You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Module #1 in BookkeepingDocument3 pagesModule #1 in Bookkeepingrowena marambaNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Profe DevDocument29 pagesProfe Devrowena marambaNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- 3 Applied Economics - Quizzes & ActivitiesDocument3 pages3 Applied Economics - Quizzes & Activitiesrowena marambaNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- MODULE 3 Lesson 1 - Acitivites and QuizDocument3 pagesMODULE 3 Lesson 1 - Acitivites and Quizrowena marambaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- Applied Economics - Quizzes & ActivitiesDocument10 pagesApplied Economics - Quizzes & Activitiesrowena marambaNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- (Applied Econ.) Module 4. - Introduction To Applied EconomicsDocument5 pages(Applied Econ.) Module 4. - Introduction To Applied Economicsrowena marambaNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- (Applied Econ.) Module 3. - Introduction To Applied EconomicsDocument7 pages(Applied Econ.) Module 3. - Introduction To Applied Economicsrowena marambaNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- (Applied Econ.) Module 1 - Introduction To Applied Economics (Complete)Document8 pages(Applied Econ.) Module 1 - Introduction To Applied Economics (Complete)rowena marambaNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- (Applied Econ.) Module 2 - Application of Supply and Demand (Lesson Only)Document12 pages(Applied Econ.) Module 2 - Application of Supply and Demand (Lesson Only)rowena maramba100% (1)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Secretary's Certificate - Full Client ControlDocument4 pagesSecretary's Certificate - Full Client ControlseanNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Advanced Calculations: Unit StandardsDocument48 pagesAdvanced Calculations: Unit StandardsHrh Charmagne Thando NkosiNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Ahmed Abdalla Mohammed: ProfileDocument2 pagesAhmed Abdalla Mohammed: Profileahmed hajNo ratings yet

- Press Release: Easypay Now Offers Credit and Debit Card Processing To E-Commerce MerchantsDocument2 pagesPress Release: Easypay Now Offers Credit and Debit Card Processing To E-Commerce MerchantsHR ExecsNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Sunny SIPDocument29 pagesSunny SIPPritesh PampaniyaNo ratings yet

- Post Test Cash and Cash Equivalents Name: Date: Professor: Section: ScoreDocument5 pagesPost Test Cash and Cash Equivalents Name: Date: Professor: Section: ScoreRisa Castillo MiguelNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Financial Crisis of 2008: What Happened in Simple TermsDocument2 pagesThe Financial Crisis of 2008: What Happened in Simple TermsBig ALNo ratings yet

- A Study On Centralized and Decentralized Banking TechnologyDocument7 pagesA Study On Centralized and Decentralized Banking TechnologyMunuNo ratings yet

- Payoneer Pricing and Fees NON USv3Document1 pagePayoneer Pricing and Fees NON USv3azNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Visa Inc. - PaperDocument12 pagesVisa Inc. - PaperJen AdvientoNo ratings yet

- Civil and Criminal Liability For Dishonour of ChequeDocument17 pagesCivil and Criminal Liability For Dishonour of ChequeMalavika TNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- MEDICI Open BankingDocument14 pagesMEDICI Open BankingAkshay PrasathNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- LinksDocument1 pageLinksKokila ThangamNo ratings yet

- Sip Report On SbiDocument46 pagesSip Report On SbiRashmi RanjanNo ratings yet

- Finance Project AnjaliDocument37 pagesFinance Project AnjaliRushikesh MaidNo ratings yet

- Comparitive Analysis of Public Sector and Private Sectors Banks PDFDocument67 pagesComparitive Analysis of Public Sector and Private Sectors Banks PDFAnonymous y3E7ia100% (1)

- Detailed Procedure To Register A Vehicle in Luxembourg - May 2017Document4 pagesDetailed Procedure To Register A Vehicle in Luxembourg - May 2017Ting ohnNo ratings yet

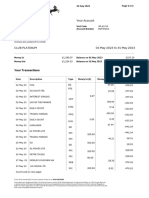

- Your Barclays Bank Account StatementDocument3 pagesYour Barclays Bank Account StatementSteven LeeNo ratings yet

- Postpaid Bill Anchal Jul 2022-1Document1 pagePostpaid Bill Anchal Jul 2022-1Mandhir BudhirajaNo ratings yet

- Jan HTC HOSTING LLC Allian Credit Union StatementDocument2 pagesJan HTC HOSTING LLC Allian Credit Union StatementJonathan Seagull LivingstonNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Fundamental of FinanceDocument48 pagesFundamental of FinanceIrrana ErissaNo ratings yet

- What Led To The Eventual Collapse of Enron Under Lay and Skilling?Document15 pagesWhat Led To The Eventual Collapse of Enron Under Lay and Skilling?Ananya MNo ratings yet

- CH.8 Notes - Accounting For ReceivablesDocument19 pagesCH.8 Notes - Accounting For ReceivablesLEEN hashemNo ratings yet

- 21072023, 010608 PDFDocument2 pages21072023, 010608 PDFCatalina-Elena100% (1)

- Co Signers Statement2Document2 pagesCo Signers Statement2Pharmastar Int'l Trading Corp.No ratings yet

- Economics MCQ E-BookDocument99 pagesEconomics MCQ E-BookRamanujam SinghNo ratings yet

- Harmony, Integrity, IndustryDocument6 pagesHarmony, Integrity, Industryjohn kevin pascuaNo ratings yet

- Basic Concepts Bank Reports: Big Picture B. Ulo BDocument26 pagesBasic Concepts Bank Reports: Big Picture B. Ulo BEDLYN MABUTINo ratings yet

- MGT162 Individual AssignmentDocument17 pagesMGT162 Individual AssignmentMEOR HAMIZAN MEOR MOHAMMAD FAREDNo ratings yet

- ApplicaionDocument41 pagesApplicaionRamesh MenonNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)