You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Salary Slips 3Document2 pagesSalary Slips 3Pramod KumarNo ratings yet

- Resolution by Self Help Group For Opening Savings AccountDocument9 pagesResolution by Self Help Group For Opening Savings Accountvvivek22No ratings yet

- Form B: (See Sub-Paragraphs (2), (3) and (7) of Paragraph 7)Document2 pagesForm B: (See Sub-Paragraphs (2), (3) and (7) of Paragraph 7)vvivek22No ratings yet

- Diploma in Banking & Finance Examination - July 2014 (Online Mode)Document1 pageDiploma in Banking & Finance Examination - July 2014 (Online Mode)vvivek22No ratings yet

- Finacle 19A - Cbs Menu - UpgbDocument27 pagesFinacle 19A - Cbs Menu - UpgbyezdiarwNo ratings yet

- 2 Quick Success Series BPRDocument8 pages2 Quick Success Series BPRvvivek22No ratings yet

- Train LawDocument23 pagesTrain LawDennis BudanoNo ratings yet

- Proforma Profits Tax ComputationDocument2 pagesProforma Profits Tax ComputationVintonius Raffaele PRIMUSNo ratings yet

- Talenta Payslip Margaria Batik Okt 2023 NooryatiDocument3 pagesTalenta Payslip Margaria Batik Okt 2023 Nooryatinoryati939No ratings yet

- Invoice: Peninsular Maritime India PVT LTDDocument2 pagesInvoice: Peninsular Maritime India PVT LTDShravan KumarNo ratings yet

- Bir Ruling Da JV 039 379 078Document5 pagesBir Ruling Da JV 039 379 078Alfred Hernandez CampañanoNo ratings yet

- LT Check Printing Report. 5-5pdfDocument1 pageLT Check Printing Report. 5-5pdfKelton ShieldsNo ratings yet

- Bir - Train - It & WT - 20180418Document87 pagesBir - Train - It & WT - 20180418Corrine AbucejoNo ratings yet

- Chapter 3 Income TaxationDocument7 pagesChapter 3 Income TaxationMary Jane PabroaNo ratings yet

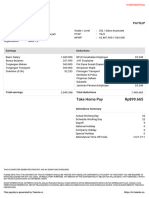

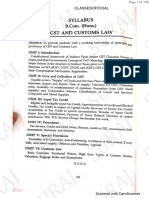

- GST Shiv Das Bcom (H)Document149 pagesGST Shiv Das Bcom (H)132komalprasadNo ratings yet

- VAT 101e: Value-Added TaxDocument5 pagesVAT 101e: Value-Added Taxdarl1No ratings yet

- Taxation CompressDocument3 pagesTaxation CompressJulie BagaresNo ratings yet

- Opening My Account: Statement of AcceptanceDocument6 pagesOpening My Account: Statement of AcceptanceMiroslav ŽivadinovićNo ratings yet

- Life Long Gas Stove Bill InvoiceDocument1 pageLife Long Gas Stove Bill Invoicesreenivas100% (1)

- 1996 Financial StatementsDocument634 pages1996 Financial Statements!nCrypted!No ratings yet

- Macro CH 10Document31 pagesMacro CH 10Tanisha TibrewalNo ratings yet

- Business Structures Advantages and Disadvantages of Common Business StructuresDocument2 pagesBusiness Structures Advantages and Disadvantages of Common Business StructuresShariBarry123No ratings yet

- Evaluate 2 - Donor's TaxDocument5 pagesEvaluate 2 - Donor's TaxNicolas AlonsoNo ratings yet

- Myntra 2Document2 pagesMyntra 2Prapti ShahNo ratings yet

- Accounting For PayrollDocument15 pagesAccounting For PayrollDenise Aubrey GallardoNo ratings yet

- Tax Credit Claim Form 2020: For Donation Claims OnlyDocument2 pagesTax Credit Claim Form 2020: For Donation Claims OnlyVivian KongNo ratings yet

- GST ChallanDocument2 pagesGST Challanmohammad TabishNo ratings yet

- Olmstead Corporation S Capital Structure Is As Follows The Following Additional InformationDocument1 pageOlmstead Corporation S Capital Structure Is As Follows The Following Additional InformationHassan JanNo ratings yet

- DurgeshDocument1 pageDurgeshDavid AleNo ratings yet

- Cta Eb CV 01734 D 2019mar29 AssDocument24 pagesCta Eb CV 01734 D 2019mar29 AssAnna Dela VegaNo ratings yet

- Billing Statement: C/o RCL Feeders Phils., Inc (Agent)Document1 pageBilling Statement: C/o RCL Feeders Phils., Inc (Agent)ImaeRoseVallespinNo ratings yet

- CSB Touch - FATCA-FormDocument1 pageCSB Touch - FATCA-FormAkhil C JoyNo ratings yet

- Mouse PadDocument2 pagesMouse Pad20MA32 - PRABAVATHI TNo ratings yet

- Payment Receipt: Applicant DetailsDocument1 pagePayment Receipt: Applicant Detailsakhil SrinadhuNo ratings yet

- Capital Budgeting Case StudyDocument1 pageCapital Budgeting Case StudySunil Vadhva100% (1)