You might also like

- Des Ember 01Document2 pagesDes Ember 01Affan akbar Reno antonoNo ratings yet

- Brazil's Template Adjusted Growth StrategiesDocument36 pagesBrazil's Template Adjusted Growth StrategiesbrunoorsiscribdNo ratings yet

- PROD-1213 Tot ProvincialDocument1 pagePROD-1213 Tot ProvincialRamiro SosaNo ratings yet

- Volume RateDocument1 pageVolume Ratekimboon_ngNo ratings yet

- Advances in Control Systems: Theory and ApplicationsFrom EverandAdvances in Control Systems: Theory and ApplicationsNo ratings yet

- Mét R I Cas: Mar Gem Li Qui DaDocument1 pageMét R I Cas: Mar Gem Li Qui DafosaumNo ratings yet

- Demonstra??es Financeiras em Padr?es InternacionaisDocument73 pagesDemonstra??es Financeiras em Padr?es InternacionaisKlabin_RINo ratings yet

- Computer Integrated ConstructionFrom EverandComputer Integrated ConstructionH. WagterNo ratings yet

- Kmeans Clustering-Results PDFDocument35 pagesKmeans Clustering-Results PDFAnneNo ratings yet

- Annex E Balance Sheet 2020Document4 pagesAnnex E Balance Sheet 2020EunicaNo ratings yet

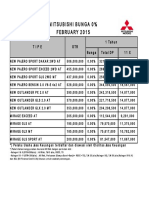

- Mitsubishibunga 0% February 2015: Tip E Otr 1 Tahun Bunga Totaldp 1 1 XDocument1 pageMitsubishibunga 0% February 2015: Tip E Otr 1 Tahun Bunga Totaldp 1 1 Xstella sunstarbaliNo ratings yet

- Can The MICs Reach The Social MDGS? How Inclusive and Sustainable Are Asia's Social Protection Systems in Asia? (Presentation)Document23 pagesCan The MICs Reach The Social MDGS? How Inclusive and Sustainable Are Asia's Social Protection Systems in Asia? (Presentation)ADB Poverty ReductionNo ratings yet

- Bosch Rexroth - Catalog de Produse de BazăDocument38 pagesBosch Rexroth - Catalog de Produse de Bazăjo_rz_57No ratings yet

- CFA L1 ClassNotes SampleDocument35 pagesCFA L1 ClassNotes Samplepranavkumar17373No ratings yet

- Annex E Cash Flow 2020Document2 pagesAnnex E Cash Flow 2020EunicaNo ratings yet

- Significant Causes: SUR Lafarge Surma Cement LTDDocument1 pageSignificant Causes: SUR Lafarge Surma Cement LTDprosenjit2001No ratings yet

- Important 1 TDDocument5 pagesImportant 1 TDSalah Eddine SpiritNo ratings yet

- Pm-030 Ims Transition and Contingency Plan v2Document20 pagesPm-030 Ims Transition and Contingency Plan v2Ivo HuaynatesNo ratings yet

- Technical table conversionDocument1 pageTechnical table conversionkimboon_ngNo ratings yet

- Program 1 ResultsDocument3 pagesProgram 1 ResultsChirag SaraogiNo ratings yet

- ZjbnubjDocument1 pageZjbnubjKeilaLimaNo ratings yet

- Interface: Register RegisterDocument26 pagesInterface: Register RegisterPolitik Itu KejamNo ratings yet

- Maruti SuzukiDocument20 pagesMaruti SuzukiMalay SaurabhNo ratings yet

- CAPITAL STRUCTURE ANALYSIS OF NESTLE INDIA LIMITEDDocument19 pagesCAPITAL STRUCTURE ANALYSIS OF NESTLE INDIA LIMITEDtony_njNo ratings yet

- Islamabad Campus: Chartered and Recognized by The GovernmentDocument2 pagesIslamabad Campus: Chartered and Recognized by The Governmentsaim1005No ratings yet

- Bata Sept 10 ResltsDocument1 pageBata Sept 10 Resltssubodh_purohit7258No ratings yet

- EN Review of Hydraulic Equipment MaintanceDocument16 pagesEN Review of Hydraulic Equipment MaintanceMukhsi Hanafi2No ratings yet

- Confirmed and Probable COVID-19 Deaths Daily ReportDocument3 pagesConfirmed and Probable COVID-19 Deaths Daily ReportMohamad ShafeyNo ratings yet

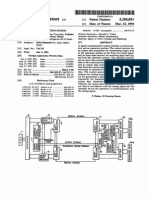

- United States Patent (19) : MarchDocument7 pagesUnited States Patent (19) : Marchghftr456No ratings yet

- STS130Document252 pagesSTS130MaestroColicus0% (1)

