You might also like

- Basel 2.5, Basel III. Their Tasks Are To Identify Risks To The Financial Stability of TheDocument5 pagesBasel 2.5, Basel III. Their Tasks Are To Identify Risks To The Financial Stability of TheSahoo SKNo ratings yet

- Understanding Dodd-Frank Wall Street Reform ActDocument3 pagesUnderstanding Dodd-Frank Wall Street Reform ActCL AhNo ratings yet

- Dodd-Frank Wallstreet Finance ReformDocument17 pagesDodd-Frank Wallstreet Finance ReformStad Ics100% (1)

- Dodd Frank Explained - CNBCDocument3 pagesDodd Frank Explained - CNBCAks SukhtankarNo ratings yet

- Dodd FrankactDocument3 pagesDodd FrankactPamela Moore YoungNo ratings yet

- FinTech Rising: Navigating the maze of US & EU regulationsFrom EverandFinTech Rising: Navigating the maze of US & EU regulationsRating: 5 out of 5 stars5/5 (1)

- FIRE 441 Summer 2015 Final Examination Review Guide.Document3 pagesFIRE 441 Summer 2015 Final Examination Review Guide.Osman Malik-FoxNo ratings yet

- So How Does This Affect Me? A Commercial Borrower's Perspective of The Dodd Frank Wall Street Reform and Consumer Protection ActDocument6 pagesSo How Does This Affect Me? A Commercial Borrower's Perspective of The Dodd Frank Wall Street Reform and Consumer Protection ActArnstein & Lehr LLPNo ratings yet

- Dodd Frank Act-2016088Document18 pagesDodd Frank Act-2016088nikhilNo ratings yet

- Financial Regulation PrimerDocument8 pagesFinancial Regulation Primeraxsinn9016No ratings yet

- Chapter 3 Book AnswersDocument14 pagesChapter 3 Book AnswersKaia LorenzoNo ratings yet

- Chapter 3Document33 pagesChapter 3mokeNo ratings yet

- Trends Winter 2013Document16 pagesTrends Winter 2013caitlynharveyNo ratings yet

- Via Email FilingDocument4 pagesVia Email FilingMarketsWikiNo ratings yet

- 2ee7388d-bfc6-4aa9-8c58-ecfe184a85e6Document43 pages2ee7388d-bfc6-4aa9-8c58-ecfe184a85e6Troy StrawnNo ratings yet

- Investment TermpaperDocument9 pagesInvestment TermpaperMichael HessNo ratings yet

- BASEL 3 (Stricter Bank Capital Limits Causing Concern of Liquidity and Credit Availability)Document4 pagesBASEL 3 (Stricter Bank Capital Limits Causing Concern of Liquidity and Credit Availability)Mickey SNo ratings yet

- Three Models of Financial RegulationDocument16 pagesThree Models of Financial RegulationRamjunum RandhirsinghNo ratings yet

- Chapter 19 Banking Industry Structure and CompetitionDocument5 pagesChapter 19 Banking Industry Structure and CompetitionRenz VillaramaNo ratings yet

- Goldman SachsDocument22 pagesGoldman SachsMarketsWikiNo ratings yet

- Dodd-Frank Wall Street Reform and Consumer Protection ActDocument34 pagesDodd-Frank Wall Street Reform and Consumer Protection ActJohn M. AnthonyNo ratings yet

- 11 Final July 15Document22 pages11 Final July 15MarketsWikiNo ratings yet

- Dodd-Frank Act Explained: What It Does and CriticismsDocument3 pagesDodd-Frank Act Explained: What It Does and CriticismsFarwa Muhammad SaleemNo ratings yet

- Bank Organization and RegulationDocument66 pagesBank Organization and RegulationPuput AjaNo ratings yet

- Solution Manual For Bank Management and Financial Services 9th Edition Rose Hudgins 0078034671 9780078034671Document36 pagesSolution Manual For Bank Management and Financial Services 9th Edition Rose Hudgins 0078034671 9780078034671charlesblackdmpscxyrfi100% (29)

- BIP 390 Investment Banking RegulationsDocument38 pagesBIP 390 Investment Banking RegulationsDuc Bui100% (2)

- Chapter 13Document4 pagesChapter 13Divid RomanyNo ratings yet

- Trustees Versus Fiscal Agents For Sovereign Bonds: Lee C. BuchheitDocument5 pagesTrustees Versus Fiscal Agents For Sovereign Bonds: Lee C. BuchheitAqsa ParveenNo ratings yet

- Resolution Plans Required For Insured Depository Institutions With $50 Bilion or More inDocument55 pagesResolution Plans Required For Insured Depository Institutions With $50 Bilion or More inForeclosure FraudNo ratings yet

