You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Kimball DimensionalModelingDocument75 pagesKimball DimensionalModelingMusaddiq KhanNo ratings yet

- SBasic ABAPDocument167 pagesSBasic ABAPTejaswi paritalaNo ratings yet

- Oracle DWDocument522 pagesOracle DWSellSalesNo ratings yet

- Website Design AgreementDocument21 pagesWebsite Design AgreementPierrot Mamba100% (1)

- CAE Parc Aviation Ethiopian Airlines - B777 Captain - Terms and Conditio...Document5 pagesCAE Parc Aviation Ethiopian Airlines - B777 Captain - Terms and Conditio...Marcos BantelNo ratings yet

- BS 5977 - 1 Lintels PDFDocument14 pagesBS 5977 - 1 Lintels PDFTom YeeNo ratings yet

- Encyclopædia of Law and - Forms PDFDocument731 pagesEncyclopædia of Law and - Forms PDFJulio Cesar Navas100% (1)

- Corporate Social Responsibility of AmouageDocument10 pagesCorporate Social Responsibility of AmouageZahur AhmedNo ratings yet

- Technology & SocietyDocument29 pagesTechnology & SocietyJulius Memeg PanayoNo ratings yet

- Artistic and Cultural EventDocument17 pagesArtistic and Cultural EventDaniela Lara SaénzNo ratings yet

- Shagor CV (New)Document2 pagesShagor CV (New)md_shagorNo ratings yet

- ERS - Evaluated Receipt SystemDocument3 pagesERS - Evaluated Receipt Systemjindalyash1234No ratings yet

- Project Report On Vivels Fairness CreamDocument47 pagesProject Report On Vivels Fairness CreamDhirender Chauhan0% (1)

- Taxguru - In-Sample Management Representation Letter For GST AuditDocument6 pagesTaxguru - In-Sample Management Representation Letter For GST AuditranjitNo ratings yet

- Implementing A Successful OM Strategy For Solar PVDocument10 pagesImplementing A Successful OM Strategy For Solar PVfoxmancementNo ratings yet

- Amazon Buy Box Bible - 2016Document53 pagesAmazon Buy Box Bible - 2016mhermes100% (1)

- 5b3b0c0283739 BPI IR 2017 Senior Management and Corporate Governance 6Document20 pages5b3b0c0283739 BPI IR 2017 Senior Management and Corporate Governance 6John Karlo CamineroNo ratings yet

- LC Financial Report & Google Drive Link: Aiesec Delhi IitDocument6 pagesLC Financial Report & Google Drive Link: Aiesec Delhi IitCIM_DelhiIITNo ratings yet

- Chapter 10 (2ed) 2Document12 pagesChapter 10 (2ed) 2api-522706No ratings yet

- Sun Account DetailsDocument12 pagesSun Account DetailsJulius AlcantaraNo ratings yet

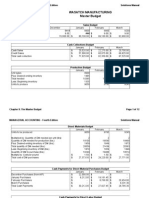

- Wasatch ManufacturingDocument12 pagesWasatch Manufacturingapi-301899907No ratings yet

- Wilo Dealer Evaluation FormDocument4 pagesWilo Dealer Evaluation FormBala Ji GNo ratings yet

- Khodaram OLDocument9 pagesKhodaram OLKrupal MehtaNo ratings yet

- Issues of The Local Investment Code of The City of Malolos, BulacanDocument4 pagesIssues of The Local Investment Code of The City of Malolos, BulacanJan Russell Nicolas CruzNo ratings yet

- KEY Cuadernillo Nivel 4Document112 pagesKEY Cuadernillo Nivel 4Cami NogueraNo ratings yet

- Gujarat Activity ReportDocument15 pagesGujarat Activity ReportgandhiannexNo ratings yet

- TQM: A Quality and Performance Enhancer: Laxmikumari DR Y Vijay Kumar Dr. V.Venkata RamanaDocument4 pagesTQM: A Quality and Performance Enhancer: Laxmikumari DR Y Vijay Kumar Dr. V.Venkata RamanaAce Maynard DiancoNo ratings yet

- Brewers On The RiseDocument46 pagesBrewers On The RiselstntNo ratings yet

- 12.06.2013 CaDocument31 pages12.06.2013 CasugupremNo ratings yet

- Electronic Data InterchangeDocument16 pagesElectronic Data InterchangeGauravNo ratings yet