You might also like

- Accounting 101Document4 pagesAccounting 101Cheche AmpoanNo ratings yet

- Accounting Midterms ReviwerDocument5 pagesAccounting Midterms ReviwermariaNo ratings yet

- Accounting 1Document3 pagesAccounting 1Carmina Dongcayan100% (1)

- Primitive Accounting Middle Ages Industrial Revolution & Corporate Organization Information AgeDocument28 pagesPrimitive Accounting Middle Ages Industrial Revolution & Corporate Organization Information AgePhil Cahilig-GariginovichNo ratings yet

- Integrated AccountingDocument4 pagesIntegrated AccountingJennilou AñascoNo ratings yet

- Chapter-One 1. Introduction To Accounting and Business: Objectives After Studying This Chapter, You Should Be Able ToDocument16 pagesChapter-One 1. Introduction To Accounting and Business: Objectives After Studying This Chapter, You Should Be Able ToAbrha636100% (1)

- LS 1 - ACCOUNTING AND ITS ENVIRONMENT Part 2Document53 pagesLS 1 - ACCOUNTING AND ITS ENVIRONMENT Part 2Danielle Angel Malana100% (1)

- Chapter 1 Int. To Acc. and BusinessDocument13 pagesChapter 1 Int. To Acc. and BusinessSellihom TadesseNo ratings yet

- Financial Accounting Discussion 1Document11 pagesFinancial Accounting Discussion 1Tasha HilarieNo ratings yet

- Accounting Is The Art of RecordingDocument10 pagesAccounting Is The Art of RecordingChristine ChuaNo ratings yet

- Abm1 PPTDocument161 pagesAbm1 PPTPavi Antoni Villaceran100% (1)

- ACCOUNTING-WPS OfficeDocument6 pagesACCOUNTING-WPS OfficeNorjehanie AliNo ratings yet

- BAM 1 - Fundamentals of AccountingDocument33 pagesBAM 1 - Fundamentals of AccountingimheziiyyNo ratings yet

- Accounting and Its EnvironmentDocument27 pagesAccounting and Its EnvironmentMarta MeaNo ratings yet

- Far 1 Accounting For Partnership Corporation Midterms Review CompressDocument12 pagesFar 1 Accounting For Partnership Corporation Midterms Review CompressBuhia, Alexandra DeniceNo ratings yet

- Principle ch-1 EditedDocument14 pagesPrinciple ch-1 Editedfitsum tesfayeNo ratings yet

- External Users: Not Directly Involved. These Are Secondary Users of Financial Information Who Are PartiesDocument8 pagesExternal Users: Not Directly Involved. These Are Secondary Users of Financial Information Who Are PartiesAizel AlindoyNo ratings yet

- Chapter 1-Introduction To Financial Accounting (Acc106)Document17 pagesChapter 1-Introduction To Financial Accounting (Acc106)Syahirah AzlyzanNo ratings yet

- Principles of Accounting (Notes)Document6 pagesPrinciples of Accounting (Notes)hjpa2023-7388-23616No ratings yet

- CHAPTER 1 and 2 Overview and Concepts in AccountingDocument15 pagesCHAPTER 1 and 2 Overview and Concepts in AccountingVin FajardoNo ratings yet

- Acct-1 Chap-1-1Document11 pagesAcct-1 Chap-1-1Natnael GetahunNo ratings yet

- Accounting ReviewerDocument6 pagesAccounting ReviewerFictional PlayerNo ratings yet

- Accounting Concepts An PrinciplesDocument3 pagesAccounting Concepts An PrinciplesDanica QuinacmanNo ratings yet

- Far NotesDocument4 pagesFar NotesMikasa AckermanNo ratings yet

- Accounting 101Document6 pagesAccounting 101Gianna ReyesNo ratings yet

- ACT103 - Module 1Document13 pagesACT103 - Module 1Le MinouNo ratings yet

- Lesson 1Document33 pagesLesson 1Cher NaNo ratings yet

- Chapter 1 8Document19 pagesChapter 1 8Ren AikawaNo ratings yet

- Accounting PrinciplesDocument22 pagesAccounting PrinciplesMicah Danielle S. TORMONNo ratings yet

- Fabm MidtermDocument7 pagesFabm MidtermSamantha LiberatoNo ratings yet

- Chapter 1 PPT - UpdatedDocument64 pagesChapter 1 PPT - Updatedjoudaa alkordyNo ratings yet

