You might also like

- Inventory Excel TemplateDocument9 pagesInventory Excel TemplateFail PelajarNo ratings yet

- Business Analytics Using SASDocument117 pagesBusiness Analytics Using SASsujit9100% (5)

- Share Based Compensation Share Based Compensation: Accounting (Mapua University) Accounting (Mapua University)Document6 pagesShare Based Compensation Share Based Compensation: Accounting (Mapua University) Accounting (Mapua University)Peri Babs100% (1)

- Loan Default Risk Assessment Using Supervised LearningDocument7 pagesLoan Default Risk Assessment Using Supervised LearningInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- (Original For Recipient) : Sl. No Description Unit Price Discount Qty Net Amount Tax Rate Tax Type Tax Amount Total AmountDocument1 page(Original For Recipient) : Sl. No Description Unit Price Discount Qty Net Amount Tax Rate Tax Type Tax Amount Total Amountsrikanth121No ratings yet

- A Data Mining Approach To Predict Prospective Business Sectors For Lending in Retail Banking Using Decision TreeDocument10 pagesA Data Mining Approach To Predict Prospective Business Sectors For Lending in Retail Banking Using Decision TreeLewis TorresNo ratings yet

- Get PDF 1Document4 pagesGet PDF 1Poorni BablooNo ratings yet

- The Value of Big Data For Credit Scoring: Enhancing Financial Inclusion Using Mobile Phone Data and Social Network AnalyticsDocument36 pagesThe Value of Big Data For Credit Scoring: Enhancing Financial Inclusion Using Mobile Phone Data and Social Network AnalyticsMabociv NabajinNo ratings yet

- Predicting The Probability of Bank Deposit SubscriptionDocument4 pagesPredicting The Probability of Bank Deposit SubscriptionIJRASETPublicationsNo ratings yet

- Dissertation Presentation Bidyut MondalDocument22 pagesDissertation Presentation Bidyut MondalRano JoyNo ratings yet

- Literature Review On Banking TechnologyDocument4 pagesLiterature Review On Banking Technologyafmzfxfaalkjcj100% (1)

- Derive A Customer Relationship Strategy For A Marketer Supplying A Marketing Service For A Business of Your ChoiceDocument16 pagesDerive A Customer Relationship Strategy For A Marketer Supplying A Marketing Service For A Business of Your ChoiceTinotenda Reginald ChabvongaNo ratings yet

- (2018) Data Analysis of Consumer Complaints in BankingDocument5 pages(2018) Data Analysis of Consumer Complaints in BankingWONG ZHI LIN MBS201232No ratings yet

- E-Banking and Customer Satisfaction ThesisDocument5 pagesE-Banking and Customer Satisfaction Thesisnessahallhartford100% (2)

- Industrial Marketing Management: Jui-Long Hung, Wu He, Jiancheng Shen TDocument10 pagesIndustrial Marketing Management: Jui-Long Hung, Wu He, Jiancheng Shen TЈелена МанојловићNo ratings yet

- An Empirical Comparison of Machine-Learning Methods On Bank Client Credit AssessmentsDocument23 pagesAn Empirical Comparison of Machine-Learning Methods On Bank Client Credit Assessmentscagp5001No ratings yet

- Expert Systems With Applications: Guangli Nie, Wei Rowe, Lingling Zhang, Yingjie Tian, Yong ShiDocument3 pagesExpert Systems With Applications: Guangli Nie, Wei Rowe, Lingling Zhang, Yingjie Tian, Yong ShiPiNo ratings yet

- Banking Literature ReviewDocument5 pagesBanking Literature Reviewafmzeracmdvbfe100% (1)

- Benchmarking State-Of-The-Art Classification Algorithms For Credit Scoring: A Ten-Year UpdateDocument30 pagesBenchmarking State-Of-The-Art Classification Algorithms For Credit Scoring: A Ten-Year UpdatemahaNo ratings yet

- Level of Awareness Regarding BancassuranceDocument15 pagesLevel of Awareness Regarding BancassuranceNhud GhazaliNo ratings yet

- Literature Review of CRM in Banking SectorDocument6 pagesLiterature Review of CRM in Banking Sectoraflschrjx100% (1)

- Chapter 2Document6 pagesChapter 2sinchanaNo ratings yet

- Consumer Awareness and Satisfaction Related To E Commerce Sector.Document8 pagesConsumer Awareness and Satisfaction Related To E Commerce Sector.Sarit SinghNo ratings yet

- Bank Loan Case Study ReportDocument23 pagesBank Loan Case Study Reportabrarmungi120402No ratings yet

- Research ProposalDocument8 pagesResearch Proposaldawood sadiq janjuaNo ratings yet

- Customer Churn Prediction in Banking Industry Using Power-BiDocument9 pagesCustomer Churn Prediction in Banking Industry Using Power-BiDiana VargheseNo ratings yet

- Research Proposal - FINANCE: Customer Churn & Cultural Shift in Banking IndustryDocument6 pagesResearch Proposal - FINANCE: Customer Churn & Cultural Shift in Banking IndustryNavmeen KhanNo ratings yet

