo ratings yet

- Ias 39Document43 pagesIas 39The ProtectorNo ratings yet

- IAS 16 Part BDocument12 pagesIAS 16 Part BRohail HanifNo ratings yet

- Ifrspracticestatement1 130Document12 pagesIfrspracticestatement1 130TiNo ratings yet

- Fallback To IFRS 9 Financial Instruments 2012Document2 pagesFallback To IFRS 9 Financial Instruments 2012German ChavezNo ratings yet

- 1992 FIDIC Joint Venture AgreementDocument27 pages1992 FIDIC Joint Venture AgreementBabu Balu Babu100% (3)

- NCSR 9-InF.14 - Considerations On The Implementation Arrangement For OnboarDocument5 pagesNCSR 9-InF.14 - Considerations On The Implementation Arrangement For OnboarManish RawatNo ratings yet

- 26 International Financial Reporting StandardsDocument3 pages26 International Financial Reporting StandardsClyleo Eddard YoupaNo ratings yet

- IFRS 9 Financial Instruments GuideDocument70 pagesIFRS 9 Financial Instruments GuideJ. JimenezNo ratings yet

- Financial Instruments: International Financial Reporting Standard 9Document68 pagesFinancial Instruments: International Financial Reporting Standard 9elle868No ratings yet

- IMF Committee Meeting Focuses on Debt Statistics MethodsDocument7 pagesIMF Committee Meeting Focuses on Debt Statistics MethodsHichemBdiriNo ratings yet

- SP 1 - 2009 Economic Development Advisory Committee Work PlanDocument6 pagesSP 1 - 2009 Economic Development Advisory Committee Work Planlangleyrecord8339No ratings yet

- IFRS On Point - January 2021Document8 pagesIFRS On Point - January 2021Khoa PhanNo ratings yet

- 004 - Chapter 02 - Financial Reporting FrameworksDocument10 pages004 - Chapter 02 - Financial Reporting FrameworksHaris ButtNo ratings yet

- 2021-IPSASB-Handbook Vol-1 ENG Web SecureDocument626 pages2021-IPSASB-Handbook Vol-1 ENG Web SecureTESDA PasMakNo ratings yet

- Chapter 1 - Introduction To IFRSDocument4 pagesChapter 1 - Introduction To IFRSBahader AliNo ratings yet

- IAASB Exposure Draft Proposed ISA 240 Revised FraudDocument162 pagesIAASB Exposure Draft Proposed ISA 240 Revised FraudUmmar FarooqNo ratings yet

- 4122 PDFDocument32 pages4122 PDFRussel Jun PachesNo ratings yet

- IFRS On Point - March 2020Document12 pagesIFRS On Point - March 2020The geek CuestaNo ratings yet

- Training On: International Financial Reporting Standards (IFRS)Document54 pagesTraining On: International Financial Reporting Standards (IFRS)Yaqeeroo TubeNo ratings yet

- Introductory Chapters To Derivatives 2021Document127 pagesIntroductory Chapters To Derivatives 2021Blessmore Andrew ChikwavaNo ratings yet

- Market Regulations, Benchmarks, Value Growth Investors Etc 2021Document59 pagesMarket Regulations, Benchmarks, Value Growth Investors Etc 2021Blessmore Andrew ChikwavaNo ratings yet

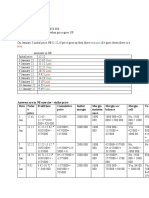

- Company Amount Invested (US$) Portfolio Allocation Returns (US$) Weighted ReturnsDocument5 pagesCompany Amount Invested (US$) Portfolio Allocation Returns (US$) Weighted ReturnsBlessmore Andrew ChikwavaNo ratings yet

- Risc MatrixDocument9 pagesRisc MatrixAlexNo ratings yet

- Group Assignment Q3Document5 pagesGroup Assignment Q3Blessmore Andrew ChikwavaNo ratings yet

- Individula AssignmentDocument2 pagesIndividula AssignmentBlessmore Andrew ChikwavaNo ratings yet

- Lecture 1: Introduction To Financial System and Its OverviewDocument64 pagesLecture 1: Introduction To Financial System and Its OverviewBlessmore Andrew ChikwavaNo ratings yet

