You might also like

- Pfrs 7 Financial Instruments DisclosuresDocument3 pagesPfrs 7 Financial Instruments DisclosuresR.A.No ratings yet

- Pfrs 15 Revenue From Contracts With CustomersDocument3 pagesPfrs 15 Revenue From Contracts With CustomersR.A.No ratings yet

- Pfrs 17 Insurance ContractsDocument3 pagesPfrs 17 Insurance ContractsR.A.No ratings yet

- Pfrs 1 First-Time Adoptation of Philippine Financial Reporting StandardsDocument3 pagesPfrs 1 First-Time Adoptation of Philippine Financial Reporting StandardsR.A.No ratings yet

- Pfrs 16 LeasesDocument4 pagesPfrs 16 LeasesR.A.No ratings yet

- Pfrs 2 Share-Based PaymentsDocument3 pagesPfrs 2 Share-Based PaymentsR.A.No ratings yet

- Pas 28 Investments in Associates and Joint VenturesDocument2 pagesPas 28 Investments in Associates and Joint VenturesR.A.No ratings yet

- Pas 41 AgricultureDocument2 pagesPas 41 AgricultureR.A.No ratings yet

- Pfrs 12 Disclosure of Interests in Other EntitiesDocument2 pagesPfrs 12 Disclosure of Interests in Other EntitiesR.A.No ratings yet

- Pas 36 Impairment of AssetsDocument2 pagesPas 36 Impairment of AssetsR.A.No ratings yet

- Pas 40 Investment PropertyDocument3 pagesPas 40 Investment PropertyR.A.No ratings yet

- Pas 2 Inventories: I. NatureDocument2 pagesPas 2 Inventories: I. NatureR.A.No ratings yet

- Pas 21 The Effects of Changes in Foreign Exchange RatesDocument2 pagesPas 21 The Effects of Changes in Foreign Exchange RatesR.A.No ratings yet

- Pas 29 Financial Reporting in Hyperinflationary EconomiesDocument2 pagesPas 29 Financial Reporting in Hyperinflationary EconomiesR.A.No ratings yet

- Pas 32 Financial InstrumentsDocument2 pagesPas 32 Financial InstrumentsR.A.No ratings yet

- Pas 24 Related Party DisclosureDocument3 pagesPas 24 Related Party DisclosureR.A.No ratings yet

- Pas 12 Income TaxesDocument3 pagesPas 12 Income TaxesR.A.No ratings yet

- Pas 20 Accounting For Government Grants and Disclosure of Government AssistanceDocument2 pagesPas 20 Accounting For Government Grants and Disclosure of Government AssistanceR.A.No ratings yet

- Pas 33 Earnings Per Share: I. NatureDocument3 pagesPas 33 Earnings Per Share: I. NatureR.A.No ratings yet

- Pas 1 Presentation of Financial StatementsDocument8 pagesPas 1 Presentation of Financial StatementsR.A.100% (1)

- Pas 26 Accounting and Reporting by Retirement Benefit PlansDocument2 pagesPas 26 Accounting and Reporting by Retirement Benefit PlansR.A.No ratings yet

- Conceptual Framework and Accounting Standards: I. NatureDocument4 pagesConceptual Framework and Accounting Standards: I. NatureR.A.No ratings yet

- Pas 16 Property, Plant, and Equipment: I. NatureDocument2 pagesPas 16 Property, Plant, and Equipment: I. NatureR.A.No ratings yet

- Conceptual Framework and Accounting Standards: I. NatureDocument4 pagesConceptual Framework and Accounting Standards: I. NatureR.A.No ratings yet

- Pas 7 Statement of Cash FlowsDocument2 pagesPas 7 Statement of Cash FlowsR.A.No ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Package 1 (LT 1 - 6) Includes TutorialsDocument102 pagesPackage 1 (LT 1 - 6) Includes TutorialsjacechanNo ratings yet

- Invoice Receipt RAJESH MONDALDocument1 pageInvoice Receipt RAJESH MONDALsouvikNo ratings yet

- Chapter 4Document50 pagesChapter 4carlo knowsNo ratings yet

- AME Lean Manufacturing AssessmentDocument35 pagesAME Lean Manufacturing AssessmentacauaNo ratings yet

- Accounting Warren 23rd Edition Solutions ManualDocument54 pagesAccounting Warren 23rd Edition Solutions Manualbrennadrusillas7zNo ratings yet

- Final Accounts: Receipts & Expenditure Adjustment & Closing Entries Final Accounts of Manufacturing ConcernsDocument9 pagesFinal Accounts: Receipts & Expenditure Adjustment & Closing Entries Final Accounts of Manufacturing ConcernsVidhi Patel100% (1)