- Mijet,+EngAcc+Vol08no01pp15 21+Vr03Document7 pagesMijet,+EngAcc+Vol08no01pp15 21+Vr03Esteti Handayani HiaNo ratings yet

- 1 Ijsmmrdfeb20181Document10 pages1 Ijsmmrdfeb20181TJPRC PublicationsNo ratings yet

- Capstone Project Weekly Progress ReportDocument3 pagesCapstone Project Weekly Progress ReportRohit NNo ratings yet

- Data Mining Attrition AnalysisDocument14 pagesData Mining Attrition AnalysisNam TungNo ratings yet

- Peer To Peer Lending Risk Analysis: Predictions From Lending ClubDocument10 pagesPeer To Peer Lending Risk Analysis: Predictions From Lending Clubortegadelia810No ratings yet

- Computers in Human Behavior: Tiago Oliveira, Matilde Alhinho, Paulo Rita, Gurpreet DhillonDocument12 pagesComputers in Human Behavior: Tiago Oliveira, Matilde Alhinho, Paulo Rita, Gurpreet DhillonMad HydroNo ratings yet

- Literature Review of Banking SystemDocument6 pagesLiterature Review of Banking Systemafmzsgbmgwtfoh100% (1)

- ADVANCED WEB DESIGN AND CONTENT MANAGEMENT ReportDocument42 pagesADVANCED WEB DESIGN AND CONTENT MANAGEMENT ReportMOHAMAD IZUDIN ABDUL RAHAMANNo ratings yet

- Credit Approval Data Analysis Using Classification and Regression ModelsDocument2 pagesCredit Approval Data Analysis Using Classification and Regression Modelsaman guptaNo ratings yet

- Credit Risk Management Literature Review PDFDocument7 pagesCredit Risk Management Literature Review PDFafmzveaqnkpypm100% (1)

- Finance & Banking Studies: Accounts Receivables Management: Insight and ChallengesDocument12 pagesFinance & Banking Studies: Accounts Receivables Management: Insight and ChallengesJuheltiNo ratings yet

- What Is The Right Delivery Option For YouDocument23 pagesWhat Is The Right Delivery Option For YouTien Thanh DangNo ratings yet

- A Comparative Study of Data Mining Techniques in Predicting Consumers' Credit Card Risk in BanksDocument6 pagesA Comparative Study of Data Mining Techniques in Predicting Consumers' Credit Card Risk in BankserwismeNo ratings yet

- Literature Review On Banking RegulationDocument8 pagesLiterature Review On Banking Regulationafdtwbhyk100% (1)

- Loan Eligibility PredictionDocument12 pagesLoan Eligibility PredictionUddhav ChaliseNo ratings yet

- Literature Review On Banking in IndiaDocument4 pagesLiterature Review On Banking in Indiaea6qsxqd100% (1)

- Patel Vipul (097520592058) Patel Nisit (097520592054)Document23 pagesPatel Vipul (097520592058) Patel Nisit (097520592054)Vipul PatelNo ratings yet

- Bayesian Data Mining, With Application To Bench Marking and Credit ScoringDocument13 pagesBayesian Data Mining, With Application To Bench Marking and Credit ScoringNedim HifziefendicNo ratings yet

- ProjectDocument15 pagesProjectJitender ThakurNo ratings yet

- Literature Review On Retail LoansDocument8 pagesLiterature Review On Retail Loansafmzaoahmicfxg100% (1)

- Credit Risk and Financial Integration: An Application of Network AnalysisDocument3 pagesCredit Risk and Financial Integration: An Application of Network AnalysiskamransNo ratings yet

- Analyzing Machine Learning Models For Credit Scoring With Explainable AI and Optimizing Investment DecisionsDocument16 pagesAnalyzing Machine Learning Models For Credit Scoring With Explainable AI and Optimizing Investment DecisionsaijbmNo ratings yet

- Cluster Credit Risk R PDFDocument13 pagesCluster Credit Risk R PDFFabian ChahinNo ratings yet

- Churn ModelingDocument11 pagesChurn ModelingAvinash Shankar100% (1)

- RegressionDocument22 pagesRegressionRasheed OlatunbosunNo ratings yet

- CHapter 3 (Literature Review)Document13 pagesCHapter 3 (Literature Review)Kshitij ShingadeNo ratings yet

- SHIVAM - A00876542A - Capstone PaperDocument25 pagesSHIVAM - A00876542A - Capstone Papermaomao KateNo ratings yet

- MethodologyDocument8 pagesMethodologyMorelate KupfurwaNo ratings yet

- Empirical Literature Review On Mobile BankingDocument4 pagesEmpirical Literature Review On Mobile Bankinggw2xyzw9100% (1)

- Simulation of Trust in Client - Wealth Management Advisor RelationshipsDocument9 pagesSimulation of Trust in Client - Wealth Management Advisor RelationshipsLynnHanNo ratings yet

- Method For Ranking Online ReviewsDocument50 pagesMethod For Ranking Online Reviewskavya J.CNo ratings yet

