You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Concrete Repair Guide For Concrete Bridge ComponentsDocument20 pagesConcrete Repair Guide For Concrete Bridge ComponentsSifis MakridakisNo ratings yet

- Mandrake Amigurumi - Free Crochet Pattern - StringyDingDingDocument23 pagesMandrake Amigurumi - Free Crochet Pattern - StringyDingDingrosescal100% (2)

- 12 Tissue Remedies of Shcussler by Boerick.Document432 pages12 Tissue Remedies of Shcussler by Boerick.scientist786100% (8)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Year 8 SoundDocument33 pagesYear 8 SoundBaggao Nas Sta Margarita67% (3)

- Gi-0007 021Document4 pagesGi-0007 021malika_00No ratings yet

- Matter and Interaction Chapter 04 SolutionsDocument71 pagesMatter and Interaction Chapter 04 SolutionslangemarNo ratings yet

- TCS BaNCS Service Repository Document - ReverseUUIDDocument9 pagesTCS BaNCS Service Repository Document - ReverseUUIDMohit GuptaNo ratings yet

- New York Times Co v. United StatesDocument11 pagesNew York Times Co v. United StatesKenrey LicayanNo ratings yet

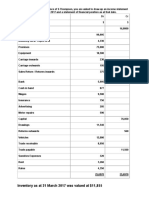

- Inventory As at 31 March 2017 Was Valued at $11,855Document2 pagesInventory As at 31 March 2017 Was Valued at $11,855Shoaib AslamNo ratings yet

- Accrued Expenses: Practice Question # 1Document4 pagesAccrued Expenses: Practice Question # 1Shoaib AslamNo ratings yet

- Scan 0002Document1 pageScan 0002Shoaib AslamNo ratings yet

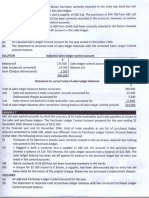

- Solution: 14.8 Advantages and Uses of Control AccountsDocument1 pageSolution: 14.8 Advantages and Uses of Control AccountsShoaib AslamNo ratings yet

- Control Accounts: Example 5Document1 pageControl Accounts: Example 5Shoaib AslamNo ratings yet

- Sample of Revision Plan - 10-cDocument3 pagesSample of Revision Plan - 10-cShoaib AslamNo ratings yet

- As Level Accounting Topic 1 OddDocument45 pagesAs Level Accounting Topic 1 OddShoaib AslamNo ratings yet

- Principles of Accounts: GCE Ordinary Level (2017) (Syllabus 7175)Document48 pagesPrinciples of Accounts: GCE Ordinary Level (2017) (Syllabus 7175)Shoaib AslamNo ratings yet

- Time Table IX M CrimsonDocument2 pagesTime Table IX M CrimsonShoaib AslamNo ratings yet

- Enterprise Architecture: Glossary ADocument4 pagesEnterprise Architecture: Glossary Amconde08No ratings yet

- Discovery On Tunnel DiodeDocument4 pagesDiscovery On Tunnel DiodeVaughan PngNo ratings yet

- Taxable Income and Tax DueDocument13 pagesTaxable Income and Tax DueSheena Gane Esteves100% (1)

- High Mast and Octagonal Poles CatalogueDocument5 pagesHigh Mast and Octagonal Poles CatalogueakhilNo ratings yet

- Tool BoxDocument6 pagesTool BoxSinar GemilangNo ratings yet

- What Is Sequence and Logic Control?Document6 pagesWhat Is Sequence and Logic Control?Marwan ShamsNo ratings yet

- What Things Do People Often Complain About in Your Country?: Complaint IsDocument5 pagesWhat Things Do People Often Complain About in Your Country?: Complaint IsTrần Ngọc Mỹ TâmNo ratings yet

- Contact Mechanics: Course OnDocument1 pageContact Mechanics: Course OnsanthoshnlNo ratings yet

- Paysliper Template Grid2Document5 pagesPaysliper Template Grid2Jeeva KumarNo ratings yet

- OVRS-1 Global Common Technical Specification For Production RobotsDocument63 pagesOVRS-1 Global Common Technical Specification For Production RobotsKask84No ratings yet

- Informe Milka Case StudyDocument5 pagesInforme Milka Case StudyCesar D. VillanuevaNo ratings yet

- The Growth Story of Mineral Water Industry in IndiaDocument2 pagesThe Growth Story of Mineral Water Industry in IndiaSNo ratings yet

- Mechanism Action of Fluorides II PedoDocument17 pagesMechanism Action of Fluorides II PedoFourthMolar.comNo ratings yet

- EAC MicroprojectDocument17 pagesEAC MicroprojectPrasad BurkuleNo ratings yet

- Resume SampleDocument1 pageResume SampleAnukrit AnilNo ratings yet

- Feasibility StudyDocument2 pagesFeasibility StudyNaths BarreraNo ratings yet

- Wavelength Routing Testbeds: Presented By, Bibi Mohanan M.Tech, OEC Roll No:7Document30 pagesWavelength Routing Testbeds: Presented By, Bibi Mohanan M.Tech, OEC Roll No:7Bibi Mohanan100% (1)

- Assistant Director For PlanningDocument4 pagesAssistant Director For PlanningSultan Kudarat State UniversityNo ratings yet

- Cocamide DEADocument1 pageCocamide DEADyah Putri Ayu DinastyarNo ratings yet

- A Statement Showing AssetsDocument2 pagesA Statement Showing AssetsNeha jainNo ratings yet

- NetcraftDocument9 pagesNetcraftapi-238604507No ratings yet

- Quantum Physics NotesDocument1 pageQuantum Physics NotesChloe InnsNo ratings yet