You might also like

- Credit RationingDocument17 pagesCredit RationingLus PMwnkNo ratings yet

- Cooper RossDocument19 pagesCooper RossAndreea BorlanNo ratings yet

- FRIED & HOWITT, Credit Rationing and Implicit Contract TheoryDocument18 pagesFRIED & HOWITT, Credit Rationing and Implicit Contract TheoryAnonymous ykRTOENo ratings yet

- Why Banking Should RegulatedDocument11 pagesWhy Banking Should RegulatedAnggatelliNo ratings yet

- Credit Risk Models Par Robert A. JarrowDocument33 pagesCredit Risk Models Par Robert A. JarrowCJNo ratings yet

- Jaffee & Stiglitz, Credit RationingDocument52 pagesJaffee & Stiglitz, Credit RationingAnonymous ykRTOE100% (1)

- Bank Loan Supply and Corporate Capital StructureDocument44 pagesBank Loan Supply and Corporate Capital StructuremianzeeshanullahNo ratings yet

- A Theory and Test of Credit RationingDocument24 pagesA Theory and Test of Credit RationingEdson PrataNo ratings yet

- Theoretical Reflections On EndogenousDocument13 pagesTheoretical Reflections On EndogenousGrace LlerenaNo ratings yet

- Lending by Numbers Credit Scoring and The Constitution of Risk Within American Consumer CreditDocument32 pagesLending by Numbers Credit Scoring and The Constitution of Risk Within American Consumer CreditArjun RajanNo ratings yet

- Credit Rationing in Developing Countries:: An Overview of The TheoryDocument24 pagesCredit Rationing in Developing Countries:: An Overview of The TheorymitalptNo ratings yet

- Financial Intermediation and The Post-Crisis Financial SystemDocument32 pagesFinancial Intermediation and The Post-Crisis Financial SystemTina FrancisNo ratings yet

- Meltzer 1960meltzer 1960meltzer 1960meltzer 1960meltzer 1960meltzer 1960Document10 pagesMeltzer 1960meltzer 1960meltzer 1960meltzer 1960meltzer 1960meltzer 1960Karla PhamNo ratings yet

- This Content Downloaded From 196.47.134.59 On Fri, 06 May 2022 10:13:25 UTCDocument19 pagesThis Content Downloaded From 196.47.134.59 On Fri, 06 May 2022 10:13:25 UTCJules Daniel ElibiNo ratings yet

- Of Thumb in The Lending Market To Generate Exogenous Variation in The Ease ofDocument56 pagesOf Thumb in The Lending Market To Generate Exogenous Variation in The Ease ofShafi S.No ratings yet

- Association For Evolutionary Economics: Info/about/policies/terms - JSPDocument11 pagesAssociation For Evolutionary Economics: Info/about/policies/terms - JSPch0k3 iiiNo ratings yet

- J. Finan. Intermediation: Viral V. Acharya, Anjan V. ThakorDocument18 pagesJ. Finan. Intermediation: Viral V. Acharya, Anjan V. ThakorzerdnaNo ratings yet

- Michael Woodford 2010 Financial Intermediation and Macroeconomic AnalysisDocument25 pagesMichael Woodford 2010 Financial Intermediation and Macroeconomic AnalysisOscar Neira CuadraNo ratings yet

- The Arbitrage-Free Valuation and Hedging of Demand Deposits and Credit Card LoansDocument24 pagesThe Arbitrage-Free Valuation and Hedging of Demand Deposits and Credit Card LoansmahaNo ratings yet

- Bunk Runs, Deposit Insurance and LiquidityDocument19 pagesBunk Runs, Deposit Insurance and LiquidityGIMENEZ PUENTES MARIA PIANo ratings yet

- Tarekegn Literature PartDocument33 pagesTarekegn Literature ParttewodrosbayisaNo ratings yet

- Endogenous Credit CyclesDocument27 pagesEndogenous Credit CyclesJonas SiqueiraNo ratings yet

- Credit Channel PDFDocument45 pagesCredit Channel PDFSonia VivenyNo ratings yet

- Clearing Settlement and Monetary PolicyDocument30 pagesClearing Settlement and Monetary PolicyFlaviub23No ratings yet

- Real-Time Gross Settlement and The Costs of Immediacy: Charles M. Kahn and William RoberdsDocument30 pagesReal-Time Gross Settlement and The Costs of Immediacy: Charles M. Kahn and William RoberdsVenkatesh SangepuNo ratings yet

- 1# Managing Bank Liquidity Risk How Deposit-Loan Synergies Vary With Market ConditionsDocument35 pages1# Managing Bank Liquidity Risk How Deposit-Loan Synergies Vary With Market ConditionsYING DINGNo ratings yet