- CHAPTER 2 Accounting Equation and The Double Entry SystemDocument2 pagesCHAPTER 2 Accounting Equation and The Double Entry SystemGabrielle Joshebed AbaricoNo ratings yet

- PT Anabatic Technologies TBK Dan Entitas Anaknya/And Its SubsidiariesDocument231 pagesPT Anabatic Technologies TBK Dan Entitas Anaknya/And Its SubsidiariesDhesi Bintang ShafitriNo ratings yet

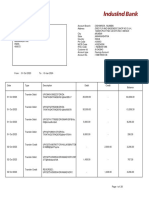

- Bank Statement IndusindDocument28 pagesBank Statement IndusindRohit RajagopalNo ratings yet

- Step 1: Analysis of The Subsidiary's Net AssetsDocument10 pagesStep 1: Analysis of The Subsidiary's Net AssetsJulie Mae Caling MalitNo ratings yet

- Handout 1 For Chapter 7 - Recognition and Valuation of Accounts ReceivablesDocument5 pagesHandout 1 For Chapter 7 - Recognition and Valuation of Accounts ReceivablesJamieNo ratings yet

- Kashato Shirts: General JournalDocument34 pagesKashato Shirts: General JournalJade Cruz100% (1)

- LCCI LEVEL 1&2 TextbookDocument100 pagesLCCI LEVEL 1&2 TextbookJohn Sue Han100% (2)

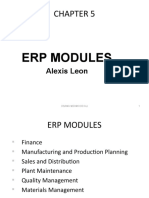

- Chapter 5 Osama Mehmood Ali1 Erp Modules Alexis LeonDocument44 pagesChapter 5 Osama Mehmood Ali1 Erp Modules Alexis LeonNikhil PrasannaNo ratings yet

- Homework Chapter 6Document3 pagesHomework Chapter 6Linh TranNo ratings yet

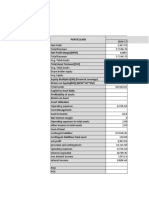

- Solution of Finanical Statement AnalysisDocument14 pagesSolution of Finanical Statement AnalysisMUHAMMAD AZAM100% (2)

- BFS Du Point Analysis BR6 Axis BankDocument27 pagesBFS Du Point Analysis BR6 Axis BankMadhusudhanan RameshkumarNo ratings yet

- Ais FlowchartDocument7 pagesAis FlowchartTangkua NasaNo ratings yet

- dc113 - 07052012 - 2 - WEBSITE UUMKLDocument1 pagedc113 - 07052012 - 2 - WEBSITE UUMKLEddie_Ka_6309No ratings yet

- Principles of Accounting (Grade-XI) : Welcome To You in Global College of ManagementDocument57 pagesPrinciples of Accounting (Grade-XI) : Welcome To You in Global College of ManagementNirajan Jaiswal KalwarNo ratings yet

- Ma As2Document6 pagesMa As2Omar AbidNo ratings yet

- Accounting CH 3Document49 pagesAccounting CH 3mad76857700No ratings yet

- Chapter 13: Foreign Currency Financial Statements: Advanced AccountingDocument42 pagesChapter 13: Foreign Currency Financial Statements: Advanced AccountingMad JayaNo ratings yet

- Terms of Business For Cranleys Chartered Accountants As at 01 Janaury 2010Document14 pagesTerms of Business For Cranleys Chartered Accountants As at 01 Janaury 2010Colin DavisonNo ratings yet

- Applications of Contemporary Management Accounting Techniques in Indian Industry: An Empirical Study - PHD (2006), by Liaqat Ali, Faculty ofDocument4 pagesApplications of Contemporary Management Accounting Techniques in Indian Industry: An Empirical Study - PHD (2006), by Liaqat Ali, Faculty ofananth6No ratings yet

- Oracle Projects Fundamentals - R12Document194 pagesOracle Projects Fundamentals - R12Shaik Mahamood100% (1)

- Acctg Conceptual FrameworkDocument11 pagesAcctg Conceptual FrameworkMaimona SemaNo ratings yet

- Z17520020220174021New PPT Ch1Document30 pagesZ17520020220174021New PPT Ch1Melissa Indah FiantyNo ratings yet

- Paper - 1: Principles and Practice of Accounting: Question No. 1 Is CompulsoryDocument25 pagesPaper - 1: Principles and Practice of Accounting: Question No. 1 Is CompulsorySaurabh JainNo ratings yet

- Finacc Quiz 2 PDF FreeDocument11 pagesFinacc Quiz 2 PDF FreeGuinevereNo ratings yet