You might also like

- BUSINESS COMBINATION - PTDocument13 pagesBUSINESS COMBINATION - PTSchool FilesNo ratings yet

- Introduction of Partnership FormationDocument16 pagesIntroduction of Partnership FormationRamon AlpitcheNo ratings yet

- Chapter 1 Partnership Formation Test BanksDocument46 pagesChapter 1 Partnership Formation Test BanksRaisa Gelera91% (23)

- Partnership FormationDocument8 pagesPartnership FormationAira Kaye MartosNo ratings yet

- Group Accounts - ConsolidationDocument14 pagesGroup Accounts - ConsolidationWinnie GiveraNo ratings yet

- Consolidated FsDocument7 pagesConsolidated FsfreyawonderlandNo ratings yet

- PDF 325316809 Chapter 1 Partnership Formation Test Banks Docxdocx DLDocument46 pagesPDF 325316809 Chapter 1 Partnership Formation Test Banks Docxdocx DLSofia SerranoNo ratings yet

- Business Combination Problems SolutionsDocument12 pagesBusiness Combination Problems Solutionsnana100% (2)

- Far Pet Class - Mock Quiz CorporationDocument11 pagesFar Pet Class - Mock Quiz CorporationNia BranzuelaNo ratings yet

- BADVAC1X MOD 1 Business CombiDocument4 pagesBADVAC1X MOD 1 Business CombiRalph Lawrence Francisco BatangasNo ratings yet

- Mindanao State University - Marawi City College of Business Administration and Accountancy Accountancy Department 2 Semester, AY 2015-2016Document9 pagesMindanao State University - Marawi City College of Business Administration and Accountancy Accountancy Department 2 Semester, AY 2015-2016Sittie Ainna A. UnteNo ratings yet

- JOINT OPERATION FORMATIONDocument7 pagesJOINT OPERATION FORMATIONChristine Jane Abang100% (1)

- Practice Set 1 ABC-3Document3 pagesPractice Set 1 ABC-3reiNo ratings yet

- Partnership Formation GuideDocument9 pagesPartnership Formation GuideKhim CortezNo ratings yet

- Ernie and Bert Form PartnershipDocument35 pagesErnie and Bert Form PartnershipxjammerNo ratings yet

- SPECTRAN_Corpo-LiquidationDocument11 pagesSPECTRAN_Corpo-LiquidationJhon RenomeronNo ratings yet

- Partnership-FormationDocument47 pagesPartnership-FormationStudent 101No ratings yet

- C1 Business Combi AssignmentDocument2 pagesC1 Business Combi AssignmentkimberlyroseabianNo ratings yet

- Accounting For Business CombinationDocument17 pagesAccounting For Business CombinationTrace ReyesNo ratings yet

- Indicate Whether The Statement Is True or FalseDocument11 pagesIndicate Whether The Statement Is True or Falseryan rosalesNo ratings yet

- AFARDocument16 pagesAFARCheska MangahasNo ratings yet

- AFAR December 2021 CPA Exam ReviewDocument19 pagesAFAR December 2021 CPA Exam ReviewT-306 Caturla FairyzenNo ratings yet

- Topic 2 Complex GroupDocument11 pagesTopic 2 Complex GroupSpencerNo ratings yet

- Week 7 NotesDocument6 pagesWeek 7 NotescalebNo ratings yet

- Chapter 1 Partnership Formation Test BanksDocument49 pagesChapter 1 Partnership Formation Test BanksLizza Marie Casidsid90% (20)

- AFARDocument41 pagesAFARAlican, JerhamelNo ratings yet

- C10 - PAS 7 Statement of Cash FlowsDocument15 pagesC10 - PAS 7 Statement of Cash FlowsAllaine Elfa100% (2)

- Chapter 8 Consolidation IDocument18 pagesChapter 8 Consolidation IAkkama100% (1)

- Lesson 1 Partnership FormationDocument21 pagesLesson 1 Partnership FormationDan Gabrielle SalacNo ratings yet

- Exercises: Method. Under This Form Expenses Are Aggregated According To Their Nature and NotDocument15 pagesExercises: Method. Under This Form Expenses Are Aggregated According To Their Nature and NotCherry Doong CuantiosoNo ratings yet

- Assignment-1-Intermediate-Accounting - PERDIZO, MILJANE P.Document8 pagesAssignment-1-Intermediate-Accounting - PERDIZO, MILJANE P.Miljane PerdizoNo ratings yet

- Chapter 15Document12 pagesChapter 15TRINH DUC DIEPNo ratings yet

- IFRS 3 Business Combination AccountingDocument4 pagesIFRS 3 Business Combination AccountingMarvinNo ratings yet

- 15 Business CombinationDocument6 pages15 Business CombinationTinNo ratings yet

- Accounting for Business CombinationsDocument52 pagesAccounting for Business CombinationsXavier AresNo ratings yet

