You might also like

- NHAI Updated ResearchDocument1 pageNHAI Updated Researchkumar kartikeyaNo ratings yet

- Kluwer International Tax Blog: "Global Minimum Tax: A Game Changer?"Document11 pagesKluwer International Tax Blog: "Global Minimum Tax: A Game Changer?"kumar kartikeyaNo ratings yet

- Hydrographic Surveying in Exclusive Economic Zones: Jurisdictional IssuesDocument10 pagesHydrographic Surveying in Exclusive Economic Zones: Jurisdictional Issueskumar kartikeyaNo ratings yet

- Tax Computation FY 2020-21Document9 pagesTax Computation FY 2020-21kumar kartikeyaNo ratings yet

- SSRN Id1546242Document42 pagesSSRN Id1546242kumar kartikeyaNo ratings yet

- SemIII-C 87 CG-I Kumarkartikeya ProjectDocument18 pagesSemIII-C 87 CG-I Kumarkartikeya Projectkumar kartikeyaNo ratings yet

- Company Law 1Document3 pagesCompany Law 1kumar kartikeyaNo ratings yet

- Index: SEMESTER VI - B.A.LL.B. (Hons.) Syllabus (Session: Jan-June)Document48 pagesIndex: SEMESTER VI - B.A.LL.B. (Hons.) Syllabus (Session: Jan-June)kumar kartikeyaNo ratings yet

- Modes of Acquisition Under International LawDocument12 pagesModes of Acquisition Under International Lawkumar kartikeyaNo ratings yet

- Tax Sace 1Document13 pagesTax Sace 1kumar kartikeyaNo ratings yet

- Election Method of The PresidentDocument5 pagesElection Method of The Presidentkumar kartikeyaNo ratings yet

- The Indian Legal SystemDocument5 pagesThe Indian Legal Systemkumar kartikeyaNo ratings yet

- LLP Agreement - Shreya SinghDocument20 pagesLLP Agreement - Shreya Singhkumar kartikeyaNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Genocide at The Dawn of 21st C - Rwanda, Bosnia, Kosovo, and Darfur PDFDocument305 pagesGenocide at The Dawn of 21st C - Rwanda, Bosnia, Kosovo, and Darfur PDFjeffNo ratings yet

- United States v. Aaron Gomes, 387 F.3d 157, 2d Cir. (2004)Document8 pagesUnited States v. Aaron Gomes, 387 F.3d 157, 2d Cir. (2004)Scribd Government DocsNo ratings yet

- FranchisingDocument36 pagesFranchisingMukesh Raj PurohitNo ratings yet

- Filing of F.I.R Assignment: Amit Grover A3221515130 Bba LL.B (H) Section B 2015-20Document7 pagesFiling of F.I.R Assignment: Amit Grover A3221515130 Bba LL.B (H) Section B 2015-20Amit GroverNo ratings yet

- Frequently Asked Questions: On Adoption in Indian - LawDocument8 pagesFrequently Asked Questions: On Adoption in Indian - LawIshaNo ratings yet

- City of Iriga V CASURECO IIIDocument3 pagesCity of Iriga V CASURECO IIIJerico GodoyNo ratings yet

- Role of Lokpal and Lokyukta in India Redressal of PublicDocument14 pagesRole of Lokpal and Lokyukta in India Redressal of Publictayyaba redaNo ratings yet

- COMPLAINT SHEET BLANK - EditedDocument1 pageCOMPLAINT SHEET BLANK - EditedRyan Dela CruzNo ratings yet

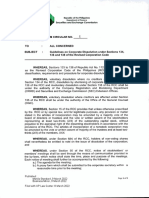

- SEC Dissolution GuidelinesDocument9 pagesSEC Dissolution GuidelinesErwin BautistaNo ratings yet

- All Constitution Q&ADocument57 pagesAll Constitution Q&APranjal PragyaNo ratings yet

- Valdez, People V LarranagaDocument4 pagesValdez, People V LarranagaAnonymous b80BEURy8No ratings yet

- Statcon CasesDocument22 pagesStatcon CasesJoahnna Paula CorpuzNo ratings yet

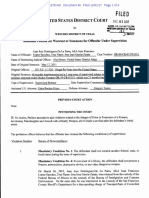

- US Supreme Court Writ For CertiorariDocument58 pagesUS Supreme Court Writ For CertiorariNausheen ZainulabeddinNo ratings yet

- BUS 305 Midterm 1 ReviewDocument4 pagesBUS 305 Midterm 1 ReviewbobNo ratings yet

- The Rise of Extra-Legal RemediesDocument3 pagesThe Rise of Extra-Legal Remediesem corderoNo ratings yet

- Eduarte vs. Court of Appeals, 253 SCRA 391, February 09, 1996Document15 pagesEduarte vs. Court of Appeals, 253 SCRA 391, February 09, 1996Kath ONo ratings yet

- Sample Memo To EmployeesDocument3 pagesSample Memo To EmployeesJudith Tito Bularon100% (2)

- People vs. EstebiaDocument5 pagesPeople vs. EstebiaAdrianne BenignoNo ratings yet

- Garcia Zarate AMMENDED Arrest WarrantDocument4 pagesGarcia Zarate AMMENDED Arrest WarrantSyndicated NewsNo ratings yet

- Oath of Office (SSG)Document3 pagesOath of Office (SSG)sirpencilbox89% (19)

- Civil Law Reviewer QuestionsDocument230 pagesCivil Law Reviewer QuestionsStrawber Ry100% (2)

- Direct Credit Facility Form: Important NotesDocument1 pageDirect Credit Facility Form: Important NotesOrange HazelNo ratings yet

- United States v. Shively, 10th Cir. (2001)Document6 pagesUnited States v. Shively, 10th Cir. (2001)Scribd Government DocsNo ratings yet

- In Re Brooks, 1 Phil., 55, November 05, 1901Document2 pagesIn Re Brooks, 1 Phil., 55, November 05, 1901Campbell HezekiahNo ratings yet

- TEDx Speaker Release 080916Document3 pagesTEDx Speaker Release 080916ZasaliveNo ratings yet

- Intestate Estate of Don Mariano San Pedro v. Court of Appeals, GR No. 103727, Dec. 1, 1996Document3 pagesIntestate Estate of Don Mariano San Pedro v. Court of Appeals, GR No. 103727, Dec. 1, 1996Jamiah Obillo HulipasNo ratings yet

- Case Stated Freedom of Information RedactDocument35 pagesCase Stated Freedom of Information RedactGotnitNo ratings yet

- Exclusive Patent License Agreement Between Alliance For Sustainable Energy, LLC andDocument19 pagesExclusive Patent License Agreement Between Alliance For Sustainable Energy, LLC andPOOJA AGARWALNo ratings yet

- ACI PHILIPPINES, INC. V COQUIADocument1 pageACI PHILIPPINES, INC. V COQUIAChilzia RojasNo ratings yet

- Flores V Esteban and Samson V YatCvil LawcoDocument2 pagesFlores V Esteban and Samson V YatCvil LawcoymaguindraNo ratings yet