- SSRN Id3769854Document8 pagesSSRN Id3769854whitneykarundeng08No ratings yet

- Emerging Trends in Banking Financial Services of Banking Sector in India With Respect To State Bank of IndiaDocument16 pagesEmerging Trends in Banking Financial Services of Banking Sector in India With Respect To State Bank of IndiaarcherselevatorsNo ratings yet

- Review Jurnal CB 2 (Sciencefirect Q1)Document16 pagesReview Jurnal CB 2 (Sciencefirect Q1)coffecake24No ratings yet

- Instance Sampling in Credit Scoring: An Empirical Study of Sample SizeDocument15 pagesInstance Sampling in Credit Scoring: An Empirical Study of Sample SizeerwismeNo ratings yet

- Data and Analytics in Action: Project Ideas and Basic Code Skeleton in PythonFrom EverandData and Analytics in Action: Project Ideas and Basic Code Skeleton in PythonNo ratings yet

- Crompton DealerDocument6 pagesCrompton Dealerrdeepak99No ratings yet

- Module 2Document108 pagesModule 2Lakshya JainNo ratings yet

- Baye Janson Unit 1 Part 1Document28 pagesBaye Janson Unit 1 Part 1Sudhanshu Sharma bchd21No ratings yet

- (Reaffirmed!2011) !Document10 pages(Reaffirmed!2011) !Devesh Kumar PandeyNo ratings yet

- Pakistan Stock Exchange (PSX)Document13 pagesPakistan Stock Exchange (PSX)NAQASH JAVED100% (2)

- Johnson V CanterburyWestland Standards Committee 3Document28 pagesJohnson V CanterburyWestland Standards Committee 3NUR INSYIRAH ZAININo ratings yet

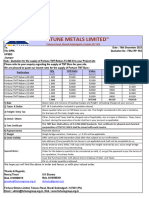

- "Fortune Metals Limited": Talwara Road, Mandi Gobindgarh, Punjab-147 301Document1 page"Fortune Metals Limited": Talwara Road, Mandi Gobindgarh, Punjab-147 301S K SharmaNo ratings yet

- KPDA Directory of Members in Good Standing, 18th May 2021Document3 pagesKPDA Directory of Members in Good Standing, 18th May 2021George K'OpiyoNo ratings yet

- Chapter 5 InvestmentDocument49 pagesChapter 5 InvestmentmeenNo ratings yet

- Flipkart Labels 27 Jun 2021 06 53Document1 pageFlipkart Labels 27 Jun 2021 06 53h4ckerNo ratings yet

- Department of Business Administration JUC-Male BranchDocument50 pagesDepartment of Business Administration JUC-Male BranchAmjad BUSAEEDNo ratings yet

- AJIO Null 1627137756324Document1 pageAJIO Null 1627137756324Rishi Kumar SinghNo ratings yet

- Payslip For The Month of May 2021: 16 Iris House Business Centre Nangal Raya New Delhi 110046Document1 pagePayslip For The Month of May 2021: 16 Iris House Business Centre Nangal Raya New Delhi 110046Manisha ThakurNo ratings yet

- Agencies That Facilitate International FlowsDocument2 pagesAgencies That Facilitate International FlowsLê Thị Ngọc DiễmNo ratings yet

- Nefas Silk Poly Technic College: Learning GuideDocument43 pagesNefas Silk Poly Technic College: Learning GuideNigussie BerhanuNo ratings yet

- Mira: An On-Chain Passive Investment Vehicle: 208311130BENZINGAFULLNGTH12290408 Makers#Document13 pagesMira: An On-Chain Passive Investment Vehicle: 208311130BENZINGAFULLNGTH12290408 Makers#ThanasisNo ratings yet

- Factories of The FutureDocument3 pagesFactories of The FutureKonstantina DumitruNo ratings yet

- Aging 6.17.2021Document81 pagesAging 6.17.2021Ricardo DelacruzNo ratings yet

- Hardiyanti 2Document9 pagesHardiyanti 2Devita Nuryco P . PNo ratings yet

- PFRS 16Document2 pagesPFRS 16Nerissa BulagsakNo ratings yet

- Return of Organization Exempt From Income Tax O&Lno.1545-0047Document102 pagesReturn of Organization Exempt From Income Tax O&Lno.1545-0047Peter M. HeimlichNo ratings yet

- The Law of Comparative AdvantageDocument8 pagesThe Law of Comparative AdvantageManak Ram SingariyaNo ratings yet

- Transaction Profile PDFDocument1 pageTransaction Profile PDFTanzir HasanNo ratings yet

- SARS INCOME TAX Notice of RegistrationDocument2 pagesSARS INCOME TAX Notice of RegistrationLame DudeNo ratings yet

- BestBari - Marketing Agreement - Property Sales (MARC Holdings LTD)Document4 pagesBestBari - Marketing Agreement - Property Sales (MARC Holdings LTD)Abdullah HridoyNo ratings yet

- Entreprepreneurship, Seminar TopicDocument13 pagesEntreprepreneurship, Seminar Topicadityakalani000oooNo ratings yet

- BYDDDocument25 pagesBYDDandre.torresNo ratings yet