- ACFrOgBKylWIFKqvQUoX2Yag018eml8V2evCY-xyBCergd9v5HXZoTbU3Q8kgtUcNC 5mafD1Hk933Hbe5goLmzsLjTjnum6IB4inPQsm6vrTPgbDppndlBKfMysfn8Document28 pagesACFrOgBKylWIFKqvQUoX2Yag018eml8V2evCY-xyBCergd9v5HXZoTbU3Q8kgtUcNC 5mafD1Hk933Hbe5goLmzsLjTjnum6IB4inPQsm6vrTPgbDppndlBKfMysfn8rodell pabloNo ratings yet

- CPA Review School ConsolidationDocument18 pagesCPA Review School ConsolidationMellaniNo ratings yet

- Finacct Mock Exam 1Document7 pagesFinacct Mock Exam 1Joseph Gerald M. ArcegaNo ratings yet

- 9419 - Joint ArrangementDocument4 pages9419 - Joint Arrangementjsmozol3434qcNo ratings yet

- Introduction To Partnership Accounting For Partnership FormationDocument19 pagesIntroduction To Partnership Accounting For Partnership FormationKarl SolomeroNo ratings yet

- Consalidated Statement of Profit and LossDocument40 pagesConsalidated Statement of Profit and LossG. DhanyaNo ratings yet

- Dry RunDocument5 pagesDry RunMarc MagbalonNo ratings yet

- Homework PDFDocument8 pagesHomework PDFTracey NguyenNo ratings yet

- Chapter Five PrintDocument18 pagesChapter Five PrintGedionNo ratings yet

- Acctg 029 - Mod 2 Conso Fs Date of AcqDocument6 pagesAcctg 029 - Mod 2 Conso Fs Date of AcqAlliah Nicole RamosNo ratings yet

- Eos Cupfinal RoundDocument7 pagesEos Cupfinal RoundSheena Pearl AlinsanganNo ratings yet

- Accounting For Partnership FARDocument31 pagesAccounting For Partnership FARlousevero10No ratings yet

- p2 - Guerrero Ch9Document49 pagesp2 - Guerrero Ch9JerichoPedragosa72% (36)

- Handouts 1 Partnership AccountingDocument5 pagesHandouts 1 Partnership AccountingRozel MontevirgenNo ratings yet

- IFRS 3 Business CombinationDocument15 pagesIFRS 3 Business CombinationAquino KimalexerNo ratings yet

- 1-Formation-1Document7 pages1-Formation-1martinfaith958No ratings yet

- P2 MaterialsDocument9 pagesP2 MaterialsmarygraceomacNo ratings yet

- Paper - 1: Financial Reporting Questions Ind AS 103Document30 pagesPaper - 1: Financial Reporting Questions Ind AS 103sam kapoorNo ratings yet

- Aa BcprelimsDocument4 pagesAa BcprelimsJamie RamosNo ratings yet

- Multiple Choice ACCSTDocument5 pagesMultiple Choice ACCSTJaene L.No ratings yet

- Advanced Financial Accounting and Reporting Qualifying RoundDocument24 pagesAdvanced Financial Accounting and Reporting Qualifying RoundJessa BeloyNo ratings yet

- Statement of Cash Flows & Book Value per Share PreparedDocument67 pagesStatement of Cash Flows & Book Value per Share PreparedKaren MagsayoNo ratings yet

- 'Ora Pro Nobis' (Fight For Us)Document4 pages'Ora Pro Nobis' (Fight For Us)Zandrea LopezNo ratings yet

- QUIZ 1 - PrelimDocument6 pagesQUIZ 1 - PrelimZandrea LopezNo ratings yet

- CompilationDocument10 pagesCompilationZandrea LopezNo ratings yet

- Practice Exercise 1Document2 pagesPractice Exercise 1Zandrea LopezNo ratings yet

- Business Combination Exercise 2Document1 pageBusiness Combination Exercise 2Zandrea LopezNo ratings yet

- Bsa3101 Bsa2e Pa1 Lopez ZandreaDocument2 pagesBsa3101 Bsa2e Pa1 Lopez ZandreaZandrea LopezNo ratings yet

- A. Taxes On Real PropertyDocument9 pagesA. Taxes On Real PropertyZandrea LopezNo ratings yet

- GROUP 1 Strategic Capacity Planning For Products and ServicesDocument99 pagesGROUP 1 Strategic Capacity Planning For Products and ServicesZandrea LopezNo ratings yet

- Managerial AccountingDocument4 pagesManagerial AccountingZandrea LopezNo ratings yet

- Flora, Gianne Patricia Lisboa, John Jacob Lopez, Zandrea Maligson, Sherilyn Metilla, Paula Jean Quebral, Pamela Angela Santos, Camille AnneDocument52 pagesFlora, Gianne Patricia Lisboa, John Jacob Lopez, Zandrea Maligson, Sherilyn Metilla, Paula Jean Quebral, Pamela Angela Santos, Camille AnneZandrea LopezNo ratings yet