- 1 s2.0 S0378426619302778 MainDocument18 pages1 s2.0 S0378426619302778 Mainaldiyar.alimbekovNo ratings yet

- Exchange Rate N Financial Fragility - Eichengreen N HausmanDocument41 pagesExchange Rate N Financial Fragility - Eichengreen N HausmanAqilah Dhau' FarahnizarNo ratings yet

- Adrian-Colla-Shin - Which Financial Frictions (Parsing The Evidence From The Financial Crisis of 2007-9)Document54 pagesAdrian-Colla-Shin - Which Financial Frictions (Parsing The Evidence From The Financial Crisis of 2007-9)Chi-Wa CWNo ratings yet

- Sunderam Money Creation and The SBSDocument51 pagesSunderam Money Creation and The SBSMariano Cruz NavarroNo ratings yet

- When Is External Debt Sustainable - (The World Bank Economic Review, Vol. 20, Issue 3) (2006)Document25 pagesWhen Is External Debt Sustainable - (The World Bank Economic Review, Vol. 20, Issue 3) (2006)tieutrieudaolinh1309No ratings yet

- Article 7Document24 pagesArticle 7Anjali Devi AnjuNo ratings yet

- 3qep3 Intraday CreditDocument16 pages3qep3 Intraday CreditFlaviub23No ratings yet

- Creditworthiness and Thresholds in A Credit Market Model With Multiple EquilibriaDocument35 pagesCreditworthiness and Thresholds in A Credit Market Model With Multiple EquilibriarrrrrrrrNo ratings yet

- TOBIN - Liquidity Preference As Behavior Towards RiskDocument23 pagesTOBIN - Liquidity Preference As Behavior Towards RiskLujan GNo ratings yet

- SSRN Id3044087Document33 pagesSSRN Id3044087Santiago RamirezNo ratings yet

- Wallace (1988) - SS Taking SeriouslyDocument16 pagesWallace (1988) - SS Taking SeriouslyThiago Leitao RibeiroNo ratings yet

- (Lehman Brothers) Quantitative Credit Research Quarterly - Quarter 3 2001Document44 pages(Lehman Brothers) Quantitative Credit Research Quarterly - Quarter 3 2001anuragNo ratings yet

- Secured Lending and Borrowers' RiskinessDocument31 pagesSecured Lending and Borrowers' RiskinessHOA DAONo ratings yet

- Credit Crunch, Bank Lending, and Monetary Policy: A Model of Financial Intermediation With Heterogeneous ProjectsDocument27 pagesCredit Crunch, Bank Lending, and Monetary Policy: A Model of Financial Intermediation With Heterogeneous ProjectsAgus Heri HoerudinNo ratings yet

- Tarekegn LiteratureDocument25 pagesTarekegn LiteraturetewodrosbayisaNo ratings yet

- From Basel I To Basel II To Basel IIIDocument5 pagesFrom Basel I To Basel II To Basel IIIOmair KhalidNo ratings yet

- Public Debt, Bank Debt, and Non-Bank Private Debt in Emerging and Developed Financial MarketsDocument8 pagesPublic Debt, Bank Debt, and Non-Bank Private Debt in Emerging and Developed Financial MarketsRiska Ayu SetiawatiNo ratings yet

- Agency Problems, Screening and Increasing Credit LinesDocument41 pagesAgency Problems, Screening and Increasing Credit LinesBen ShionNo ratings yet

- Reflexivity in Credit MarketsDocument43 pagesReflexivity in Credit MarketsMax MysterioNo ratings yet

- Credit Risk Modelling A Wheel of Risk Ma PDFDocument9 pagesCredit Risk Modelling A Wheel of Risk Ma PDFPia CallantaNo ratings yet

- This Content Downloaded From 140.213.59.20 On Sun, 13 Sep 2020 09:17:59 UTCDocument20 pagesThis Content Downloaded From 140.213.59.20 On Sun, 13 Sep 2020 09:17:59 UTCprasnaNo ratings yet

- SAMPLE Assignment Sub Prime Financial Crisis 2008Document4 pagesSAMPLE Assignment Sub Prime Financial Crisis 2008scholarsassistNo ratings yet

- FI EssaysDocument34 pagesFI EssaysAnna KucherukNo ratings yet

- Berger, A., & Bouwman, C. (2009) .Document59 pagesBerger, A., & Bouwman, C. (2009) .Vita NataliaNo ratings yet

- Credit Cycles, Credit Risk, and Prudential Regulation: Gabriel Jim Enez and Jes Us SaurinaDocument34 pagesCredit Cycles, Credit Risk, and Prudential Regulation: Gabriel Jim Enez and Jes Us SaurinaamotpizNo ratings yet

