You might also like

- Legal OpinionDocument8 pagesLegal OpinionEvin Megallon VillarubenNo ratings yet

- STP Formatting Guide 010707Document2 pagesSTP Formatting Guide 010707yeuhqhNo ratings yet

- Impact of Unethical Practices On Business Environment: A Case Study On ToyotaDocument7 pagesImpact of Unethical Practices On Business Environment: A Case Study On ToyotaWasifNo ratings yet

- Carriage of Goods LiabilityDocument1 pageCarriage of Goods LiabilityAlexPamintuanAbitanNo ratings yet

- FAA Order 8900.1 CHG 218Document5 pagesFAA Order 8900.1 CHG 218Muhammad Ashraful KabirNo ratings yet

- As 2049-2002 Roof TilesDocument7 pagesAs 2049-2002 Roof TilesSAI Global - APAC0% (1)

- Auditing Test Bank Ch1Document34 pagesAuditing Test Bank Ch1Rosvel Esquillo95% (21)

- Ebcl Dec 2021 25102021Document96 pagesEbcl Dec 2021 25102021khushi jaiswalNo ratings yet

- Foreign Contribution Regulation Rules 2011Document6 pagesForeign Contribution Regulation Rules 2011Latest Laws TeamNo ratings yet

- FAQs on Foreign Contributions RegulationsDocument10 pagesFAQs on Foreign Contributions RegulationsrkhariNo ratings yet

- TDS Not DeductDocument6 pagesTDS Not DeductAnil WayanadNo ratings yet

- The Companies Act, 1956: 211. Form and Contents of Balance-Sheet and Profit and Loss Account.Document10 pagesThe Companies Act, 1956: 211. Form and Contents of Balance-Sheet and Profit and Loss Account.Paul ArijitNo ratings yet

- It ProvisionDocument10 pagesIt Provisionvkailash12No ratings yet

- Tax Law Guide to Indian Income TaxDocument133 pagesTax Law Guide to Indian Income TaxTahaNo ratings yet

- Section 16Document17 pagesSection 16d-fbuser-65596417No ratings yet

- B.-Deductions in Respect of Certain Payments: Section 10Document4 pagesB.-Deductions in Respect of Certain Payments: Section 10Babu GupthaNo ratings yet

- Ministry of Corporate Affairs Publishes New LLP RulesDocument169 pagesMinistry of Corporate Affairs Publishes New LLP RulesshankarvittaNo ratings yet

- Income Tax Department 80cDocument6 pagesIncome Tax Department 80cSrikanth SuryaNo ratings yet

- UntitledDocument92 pagesUntitledPawandeep SinghNo ratings yet

- Advance Ruling: 14.1 Definitions (Section 28E)Document5 pagesAdvance Ruling: 14.1 Definitions (Section 28E)timirkantaNo ratings yet

- FC Faq 07062019 PDFDocument20 pagesFC Faq 07062019 PDFsandeep kulhariaNo ratings yet

- CA Inter Law Amendments May 2021Document3 pagesCA Inter Law Amendments May 2021Soul of honeyNo ratings yet

- FCRA RegulationsDocument3 pagesFCRA RegulationsAhona MukherjeeNo ratings yet

- Senate Bill No. - : Senate of The PhilippinesDocument13 pagesSenate Bill No. - : Senate of The PhilippinesAizaLizaNo ratings yet

- Foreign Contribution (Regulation) Act, 2010Document66 pagesForeign Contribution (Regulation) Act, 2010Karthik RamasamyNo ratings yet

- Explanation.-For The Purposes of This SectionDocument2 pagesExplanation.-For The Purposes of This SectionJeremy RemlalfakaNo ratings yet

- 25RMA Act 2010Document130 pages25RMA Act 2010Nyingtob Pema NorbuNo ratings yet

- Sec 194aDocument3 pagesSec 194asayanghosh55No ratings yet

- CTPMDocument28 pagesCTPMIndu Shekhar PoddarNo ratings yet

- Tax Updates For December 2011 31 10 2011Document35 pagesTax Updates For December 2011 31 10 2011gangadhardaNo ratings yet

- Tax Updates For December 2011 31 10 2011Document35 pagesTax Updates For December 2011 31 10 2011Rakhi ChaubeyNo ratings yet

- Fra Act 2015 EnglishDocument24 pagesFra Act 2015 EnglishMohammad FaridNo ratings yet