- Discussion Problems and Solutions On Module 3, Part 1Document28 pagesDiscussion Problems and Solutions On Module 3, Part 1AJ Biagan MoraNo ratings yet

- ENTRIESDocument14 pagesENTRIESZandrea LopezNo ratings yet

- ENTRIESDocument14 pagesENTRIESZandrea LopezNo ratings yet

- Home Loan Lap Disbursement ChecklistDocument1 pageHome Loan Lap Disbursement ChecklistJaved QasimNo ratings yet

- Super Bond Adhesives Private LimitedDocument22 pagesSuper Bond Adhesives Private Limitedvikasaggarwal01No ratings yet

- Tax GuidesDocument25 pagesTax Guidesjr7mondo7edoNo ratings yet

- Equity Research Summer ProjectDocument66 pagesEquity Research Summer Projectpajhaveri4009No ratings yet

- Global Markets: Third Storm (Tight Monitory Policy)Document8 pagesGlobal Markets: Third Storm (Tight Monitory Policy)Rohan ShahNo ratings yet

- Real Estate Deed of SaleDocument3 pagesReal Estate Deed of SaleAiron Bendaña100% (1)

- Accounting Manager or Financial Reporting or Financial ReportingDocument4 pagesAccounting Manager or Financial Reporting or Financial Reportingapi-121650574No ratings yet

- Uganda Implementing An IFMSDocument6 pagesUganda Implementing An IFMSkhan_sadi100% (1)

- Home and Branch Journal Entries (Markup) PDFDocument1 pageHome and Branch Journal Entries (Markup) PDFAbraham ChinNo ratings yet

- Dynacon Systems Ar 2017 5323650317Document101 pagesDynacon Systems Ar 2017 5323650317murali_pmp1766No ratings yet

- DXOCw IKasz ZWD HRDocument6 pagesDXOCw IKasz ZWD HRRabindra SinghNo ratings yet

- FinancialManagement Mplte ChoiceDocument18 pagesFinancialManagement Mplte ChoiceCrish NaNo ratings yet

- Project ReportDocument65 pagesProject ReportstafanaNo ratings yet

- Investment in Equity Securities - IA1Document17 pagesInvestment in Equity Securities - IA1dumpyforhimNo ratings yet

- Capital Balances and Profit DistributionDocument4 pagesCapital Balances and Profit DistributionLorraine Mae RobridoNo ratings yet

- Letter of ComplianceDocument1 pageLetter of ComplianceWill PridmoreNo ratings yet

- Affidavit Adequate Assurance of Due Performance Ameriquest MortgageDocument5 pagesAffidavit Adequate Assurance of Due Performance Ameriquest MortgageBernie Jones100% (2)

- Applications of Integration To Business, Economics and Life Sciences - HandoutDocument32 pagesApplications of Integration To Business, Economics and Life Sciences - HandoutTran Nguyen KhangNo ratings yet

- RR Sortino A Sharper RatioDocument6 pagesRR Sortino A Sharper Ratiokostistriant30No ratings yet

- Emba 2014 2015 Exec Mba - OxfordDocument36 pagesEmba 2014 2015 Exec Mba - OxfordAjay DevNo ratings yet

- 2023-07-12T02-55 Transaction #6425979030853126-12676821Document1 page2023-07-12T02-55 Transaction #6425979030853126-12676821mananwu07246No ratings yet

- Fixed DepositsDocument2 pagesFixed DepositsNarendrapratap1No ratings yet

- Kse 100 IndexDocument49 pagesKse 100 IndexayazNo ratings yet

- Ibm Cognos ProspectingDocument3 pagesIbm Cognos ProspectingtasvirkhaliliNo ratings yet

- FM 415 - Chapter 2A PDFDocument14 pagesFM 415 - Chapter 2A PDFMarc Charles UsonNo ratings yet

- Savings Withdrawal Form As of 042715nologo1Document1 pageSavings Withdrawal Form As of 042715nologo1Raymond Patrick Bandola SoriaNo ratings yet

- Central Bank-Monetary Policy ReviewDocument6 pagesCentral Bank-Monetary Policy ReviewAda DeranaNo ratings yet

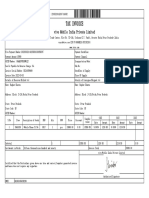

- Tax Invoice: Vivo Mobile India Private LimitedDocument1 pageTax Invoice: Vivo Mobile India Private LimitedRaghav SharmaNo ratings yet

- One Step Beyond Is The Public Sector Ready PDFDocument27 pagesOne Step Beyond Is The Public Sector Ready PDFMuhammad makhrojalNo ratings yet

- Accounting Cycle HacksDocument14 pagesAccounting Cycle HacksAnonymous mnAAXLkYQCNo ratings yet