- Building A Credit Risk ValuationDocument26 pagesBuilding A Credit Risk ValuationMazen AlbsharaNo ratings yet

- Credit Default Swaps - LawJournalDocument40 pagesCredit Default Swaps - LawJournalMark MehnerNo ratings yet

- Cooper 2015 - Shadow Money and The Shadow WorkforceDocument30 pagesCooper 2015 - Shadow Money and The Shadow Workforceanton.de.rotaNo ratings yet

- Essays UOLs FIDocument34 pagesEssays UOLs FIAnna KucherukNo ratings yet

- Vultures or Vanguards - The Role of Litigation in Sovereign DebtDocument71 pagesVultures or Vanguards - The Role of Litigation in Sovereign DebtCanhuiNo ratings yet

- Post Keynesian Monetary Theory Some IssuDocument26 pagesPost Keynesian Monetary Theory Some Issurribeiro70No ratings yet

- An Assessment of The Credit Rating Agencies: Background, Analysis, and PolicyDocument68 pagesAn Assessment of The Credit Rating Agencies: Background, Analysis, and PolicyMercatus Center at George Mason UniversityNo ratings yet

- Material Adverse Change Clauses: Decoding A Legal EnigmaDocument6 pagesMaterial Adverse Change Clauses: Decoding A Legal Enigmahariom bajpaiNo ratings yet

- Beyond DSGE Models, David Colander Et AlDocument5 pagesBeyond DSGE Models, David Colander Et AlDavid ArevalosNo ratings yet

- Steve Keen - Macroeconomics Does Not Need Microeconomic FoundationsDocument10 pagesSteve Keen - Macroeconomics Does Not Need Microeconomic FoundationsDavid ArevalosNo ratings yet

- Students Survey 2002 ReportDocument86 pagesStudents Survey 2002 ReportDavid ArevalosNo ratings yet

- David (2007) Path Dependence A Foundational Concept For Historical Social ScienceDocument24 pagesDavid (2007) Path Dependence A Foundational Concept For Historical Social ScienceDavid ArevalosNo ratings yet

- Networks An Economic PerspectiveDocument40 pagesNetworks An Economic PerspectiveDavid ArevalosNo ratings yet

- W. Brian Arthur Positive Feedbacks in The EconomyDocument12 pagesW. Brian Arthur Positive Feedbacks in The EconomyDavid ArevalosNo ratings yet

- Antonelli (2009) The Economics of Innovation From The Classical Legacies To The Economics of ComplexityDocument36 pagesAntonelli (2009) The Economics of Innovation From The Classical Legacies To The Economics of ComplexityDavid ArevalosNo ratings yet

- Deficits and Cycles : Ricer FarmerDocument12 pagesDeficits and Cycles : Ricer FarmerDavid ArevalosNo ratings yet

- Xie (2019) The Paradigm Crisis of Modern Mainstream EconomicsDocument12 pagesXie (2019) The Paradigm Crisis of Modern Mainstream EconomicsDavid ArevalosNo ratings yet

- Did Austrian Economists Predict The Financial Crisis?, Dante A. UrbinaDocument15 pagesDid Austrian Economists Predict The Financial Crisis?, Dante A. UrbinaDavid Arevalos100% (1)

- Orthodox Monetary Theory: A Critique From PostKeynesianism and Transfinancial Economics, Dante A. UrbinaDocument10 pagesOrthodox Monetary Theory: A Critique From PostKeynesianism and Transfinancial Economics, Dante A. UrbinaDavid Arevalos100% (1)

- SBI Clerk Prelims Previous Year Paper 2018Document14 pagesSBI Clerk Prelims Previous Year Paper 2018Caroline JuliyatNo ratings yet

- Chapter 2Document18 pagesChapter 2FakeMe12No ratings yet

- Perkembangan Kebun Teh Danau Kembar Dari Tahun 2000 - 2017.Document12 pagesPerkembangan Kebun Teh Danau Kembar Dari Tahun 2000 - 2017.niaputriNo ratings yet

- AOW2 2018 Post Show ReportDocument3 pagesAOW2 2018 Post Show ReportEmekaVictorOnyekwereNo ratings yet

- Fund UtilizationDocument3 pagesFund Utilizationbarangay kuyaNo ratings yet

- A Brief Analysis On The Labor Pay of Government Employed Registered Nurses (RN) in The PhilippinesDocument3 pagesA Brief Analysis On The Labor Pay of Government Employed Registered Nurses (RN) in The PhilippinesMary Joy Catherine RicasioNo ratings yet

- (MP) Platinum Ex Factory Price ListDocument1 page(MP) Platinum Ex Factory Price ListSaurabh JainNo ratings yet