- Chapter 1 Notes: Created Tags UpdatedDocument6 pagesChapter 1 Notes: Created Tags UpdatedTristan RamosNo ratings yet

- Mfe Finals ReviewerDocument3 pagesMfe Finals ReviewerMerry Joy SolizaNo ratings yet

- Basic Accounting Crash CourseDocument5 pagesBasic Accounting Crash CourseCyra JimenezNo ratings yet

- ACT103 - Topic 1Document3 pagesACT103 - Topic 1Juan FrivaldoNo ratings yet

- BAC 813 - Financial Accounting Premium Notes - Elab Notes LibraryDocument111 pagesBAC 813 - Financial Accounting Premium Notes - Elab Notes LibraryWachirajaneNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Basic ConceptsDocument5 pagesBasic ConceptsAgatha ApolinarioNo ratings yet

- Fabmlt 1Document3 pagesFabmlt 1lemonNo ratings yet

- Basic Accounting-Made EasyDocument20 pagesBasic Accounting-Made EasyRoy Kenneth Lingat100% (1)

- Modules 1Document4 pagesModules 1JT GalNo ratings yet

- I Introduction To AccountingDocument9 pagesI Introduction To AccountingDirck VerraNo ratings yet

- Acctg BasicsDocument5 pagesAcctg BasicsLmark VerdadNo ratings yet

- Development and Basic Concepts of Accounting 1Document10 pagesDevelopment and Basic Concepts of Accounting 1saphirejunelNo ratings yet

- Basic AccountingDocument7 pagesBasic AccountingBaby PinkNo ratings yet

- Acca101 SGDocument4 pagesAcca101 SGBeatrice Dominique C. PepinoNo ratings yet

- Summary 2Document4 pagesSummary 2Anne Thea AtienzaNo ratings yet

- Chapter 1 Class NotesDocument8 pagesChapter 1 Class Notesraviloves07No ratings yet

- Principles of Accounting (Notes)Document5 pagesPrinciples of Accounting (Notes)hjpa2023-7388-23616No ratings yet

- Buss1030 Notes: 1.1 Factors Affecting The Complexity of A Changing Business EnvironmentDocument56 pagesBuss1030 Notes: 1.1 Factors Affecting The Complexity of A Changing Business EnvironmentTINo ratings yet

- Accounting For EMBA Prepared by Ahmed SabbirDocument95 pagesAccounting For EMBA Prepared by Ahmed Sabbirsabbir ahmed100% (1)

- CAT 1 Module (NIAT Encoded)Document245 pagesCAT 1 Module (NIAT Encoded)UFO CatcherNo ratings yet

- Unit 1 - Introduction To Principles of AccountingDocument100 pagesUnit 1 - Introduction To Principles of AccountingNgonga FumbeloNo ratings yet

- Fin Acc TextbookDocument520 pagesFin Acc TextbookjrjhvbydfnNo ratings yet

- Accounting - DoneDocument6 pagesAccounting - Doneayaa caranzaNo ratings yet

- Revised Conceptual Framework 1st LessonDocument18 pagesRevised Conceptual Framework 1st LessonheeeyjanengNo ratings yet

- Far AssignmentDocument5 pagesFar AssignmentMy everyday LifeeeNo ratings yet

- Conceptual Foundation of Company AccountingDocument6 pagesConceptual Foundation of Company AccountingBibhush MaharjanNo ratings yet

- Business EtiquetteDocument1 pageBusiness EtiquetteTričiaStypayhørliksønNo ratings yet

- Behind Closed Doors - CritiqueDocument2 pagesBehind Closed Doors - CritiqueTričiaStypayhørliksønNo ratings yet

- GR NO 208113 - Dolores Diaz Vs PeopleDocument3 pagesGR NO 208113 - Dolores Diaz Vs PeopleTričiaStypayhørliksønNo ratings yet

- G.R. No. 153511 - Case DigestDocument3 pagesG.R. No. 153511 - Case DigestTričiaStypayhørliksønNo ratings yet

- GR NO 208113 - Dolores Diaz Vs PeopleDocument3 pagesGR NO 208113 - Dolores Diaz Vs PeopleTričiaStypayhørliksønNo ratings yet

- Ebook Ebook PDF Short Term Financial Management Fifth Edition PDFDocument41 pagesEbook Ebook PDF Short Term Financial Management Fifth Edition PDFlaura.gray126100% (40)

- Demo Rapidminer New Data April 5Document6 pagesDemo Rapidminer New Data April 5Mohit SainiNo ratings yet