- Lecture 8: Market Efficiency: Prof E. ZirambaDocument52 pagesLecture 8: Market Efficiency: Prof E. ZirambaBlessmore Andrew ChikwavaNo ratings yet

- Horticulture Zimbabwe: Updated June 2012Document8 pagesHorticulture Zimbabwe: Updated June 2012Blessmore Andrew ChikwavaNo ratings yet

- Relationship of Ethical Leadership, Corporate Social Responsibility and Organizational PerformanceDocument16 pagesRelationship of Ethical Leadership, Corporate Social Responsibility and Organizational PerformanceSneha Abhash SinghNo ratings yet

- Job Satisfaction and Problems Among Academic Sta in Higher EducationDocument38 pagesJob Satisfaction and Problems Among Academic Sta in Higher EducationBlessmore Andrew ChikwavaNo ratings yet

- Hedge Funds in Global Markets: An Analysis of Regulation and Systemic RiskDocument104 pagesHedge Funds in Global Markets: An Analysis of Regulation and Systemic RiskBlessmore Andrew ChikwavaNo ratings yet

- Disadvantages of Using BinomialDocument1 pageDisadvantages of Using BinomialBlessmore Andrew ChikwavaNo ratings yet

- The Outsourcing Handbook A Guide To Outsourcing PDFDocument62 pagesThe Outsourcing Handbook A Guide To Outsourcing PDFMikiKikiNo ratings yet

- Thomas Conkling ThesisDocument52 pagesThomas Conkling ThesisBlessmore Andrew ChikwavaNo ratings yet

- Technical AnalysisDocument1 pageTechnical AnalysisBlessmore Andrew ChikwavaNo ratings yet

- Study of The Impact of Team Morale On Construction Project PerforDocument45 pagesStudy of The Impact of Team Morale On Construction Project PerforBlessmore Andrew ChikwavaNo ratings yet

- Number 3Document2 pagesNumber 3Blessmore Andrew ChikwavaNo ratings yet

- PysparkDocument407 pagesPysparkAlejandro De LeonNo ratings yet

- Unit-5 Final AccountsDocument7 pagesUnit-5 Final AccountsSanthosh Santhu0% (1)

- VRIO AnalysisDocument2 pagesVRIO AnalysisrenjuannNo ratings yet

- Service Marketing of J&K BankDocument67 pagesService Marketing of J&K BankSubham ArenNo ratings yet

- Handwork Issue 4Document89 pagesHandwork Issue 4andrew_phelps100% (1)

- TABS Points System Implementing GuidelinesDocument8 pagesTABS Points System Implementing GuidelinesPortCallsNo ratings yet

- QUIZ 2-Mid.-Problems On Statement of Cash FlowsDocument2 pagesQUIZ 2-Mid.-Problems On Statement of Cash FlowsMonica GeronaNo ratings yet

- Intel To Enhance American Companies Competitiveness - Govt RoleDocument6 pagesIntel To Enhance American Companies Competitiveness - Govt RoleTrip KrantNo ratings yet

- Annual Report 2016 2017Document77 pagesAnnual Report 2016 2017Dream GoalNo ratings yet

- The Message Development Tool - A Case For Effective Operationalization of Messaging in Social Marketing PracticeDocument17 pagesThe Message Development Tool - A Case For Effective Operationalization of Messaging in Social Marketing PracticesanjayamalakasenevirathneNo ratings yet

- Stucor Chemba18 1Document8 pagesStucor Chemba18 1SELVAKUMAR SNo ratings yet

- Maintenance of Machinery & PlantsDocument22 pagesMaintenance of Machinery & PlantszeldotdotNo ratings yet

- Carlson School Corporate Investment Decisions Spring 2017Document12 pagesCarlson School Corporate Investment Decisions Spring 2017Novriani Tria PratiwiNo ratings yet

- Topic 6 - ADS 404 Chapter 6 2018Document25 pagesTopic 6 - ADS 404 Chapter 6 2018Nabil Azeem JehanNo ratings yet