- After Crisis of 2007Document6 pagesAfter Crisis of 2007LauraTarantinoNo ratings yet

- Bank Management and Financial Services 9th Edition Rose Solutions ManualDocument26 pagesBank Management and Financial Services 9th Edition Rose Solutions ManualMelanieThorntonbcmk100% (57)

- Banking Law RésuméDocument9 pagesBanking Law Résumémayssaferjani011No ratings yet

- Oversight of Basel Iii: Impact of Proposed Capital RulesDocument147 pagesOversight of Basel Iii: Impact of Proposed Capital RulesScribd Government DocsNo ratings yet

- Corporate Governance Is The Set ofDocument16 pagesCorporate Governance Is The Set ofMazhar SarwashNo ratings yet

- IMCh 02Document13 pagesIMCh 02Sakub Amin Sick'L'No ratings yet

- His Issue of The Akron Law Review: Historical PerspectiveDocument94 pagesHis Issue of The Akron Law Review: Historical Perspectivesam mammoNo ratings yet

- Holding bankers to account: A decade of market manipulation, regulatory failures and regulatory reformsFrom EverandHolding bankers to account: A decade of market manipulation, regulatory failures and regulatory reformsNo ratings yet

- Summary Dodd Frank ActDocument28 pagesSummary Dodd Frank ActederekNo ratings yet

- Banking and The Financial Services Industry: Chapter 1 Book 1Document20 pagesBanking and The Financial Services Industry: Chapter 1 Book 1yeehawwwwNo ratings yet

- The Dodd Frank Act A Cheat Sheet: Morrison FoersterDocument28 pagesThe Dodd Frank Act A Cheat Sheet: Morrison Foerstervikramgill1No ratings yet

- The B.E. Journal of Economic Analysis & Policy: TopicsDocument30 pagesThe B.E. Journal of Economic Analysis & Policy: TopicsShahban KhanNo ratings yet

- Class 1901 MaterialsDocument14 pagesClass 1901 MaterialsandreaNo ratings yet

- R40249 - Who Regulates Whom? An Overview of U.S. Financial SupervisionDocument40 pagesR40249 - Who Regulates Whom? An Overview of U.S. Financial SupervisionbowssenNo ratings yet

- Topic US Banking SystemDocument13 pagesTopic US Banking SystemNastia VasilenkoNo ratings yet

- Dodd-Frank Act Honor ResearchDocument7 pagesDodd-Frank Act Honor ResearchLinh KinNo ratings yet

- Federal Register / Vol. 76, No. 221 / Wednesday, November 16, 2011 / Rules and RegulationsDocument112 pagesFederal Register / Vol. 76, No. 221 / Wednesday, November 16, 2011 / Rules and RegulationsMarketsWikiNo ratings yet

- Banking Regulations: Reasons For The Regulation of BanksDocument6 pagesBanking Regulations: Reasons For The Regulation of BanksMarwa HassanNo ratings yet

- Bank of AmericaDocument113 pagesBank of AmericaMarketsWikiNo ratings yet

- The New Financial Deal: Understanding the Dodd-Frank Act and Its (Unintended) ConsequencesFrom EverandThe New Financial Deal: Understanding the Dodd-Frank Act and Its (Unintended) ConsequencesNo ratings yet

- Raising Money – Legally: A Practical Guide to Raising CapitalFrom EverandRaising Money – Legally: A Practical Guide to Raising CapitalRating: 4 out of 5 stars4/5 (1)

- Senator Chris Dodd - Statement On Financial RegulationDocument11 pagesSenator Chris Dodd - Statement On Financial RegulationrebeltradersNo ratings yet

- Is It The End of The Road For Wall Street Banks?-VRK100-28062010Document4 pagesIs It The End of The Road For Wall Street Banks?-VRK100-28062010RamaKrishna Vadlamudi, CFANo ratings yet

- What If Nothing Is Risk Free?: SATURDAY, JULY 24, 2010Document11 pagesWhat If Nothing Is Risk Free?: SATURDAY, JULY 24, 2010priyankaaneja24gmailNo ratings yet

- Regulating The Shadow Banking System: TH THDocument55 pagesRegulating The Shadow Banking System: TH THmyscribd0003No ratings yet

- Rules and Regulations: Register That Proposed To RequireDocument11 pagesRules and Regulations: Register That Proposed To RequireMarketsWikiNo ratings yet

- The Savings and Loan Crisis: Deregulation and its ConsequencesDocument2 pagesThe Savings and Loan Crisis: Deregulation and its ConsequencestylerNo ratings yet

- Frank Dodd SummaryDocument10 pagesFrank Dodd SummaryDonnaAntonucciNo ratings yet