- Orçamento Do Veículo: Obs: Coifa CaixaDocument1 pageOrçamento Do Veículo: Obs: Coifa CaixaAntonio GoncalvesNo ratings yet

- MOSIS Acceptance Test Results for 0.18um TechnologyDocument2 pagesMOSIS Acceptance Test Results for 0.18um TechnologyPraveen VsNo ratings yet

- HK Mk.23 SOCOM Pistol User ManualDocument48 pagesHK Mk.23 SOCOM Pistol User ManualGasMaskBobNo ratings yet

- Retail Financial ModelingDocument43 pagesRetail Financial ModelingtsohNo ratings yet

- Shell Flavex Oil 595: Specifications, Approvals & RecommendationsDocument2 pagesShell Flavex Oil 595: Specifications, Approvals & RecommendationsΠΑΝΑΓΙΩΤΗΣΠΑΝΑΓΟΣNo ratings yet

- CH 04 - Slides UpdatedDocument50 pagesCH 04 - Slides Updatedakshitnagpal9119No ratings yet

- NRT1 BookletDocument13 pagesNRT1 Bookletjaya19844No ratings yet

- United States Patent (19) : Bass Et A1Document70 pagesUnited States Patent (19) : Bass Et A1scolem26No ratings yet

- Consumption comparison of Cheers gallon vs 600mlDocument1 pageConsumption comparison of Cheers gallon vs 600mlDanang NCONo ratings yet

- ABC Drawing of Stoppage Apparent Causes/causes: SUR Lafarge Surma Cement LTDDocument1 pageABC Drawing of Stoppage Apparent Causes/causes: SUR Lafarge Surma Cement LTDprosenjit2001No ratings yet

- ARRI Alexa Pocket Guide 2.2Document4 pagesARRI Alexa Pocket Guide 2.2Cristal Vidrio100% (1)

- Find IP address detailsDocument1 pageFind IP address detailsRizki BunaNo ratings yet

- Canon 5diii Pocket Guide 1.2Document4 pagesCanon 5diii Pocket Guide 1.2William R AmyotNo ratings yet

- ArchivesDocument16 pagesArchivesAnonymous Feglbx5No ratings yet

- Data Booklet - IAL ChemistryDocument35 pagesData Booklet - IAL ChemistryZainabNo ratings yet

- Overview and Recent Developments: India Seen in Last 10 Odd Years As The Emerging Professional Services Hub of The WorldDocument32 pagesOverview and Recent Developments: India Seen in Last 10 Odd Years As The Emerging Professional Services Hub of The Worldratan bauriNo ratings yet

- 1/16 Scale Models - Special Sets: PZ - Kpfw. VI, Tiger I, Ausf.E (SD - Kfz. 181) - Early VersionDocument5 pages1/16 Scale Models - Special Sets: PZ - Kpfw. VI, Tiger I, Ausf.E (SD - Kfz. 181) - Early VersionsharkmouthNo ratings yet

- Umted States Patent (191 (111 4,229,287: Lepetic (45) Oct. 21, 1980Document9 pagesUmted States Patent (191 (111 4,229,287: Lepetic (45) Oct. 21, 1980Alfredo CollantesNo ratings yet

- CH - Ops - Manual Part 2Document58 pagesCH - Ops - Manual Part 2Ivan BeljinNo ratings yet

- Prog KustaDocument61 pagesProg KustaOcha BadjoNo ratings yet

- Movimientos Mensuales de ResultadosDocument3 pagesMovimientos Mensuales de ResultadosLuis Enrique TIMOTEO ORUENo ratings yet

- Movimientos Mensuales de ResultadosDocument3 pagesMovimientos Mensuales de ResultadosLuis Enrique TIMOTEO ORUENo ratings yet

- Electrical PhilosophyDocument27 pagesElectrical Philosophystoica4laurentiuNo ratings yet

- Maxon Smartfire Control System SpecDocument12 pagesMaxon Smartfire Control System SpecJohn HowardNo ratings yet

- Glastic Standoffs InsulatorsDocument2 pagesGlastic Standoffs Insulatorsdanielliram993No ratings yet

- Husky Injection Molding Systems Strategic AnalysisDocument8 pagesHusky Injection Molding Systems Strategic AnalysisYUVRAJ SINGHNo ratings yet

- Analysis of Labour Codes - Revised 29.10.2020 17.50Document64 pagesAnalysis of Labour Codes - Revised 29.10.2020 17.50subirdutNo ratings yet

- Gartley ADocument4 pagesGartley Amohammad alkhawarahNo ratings yet

- Nezone FinalDocument61 pagesNezone Finalvictor saikiaNo ratings yet

- Input 4 - Internal Quality Control SystemDocument12 pagesInput 4 - Internal Quality Control SystemRalph Aldrin F. VallesterosNo ratings yet