- Doc Ssm.nurulhedayahDocument2 pagesDoc Ssm.nurulhedayahrezza590No ratings yet

- Salao SyllabusDocument22 pagesSalao SyllabusOtep de MesaNo ratings yet

- CEA Inspection Compliance Report SummaryDocument4 pagesCEA Inspection Compliance Report Summarykalyan ReddyNo ratings yet

- HR 2-Email DraftDocument4 pagesHR 2-Email DraftMallu SailajaNo ratings yet

- Schedule-H Contract Price WeightagesDocument20 pagesSchedule-H Contract Price Weightagesjalal100% (1)

- Certificate of Incorporation-20190704Document1 pageCertificate of Incorporation-20190704Pinky KumariNo ratings yet

- FAO Project ProfileDocument3 pagesFAO Project ProfileAbubakarr SesayNo ratings yet

- Corazza FB Series ENDocument4 pagesCorazza FB Series ENAbdullahNo ratings yet

- MBA Orientation Manual March 2021Document9 pagesMBA Orientation Manual March 2021SaranyaNo ratings yet

- BID FORM. Mun. of SaraDocument1 pageBID FORM. Mun. of Saravin arañoNo ratings yet

- Oracle® Iprocurement: Implementation and Administration Guide Release 12.2Document290 pagesOracle® Iprocurement: Implementation and Administration Guide Release 12.2Indumathi KumarNo ratings yet

- Industry Sources of Opportunities: Credit To:Mskrabbs19/Industrial-Sector-In-The-PhilippinesDocument34 pagesIndustry Sources of Opportunities: Credit To:Mskrabbs19/Industrial-Sector-In-The-PhilippinesdanieljudeeNo ratings yet

- CMT555 3 Pourbaix Diagrams Sem 4Document28 pagesCMT555 3 Pourbaix Diagrams Sem 4juaxxoNo ratings yet

- Para ImprimirDocument2 pagesPara ImprimirZymafayNo ratings yet

- Squatting LawsDocument3 pagesSquatting LawsRyan AcostaNo ratings yet

- Operators-Data-Sheet (Quezon City) PDFDocument3 pagesOperators-Data-Sheet (Quezon City) PDFGene JabonNo ratings yet

- How to get US Bank Account for Non US ResidentFrom EverandHow to get US Bank Account for Non US ResidentRating: 5 out of 5 stars5/5 (1)

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet

- Deduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesFrom EverandDeduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesRating: 3 out of 5 stars3/5 (3)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsFrom EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo ratings yet

- Bookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessFrom EverandBookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessRating: 5 out of 5 stars5/5 (5)

- Lower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderRating: 5 out of 5 stars5/5 (4)

- Taxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipFrom EverandTaxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipNo ratings yet

- What Everyone Needs to Know about Tax: An Introduction to the UK Tax SystemFrom EverandWhat Everyone Needs to Know about Tax: An Introduction to the UK Tax SystemNo ratings yet

- Invested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)From EverandInvested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)Rating: 4.5 out of 5 stars4.5/5 (43)

- The Hidden Wealth of Nations: The Scourge of Tax HavensFrom EverandThe Hidden Wealth of Nations: The Scourge of Tax HavensRating: 4 out of 5 stars4/5 (11)

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProFrom EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProRating: 4.5 out of 5 stars4.5/5 (43)

- Freight Broker Business Startup: Step-by-Step Guide to Start, Grow and Run Your Own Freight Brokerage Company In in Less Than 4 Weeks. Includes Business Plan TemplatesFrom EverandFreight Broker Business Startup: Step-by-Step Guide to Start, Grow and Run Your Own Freight Brokerage Company In in Less Than 4 Weeks. Includes Business Plan TemplatesRating: 5 out of 5 stars5/5 (1)

- Tax Accounting: A Guide for Small Business Owners Wanting to Understand Tax Deductions, and Taxes Related to Payroll, LLCs, Self-Employment, S Corps, and C CorporationsFrom EverandTax Accounting: A Guide for Small Business Owners Wanting to Understand Tax Deductions, and Taxes Related to Payroll, LLCs, Self-Employment, S Corps, and C CorporationsRating: 4 out of 5 stars4/5 (1)

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyFrom EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyRating: 4 out of 5 stars4/5 (52)

- Founding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationFrom EverandFounding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationNo ratings yet