- Union Budget 2013-14 - Highlights of Direct Tax ProposalsDocument5 pagesUnion Budget 2013-14 - Highlights of Direct Tax Proposalsankit403No ratings yet

- Form For Application For Grant of Licence To Be A Certifying AuthorityDocument19 pagesForm For Application For Grant of Licence To Be A Certifying AuthorityAppy Gowda GNo ratings yet

- Value Added Tax Act AmendmentsDocument42 pagesValue Added Tax Act AmendmentsJamie ReyesNo ratings yet

- The Foreign Contribution (Regulation) Act, 2010: by The End of This Chapter, You Will Be Able ToDocument44 pagesThe Foreign Contribution (Regulation) Act, 2010: by The End of This Chapter, You Will Be Able ToDimple KhandheriaNo ratings yet

- Basic Concepts of Income Tax ExplainedDocument47 pagesBasic Concepts of Income Tax Explainedleela naga janaki rajitha attiliNo ratings yet

- Amendments Applicable For Nov 2018 Exam: Income TaxDocument4 pagesAmendments Applicable For Nov 2018 Exam: Income TaxKrishna DasNo ratings yet

- 93FCR0107FLDocument12 pages93FCR0107FLPrasad NayakNo ratings yet

- Chapter VIII Rebates and ReliefsDocument14 pagesChapter VIII Rebates and ReliefsShweta VermaNo ratings yet

- Provident Fund, Subscription To Certain Equity Shares or Debentures, Etc. 80CDocument6 pagesProvident Fund, Subscription To Certain Equity Shares or Debentures, Etc. 80CSteven SpencerNo ratings yet

- AssetsDocument7 pagesAssetsNidhi YadavNo ratings yet

- Section 194Document10 pagesSection 194Hitesh NarwaniNo ratings yet

- Income Tax ActDocument50 pagesIncome Tax ActMahesh NaikNo ratings yet

- Companies (Acceptance of Deposits) Rules 2014Document14 pagesCompanies (Acceptance of Deposits) Rules 2014PratyakshaNo ratings yet

- Sales Tax Act, 1990 (Amended-Upto-01!07!2021)Document271 pagesSales Tax Act, 1990 (Amended-Upto-01!07!2021)Taimur RahmanNo ratings yet

- Explanation.-The Provisions of This Paragraph Shall Not Apply in The Case of A Non-GovernmentDocument9 pagesExplanation.-The Provisions of This Paragraph Shall Not Apply in The Case of A Non-GovernmentAl Amin SarkarNo ratings yet

- Regulating and Promoting the Insurance IndustryDocument5 pagesRegulating and Promoting the Insurance IndustrytahirhotagiNo ratings yet

- Service Tax Rules, 1994Document75 pagesService Tax Rules, 1994Gens GeorgeNo ratings yet

- Companies Act dividend declaration rulesDocument10 pagesCompanies Act dividend declaration rulesSidharthNo ratings yet

- The Payment of Bonus Act 1965Document8 pagesThe Payment of Bonus Act 1965Abhishek ShahNo ratings yet

- ITR's and AssessmentDocument11 pagesITR's and Assessmentashutosh4iipmNo ratings yet

- ICDR Guidelines - IGP - April 05 2019Document6 pagesICDR Guidelines - IGP - April 05 2019Srishti 2k22No ratings yet

- 209A. (1) (I) (Ii)Document29 pages209A. (1) (I) (Ii)Manoj NamdevNo ratings yet

- Inherent Limitations On The Power of TaxationDocument6 pagesInherent Limitations On The Power of TaxationEdwin Villegas de NicolasNo ratings yet

- THE INDUSTRIAL DEVELOPMENT AND REGULATION ACT 1951Document6 pagesTHE INDUSTRIAL DEVELOPMENT AND REGULATION ACT 1951Dakshata GadiyaNo ratings yet

- (C) "Government Company" Means A Company in Which Not Less Than Fifty-One Per CentDocument34 pages(C) "Government Company" Means A Company in Which Not Less Than Fifty-One Per CentArvind SarafNo ratings yet

- GST RefundsDocument26 pagesGST RefundsMuskan SharmaNo ratings yet

- Income Tax Act, 1961Document13 pagesIncome Tax Act, 1961Sanketh_Surey_6489No ratings yet