- Process Costing DIP PDFDocument62 pagesProcess Costing DIP PDFIrushi EdirisinghaNo ratings yet

- 7094 Bangladesh Studies: MARK SCHEME For The May/June 2011 Question Paper For The Guidance of TeachersDocument11 pages7094 Bangladesh Studies: MARK SCHEME For The May/June 2011 Question Paper For The Guidance of Teachersmstudy123456No ratings yet

- Group 1 - Section A-MyntraDocument11 pagesGroup 1 - Section A-MyntraMaithili JoshiNo ratings yet

- Artigo Ades Di Tella 1995Document20 pagesArtigo Ades Di Tella 1995carlosNo ratings yet

- Discuss Whether Rising Real GDP Per Person Was Sufficient To Ensure That Every Citizen of The UK Was Better Off in 2013 Than 1971Document2 pagesDiscuss Whether Rising Real GDP Per Person Was Sufficient To Ensure That Every Citizen of The UK Was Better Off in 2013 Than 1971Shreya KochharNo ratings yet

- Intermediate Macroeconomics ModuleDocument76 pagesIntermediate Macroeconomics ModuleKatunga MwiyaNo ratings yet

- Articles ArchiveDocument170 pagesArticles ArchiveMayarani PraharajNo ratings yet

- Ayana Renewable Power Sr. Manager SCM EPC JobDocument3 pagesAyana Renewable Power Sr. Manager SCM EPC JobBala JiNo ratings yet

- MBA608 - Corporate Finance CHD UnivDocument297 pagesMBA608 - Corporate Finance CHD Univaashish rana100% (2)

- Nifty 50 ratiosDocument6 pagesNifty 50 ratiosDeepak RahejaNo ratings yet

- Cover Sheet SEC Form Interim FinancialsDocument79 pagesCover Sheet SEC Form Interim FinancialsKeziah Eden Tuazon-SapantaNo ratings yet

- NR ResumeDocument4 pagesNR ResumeNAMBIRAJAN GNo ratings yet

- Change Mangement and Recruitment System of Metlife (NASRIN SULTANA) 111 153 118 Final SubmissionDocument52 pagesChange Mangement and Recruitment System of Metlife (NASRIN SULTANA) 111 153 118 Final SubmissionSelim KhanNo ratings yet

- Tally 8.1: Tally 8.1 Tally 8.1 VAT Tally 7.2 Indian SoftwareDocument439 pagesTally 8.1: Tally 8.1 Tally 8.1 VAT Tally 7.2 Indian SoftwareMayank DadhichNo ratings yet

- Processing Terminal Benefits of RetireeDocument85 pagesProcessing Terminal Benefits of RetireeMichael MalabejaNo ratings yet

- Marxist Theories of Imperialism001Document33 pagesMarxist Theories of Imperialism001ChristopherGundersonNo ratings yet

- UNEP - 2013 - Integrating Env in Urban Plan & MNGMTDocument77 pagesUNEP - 2013 - Integrating Env in Urban Plan & MNGMTAlvin YPxixNo ratings yet

- International Joint Ventures Article - Stewart PDFDocument6 pagesInternational Joint Ventures Article - Stewart PDFBernard ChungNo ratings yet

- Project Report On Starting A New Business.... (Comfort Jeans)Document30 pagesProject Report On Starting A New Business.... (Comfort Jeans)lalitsingh76% (72)

- Book Keeping & Accountancy March 2019 STD 12th Commerce HSC Maharashtra Board Question PaperDocument5 pagesBook Keeping & Accountancy March 2019 STD 12th Commerce HSC Maharashtra Board Question PaperBhavin MamtoraNo ratings yet

- PUP Lesson on Scanning Industry Opportunities and ThreatsDocument8 pagesPUP Lesson on Scanning Industry Opportunities and ThreatsMika MolinaNo ratings yet

- Chapter 2 (EdDocument7 pagesChapter 2 (Ednafisul hoque moinNo ratings yet

- To What Extent Do The Incoterms 2000 Determine The Passing of Risk in A Sale Contract On Shipment Terms?Document19 pagesTo What Extent Do The Incoterms 2000 Determine The Passing of Risk in A Sale Contract On Shipment Terms?shahriar2004No ratings yet

- Financial Analysis and Risk Assessment of Production ProjectDocument10 pagesFinancial Analysis and Risk Assessment of Production ProjectSaroj MaharjanNo ratings yet

- Corporate Finance Assignment One (20%)Document5 pagesCorporate Finance Assignment One (20%)Linh BuiNo ratings yet