- Traffic and Highway Engineering 5th Edition Garber Solutions ManualDocument27 pagesTraffic and Highway Engineering 5th Edition Garber Solutions Manualsorrancemaneuverpmvll100% (32)

- Managing People in Global Markets-The Asia Pacific PerspectiveDocument4 pagesManaging People in Global Markets-The Asia Pacific PerspectiveHaniyah NadhiraNo ratings yet

- Draft LA Ghana Country Study, En-1Document35 pagesDraft LA Ghana Country Study, En-1agyenimboatNo ratings yet

- An Iot Based Dam Water Management System For AgricultureDocument21 pagesAn Iot Based Dam Water Management System For AgriculturemathewsNo ratings yet

- Full Download Business in Action 6th Edition Bovee Solutions ManualDocument35 pagesFull Download Business in Action 6th Edition Bovee Solutions Manuallincolnpatuc8100% (32)

- Reliability Evaluation of Grid-Connected Photovoltaic Power SystemsDocument32 pagesReliability Evaluation of Grid-Connected Photovoltaic Power Systemssamsai88850% (2)

- TeslaDocument20 pagesTeslaArpit Singh100% (1)

- MKT 465 ch2 SehDocument51 pagesMKT 465 ch2 SehNaimul KaderNo ratings yet

- Cir V SLMC DigestDocument3 pagesCir V SLMC DigestYour Public ProfileNo ratings yet

- List of Industries PackingDocument6 pagesList of Industries PackingRavichandran SNo ratings yet

- Gold and InflationDocument25 pagesGold and InflationRaghu.GNo ratings yet

- Analysis of Monetary Policy of IndiaDocument18 pagesAnalysis of Monetary Policy of IndiaShashwat TiwariNo ratings yet

- Bank - A Financial Institution Licensed To Receive Deposits and Make Loans. Banks May AlsoDocument3 pagesBank - A Financial Institution Licensed To Receive Deposits and Make Loans. Banks May AlsoKyle PanlaquiNo ratings yet

- Chapter 18Document16 pagesChapter 18Norman DelirioNo ratings yet

- Rec Max VS Opt AltDocument4 pagesRec Max VS Opt AltAloka RanasingheNo ratings yet

- Chapter 7 - Valuation and Characteristics of Bonds KEOWNDocument9 pagesChapter 7 - Valuation and Characteristics of Bonds KEOWNKeeZan Lim100% (1)

- 11th 12th Economics Q EM Sample PagesDocument27 pages11th 12th Economics Q EM Sample PagesKirthika RajaNo ratings yet

- Equilibrium of FirmDocument1 pageEquilibrium of Firmkamran-naqviNo ratings yet

- Chapter 6Document32 pagesChapter 6John Rick DayondonNo ratings yet

- The United States Edition of Marketing Management, 14e. 1-1Document133 pagesThe United States Edition of Marketing Management, 14e. 1-1Tauhid Ahmed BappyNo ratings yet

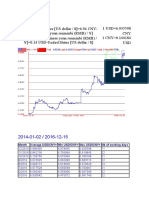

- Month Average USD/CNY Min USD/CNY Max USD/CNY NB of Working DaysDocument3 pagesMonth Average USD/CNY Min USD/CNY Max USD/CNY NB of Working DaysZahid RizvyNo ratings yet

- Module 1 GE 4 (Contemporary World)Document84 pagesModule 1 GE 4 (Contemporary World)MARY MAXENE CAMELON BITARANo ratings yet

- Chapter 6 MCQDocument3 pagesChapter 6 MCQnurul amiraNo ratings yet

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (15)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineFrom EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNo ratings yet

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsFrom EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsRating: 5 out of 5 stars5/5 (1)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- The Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingFrom EverandThe Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingRating: 4.5 out of 5 stars4.5/5 (760)

- Project Control Methods and Best Practices: Achieving Project SuccessFrom EverandProject Control Methods and Best Practices: Achieving Project SuccessNo ratings yet

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsFrom EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNo ratings yet

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeFrom EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeRating: 4 out of 5 stars4/5 (21)

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCFrom EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCRating: 5 out of 5 stars5/5 (1)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItFrom EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItRating: 4.5 out of 5 stars4.5/5 (14)

- Your Amazing Itty Bitty(R) Personal Bookkeeping BookFrom EverandYour Amazing Itty Bitty(R) Personal Bookkeeping BookNo ratings yet

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessFrom EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessRating: 4.5 out of 5 stars4.5/5 (28)

- CDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsFrom EverandCDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsRating: 4 out of 5 stars4/5 (4)

- Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetFrom EverandRatio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetRating: 4.5 out of 5 stars4.5/5 (14)