- GST Update130 PDFDocument3 pagesGST Update130 PDFTharun RajNo ratings yet

- Income Deemed To Accrue or Arise in IndiaDocument12 pagesIncome Deemed To Accrue or Arise in IndiaSuryaNo ratings yet

- Revenue Regulations No. 07-10 - Implementing The Tax Privileges Provisions of Republic Act No. 9994 (Expanded Senior Citizens Act of 2010)Document13 pagesRevenue Regulations No. 07-10 - Implementing The Tax Privileges Provisions of Republic Act No. 9994 (Expanded Senior Citizens Act of 2010)Cuayo JuicoNo ratings yet

- Section 139 - Return of incomeDocument7 pagesSection 139 - Return of incomeAnand LakraNo ratings yet

- The Following Clause 10 (D) of Section 10 by The Finance Act, 2003, W.E.F. 1-4-2004Document10 pagesThe Following Clause 10 (D) of Section 10 by The Finance Act, 2003, W.E.F. 1-4-2004120133No ratings yet

- EnglishDocument90 pagesEnglishsanjaifromusaNo ratings yet

- Export Guidelines in Nigeria PDFDocument6 pagesExport Guidelines in Nigeria PDFetohNo ratings yet

- Custom House AgentsDocument13 pagesCustom House AgentsMurali MohanNo ratings yet

- Et Iso 605 2001 PDFDocument10 pagesEt Iso 605 2001 PDFgabisoNo ratings yet

- DILG Region XII issues order on attendance to Seal of Good Local Governance trainingDocument3 pagesDILG Region XII issues order on attendance to Seal of Good Local Governance trainingJadelyn Bernadas CabAhugNo ratings yet

- 26 Filipinas CIA. de Seguros, Et Al. vs. MandanasDocument13 pages26 Filipinas CIA. de Seguros, Et Al. vs. MandanasGia DimayugaNo ratings yet

- Verified ComplaintDocument18 pagesVerified Complaintsmayer@howardrice.comNo ratings yet

- Department of Labor: fs17c AdministrativeDocument3 pagesDepartment of Labor: fs17c AdministrativeUSA_DepartmentOfLaborNo ratings yet

- Long Quiz ReviewDocument6 pagesLong Quiz ReviewCamille BagadiongNo ratings yet

- LABOR STANDARDS WAGESDocument1 pageLABOR STANDARDS WAGESInna De LeonNo ratings yet

- 1 Basic Electrical Safety SafetycorDocument2 pages1 Basic Electrical Safety SafetycorHendri Agustinus KollyNo ratings yet

- US Army Camouflage Improvement Effort SolicitationDocument67 pagesUS Army Camouflage Improvement Effort SolicitationsolsysNo ratings yet

- Success Stories by Girls Entrepreneurs NigeriaqravlDocument2 pagesSuccess Stories by Girls Entrepreneurs Nigeriaqravlspiderteller7No ratings yet

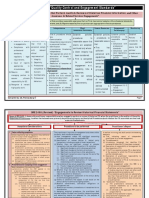

- Chapter 1 "Quality Control and Engagement Standards"Document8 pagesChapter 1 "Quality Control and Engagement Standards"Raul KarkyNo ratings yet

- ProspectusDocument8 pagesProspectusshanumanuranu100% (1)

- 19 - Pboap Vs DoleDocument17 pages19 - Pboap Vs DoleMia AdlawanNo ratings yet

- Victoriano V Elizalde Rope Workers UnionDocument9 pagesVictoriano V Elizalde Rope Workers UnionCyndi OrolfoNo ratings yet

- Directors Duties: Skip To Primary Content Skip To Secondary ContentDocument4 pagesDirectors Duties: Skip To Primary Content Skip To Secondary ContentHimal AcharyaNo ratings yet

- Chapter 3Document54 pagesChapter 3koushik kumarNo ratings yet

- US Department of Justice Official Release - 02062-06 Tax 802Document2 pagesUS Department of Justice Official Release - 02062-06 Tax 802legalmattersNo ratings yet

- LTR SupplyDocument2 pagesLTR Supplyanon_919994949No ratings yet

- Business Licence Bylaw No. 3328Document14 pagesBusiness Licence Bylaw No. 3328BillMetcalfeNo ratings yet

- MV Registration VehicleDocument3 pagesMV Registration VehicleKhak UsNo ratings yet

- BECG Reckoner - MBA GTUDocument115 pagesBECG Reckoner - MBA GTUsorathia jignesh100% (2)