- The Federal Reserve's Role in Banking Supervision and Mortgage RegulationDocument24 pagesThe Federal Reserve's Role in Banking Supervision and Mortgage Regulationaslater00No ratings yet

- 1A. Statement in Support of The Application - Rev.1Document25 pages1A. Statement in Support of The Application - Rev.1David HundeyinNo ratings yet

- Cooperation Department in BengalDocument1 pageCooperation Department in BengalK Srinivasa MurthyNo ratings yet

- PCHC ChargesDocument1 pagePCHC ChargesCJNo ratings yet

- Business Continuity PlanDocument1 pageBusiness Continuity PlanasshhwiniNo ratings yet

- Fixed Deposits - November 22 2021Document1 pageFixed Deposits - November 22 2021Lisle Daverin BlythNo ratings yet

- Guide Emerging Market Currencies 2010Document128 pagesGuide Emerging Market Currencies 2010ferrarilover2000No ratings yet

- Calculating Capital Adequacy RatiosDocument4 pagesCalculating Capital Adequacy Ratiosshuvo dasNo ratings yet

- The Refinancing of Shanghai General MotorsDocument23 pagesThe Refinancing of Shanghai General MotorsAdrija Chakraborty100% (2)

- 8 Payment Methods and How To Accept Each Payment Mode - StaxDocument12 pages8 Payment Methods and How To Accept Each Payment Mode - StaxZACHARIAH MANKIRNo ratings yet

- Chapter 3: Calculating Mortgage ReturnsDocument14 pagesChapter 3: Calculating Mortgage Returnsbaorunchen100% (1)

- "Study On Loan and Credit Facility at SDCC Bank, Rourkela ": Summer Internship Project Report OnDocument81 pages"Study On Loan and Credit Facility at SDCC Bank, Rourkela ": Summer Internship Project Report OnASIT EKKANo ratings yet

- MA170 Chapter 1Document8 pagesMA170 Chapter 1ishanissantaNo ratings yet

- Central Bank of Sri Lanka: Objectives, Functions & OrganizationDocument32 pagesCentral Bank of Sri Lanka: Objectives, Functions & OrganizationAsiri GunarathnaNo ratings yet

- Basel II and Credit RiskDocument18 pagesBasel II and Credit RiskVasuki BoopathyNo ratings yet

- Tutorial Solution Chap 5Document4 pagesTutorial Solution Chap 5Nurul AriffahNo ratings yet

- Bank charges schedule breakdownDocument26 pagesBank charges schedule breakdownMaria FayyazNo ratings yet

- Perkembangan Sistem Pembayaran Non Tunai Pada Era Revolusi Industri 4Document5 pagesPerkembangan Sistem Pembayaran Non Tunai Pada Era Revolusi Industri 4fadhila faquanikaNo ratings yet

- Data Analysis On Financial InclusionDocument21 pagesData Analysis On Financial InclusionHeidi Bell50% (2)

- Soa 23on81273 May2022Document2 pagesSoa 23on81273 May2022Nyari RecehNo ratings yet

- Chapter 13 Sources of FinanceDocument4 pagesChapter 13 Sources of Financeapi-302252730No ratings yet

- Rupay Vs VisaDocument5 pagesRupay Vs VisaSriya KannegantiNo ratings yet

- Central Banking and Monetary Policy ExplainedDocument59 pagesCentral Banking and Monetary Policy ExplainedNherwin OstiaNo ratings yet

- Request Jud Not W Motion Joinder 4-29-13 0Document518 pagesRequest Jud Not W Motion Joinder 4-29-13 0Nancy Duffy McCarronNo ratings yet

- Mathematics of FinanceDocument22 pagesMathematics of FinanceJean Espanto100% (4)

- Acquisition of Merrill Lynch by Bank of AmericaDocument26 pagesAcquisition of Merrill Lynch by Bank of AmericaNancy AggarwalNo ratings yet

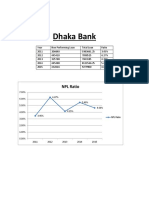

- Dhaka Bank NPL Ratio and Amount Over TimeDocument2 pagesDhaka Bank NPL Ratio and Amount Over TimeRaihan AhsanNo ratings yet

- Working Capital CommitteeDocument16 pagesWorking Capital Committeevivekkheta100% (1)

- Development Financial InstitutionsDocument9 pagesDevelopment Financial Institutionsapi-3739522No ratings yet

- Internship Report On Soneri Bank LimitedDocument78 pagesInternship Report On Soneri Bank LimitedZubair Khan50% (2)

- Loan Application ProcessDocument2 pagesLoan Application ProcessWinning EdgeNo ratings yet