- Sa20190515 PDFDocument4 pagesSa20190515 PDFMitess Boñon BrusolaNo ratings yet

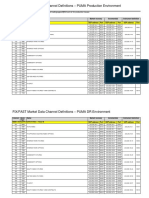

- FIX/FAST Market Data Channel Definitions - PUMA Production EnvironmentDocument3 pagesFIX/FAST Market Data Channel Definitions - PUMA Production EnvironmentVaibhav PoddarNo ratings yet

- HSBCDocument9 pagesHSBCMohammad Mehdi JourabchiNo ratings yet

- 5 Strategic Capacity Planning For Products and ServicesDocument39 pages5 Strategic Capacity Planning For Products and ServicesRubaet HossainNo ratings yet

- Conde Build Enterprises: Official ReceiptDocument1 pageConde Build Enterprises: Official ReceiptCondebuild StaffNo ratings yet

- Pag-Ibig PAMP - NegoSale - Batch - 3 - 102819Document15 pagesPag-Ibig PAMP - NegoSale - Batch - 3 - 102819Patricia Marie ManaliliNo ratings yet

- Original Listing ApplicationDocument4 pagesOriginal Listing ApplicationMihaela GaneaNo ratings yet

- Brokerage Business PlanDocument19 pagesBrokerage Business PlanMuhammad Ahmed50% (4)

- Times-Trib 43 MGDocument28 pagesTimes-Trib 43 MGnewspubincNo ratings yet

- Certificate of Creditable Tax Withheld at Source: Kawanihan NG Rentas InternasDocument4 pagesCertificate of Creditable Tax Withheld at Source: Kawanihan NG Rentas Internaszairah jean baquilarNo ratings yet

- Ross12e - CHAPTER 4 - NMIMS - Practice Problems and Solutions For ClassDocument8 pagesRoss12e - CHAPTER 4 - NMIMS - Practice Problems and Solutions For Classwander boyNo ratings yet

- HK Weekly Summary 20230718Document2 pagesHK Weekly Summary 20230718Nabil JazliNo ratings yet

- Sps. Carpo v. ChuamDocument13 pagesSps. Carpo v. ChuamEmma Ruby Aguilar-ApradoNo ratings yet

- Camposol Holding 3q 2020 Presentation PDFDocument23 pagesCamposol Holding 3q 2020 Presentation PDFJorge Zegarra ValverdeNo ratings yet

- Concertina Barb Wire (1) .Xlsxengineering EstimateDocument4 pagesConcertina Barb Wire (1) .Xlsxengineering Estimatepja shanthaNo ratings yet

- 02-06-09 Lynn Federal Court OrderDocument6 pages02-06-09 Lynn Federal Court OrdermderigoNo ratings yet

- FS of Infinity Adventure Farm and ResortDocument35 pagesFS of Infinity Adventure Farm and ResortbeldiansitsolutionsNo ratings yet

- Far660 Jan 2018 SolutionDocument7 pagesFar660 Jan 2018 SolutionHanis ZahiraNo ratings yet

- USBNDocument9 pagesUSBNAhmad Azka PrasetyoNo ratings yet

- Asset Liability ManagementDocument8 pagesAsset Liability ManagementAvinash Veerendra TakNo ratings yet

- Loan Wo Title Islamic Madam Ainul Lecture Notes PDFDocument3 pagesLoan Wo Title Islamic Madam Ainul Lecture Notes PDFFreya MehmeenNo ratings yet

- 41b EnglishDocument28 pages41b Englishபூவை ஜெ ரூபன்சார்லஸ்No ratings yet

- Project Cost ManagementDocument34 pagesProject Cost ManagementJanele PoxNo ratings yet

- Account Management & Client Services: Ashita Gupta 13PGDM136Document71 pagesAccount Management & Client Services: Ashita Gupta 13PGDM136Karan GuptaNo ratings yet

- HRM - AskaribankDocument21 pagesHRM - Askaribankhamidmalik-10% (1)

- Test EksDocument7 pagesTest EksAleksandra AbramovaNo ratings yet

- IDN Times - Taskforce - Media & HomelessDocument1 pageIDN Times - Taskforce - Media & HomelessHanan Rananta ArbiNo ratings yet

- Corporate Disclosure Practices in Indian Software IndustryDocument35 pagesCorporate Disclosure Practices in Indian Software IndustrysiyatuliNo ratings yet