You might also like

- Jim Rickards' IMPACT SystemDocument101 pagesJim Rickards' IMPACT SystemTushar KukretiNo ratings yet

- ACC 211 SIM Week 6 7Document40 pagesACC 211 SIM Week 6 7Threcia Rota50% (2)

- Schloss-10 11 06Document3 pagesSchloss-10 11 06Logic Gate CapitalNo ratings yet

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingFrom EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNo ratings yet

- Partnerships - Formation, Operations, and Changes in Ownership InterestsDocument79 pagesPartnerships - Formation, Operations, and Changes in Ownership Interestsrenna magdalenaNo ratings yet

- Dwnload Full Financial Management Core Concepts 4th Edition Brooks Solutions Manual PDFDocument35 pagesDwnload Full Financial Management Core Concepts 4th Edition Brooks Solutions Manual PDFbenboydr8pl100% (13)

- Capital Structure: Capital Structure Theories - Net Income Net Operating Income Modigliani-Miller Traditional ApproachDocument50 pagesCapital Structure: Capital Structure Theories - Net Income Net Operating Income Modigliani-Miller Traditional Approachthella deva prasadNo ratings yet

- BRV S+R Trading 210808Document50 pagesBRV S+R Trading 210808Simon Zhong100% (1)

- Project Report On SIP in Mutual FundsDocument76 pagesProject Report On SIP in Mutual FundsAnubhav Sood100% (6)

- BSM PG College Roorkee: Assignment OnDocument26 pagesBSM PG College Roorkee: Assignment OnNeeraj Singh RainaNo ratings yet

- Homework of Quantitative Courses Home Work No.: 3Document3 pagesHomework of Quantitative Courses Home Work No.: 3Jasjeet SinghNo ratings yet

- BSM PG College Roorkee: Assignment OnDocument24 pagesBSM PG College Roorkee: Assignment OnNeeraj Singh RainaNo ratings yet

- Chapter 4 Leverage Capital StructureDocument5 pagesChapter 4 Leverage Capital StructureshanksamNo ratings yet

- Financial Sourcing and Analysis: (Capital Structure)Document19 pagesFinancial Sourcing and Analysis: (Capital Structure)RITUKANT MAURYANo ratings yet

- Amalgamation TreatmentDocument283 pagesAmalgamation TreatmentMalkeet SinghNo ratings yet

- Capital Structure TheoriesDocument8 pagesCapital Structure TheoriesSirshajit SanfuiNo ratings yet

- Capital StructureDocument43 pagesCapital Structurebhavya kakumanuNo ratings yet

- Capital Structure: G.Vijaya Kumar Prof. NACDocument14 pagesCapital Structure: G.Vijaya Kumar Prof. NACkam pNo ratings yet

- Capital StructureDocument46 pagesCapital StructureShubh AgarwalNo ratings yet

- Capital Structure Last PartDocument10 pagesCapital Structure Last PartSserwadda Abdul RahmanNo ratings yet

- Unit 6 O Business Firm: Financial A YsisDocument18 pagesUnit 6 O Business Firm: Financial A YsisPooja PandeyNo ratings yet

- 07 Financial LeverageDocument28 pages07 Financial LeverageAbdullah matenNo ratings yet

- Share Holders Equity: BOOKS and Records of A CorporationDocument5 pagesShare Holders Equity: BOOKS and Records of A CorporationQueen ValleNo ratings yet

- Capital StructureDocument8 pagesCapital StructureVarun MudaliarNo ratings yet

- Capital Structure - 1Document25 pagesCapital Structure - 1bakhtiar2014No ratings yet

- MBA 711 Chapter 06 Leverage and Capital SturctureDocument42 pagesMBA 711 Chapter 06 Leverage and Capital SturctureDesalegn Baramo GENo ratings yet

- Chapter 16 Tcdn GốcDocument37 pagesChapter 16 Tcdn GốcN KhNo ratings yet

- 2203 Week 5 TemplateDocument39 pages2203 Week 5 TemplateHORTENSENo ratings yet

- Background Note 1 - Financial LeverageDocument12 pagesBackground Note 1 - Financial LeverageENS SunNo ratings yet

- UNIT - 3:financial Decision: Prepared &presented Associate Professor, Dept. of Commerce&BS, CUSBDocument71 pagesUNIT - 3:financial Decision: Prepared &presented Associate Professor, Dept. of Commerce&BS, CUSBswethaNo ratings yet

- Lecture-9 10 Capital-StructureDocument32 pagesLecture-9 10 Capital-StructuremaxNo ratings yet

- Capital Fixed & Working - New SyllabusDocument6 pagesCapital Fixed & Working - New SyllabusNaaz AliNo ratings yet

- Financial Leverage and Capital Structure Policy: Conducted by Ranjika Perera & Chanaka KarunasenaDocument53 pagesFinancial Leverage and Capital Structure Policy: Conducted by Ranjika Perera & Chanaka Karunasenacharitha007No ratings yet

- Accounting ReviewerDocument19 pagesAccounting ReviewerMa. Daisy MistulaNo ratings yet

- Partnership Liquidation: Steps Involved in LiquidationDocument13 pagesPartnership Liquidation: Steps Involved in LiquidationCharles TuazonNo ratings yet

- FM Sanyam Jain Cia 1.2Document7 pagesFM Sanyam Jain Cia 1.2ALLIED AGENCIESNo ratings yet

- Fin Corp CSDocument48 pagesFin Corp CSИрина МигусNo ratings yet

- Capital Structure Theories - PPTDocument68 pagesCapital Structure Theories - PPThardika jadavNo ratings yet

- Corporate FinanceDocument9 pagesCorporate FinancePrince HussainNo ratings yet

- CHAPTER 11 Without AnswerDocument3 pagesCHAPTER 11 Without Answerlenaka0% (1)

- Capital Structure - MAINDocument69 pagesCapital Structure - MAINSHASHANK TOMER 21211781No ratings yet

- Internal Reconstruction NotesDocument16 pagesInternal Reconstruction NotesAkash Mehta100% (1)

- Chapter 2: Statement of Financial Position Statement of Financial PositionDocument16 pagesChapter 2: Statement of Financial Position Statement of Financial PositionDaniella Mae ElipNo ratings yet

- Capital Structure Decisions: Assignment - 1Document18 pagesCapital Structure Decisions: Assignment - 1khan mandyaNo ratings yet

- Assignment Final Project Financial ManagementDocument7 pagesAssignment Final Project Financial ManagementSyed Muhammad JaaferNo ratings yet

- UM20MB551-Corporate Finance: DR C Sivashanmugam Sivashanmugam@pes - EduDocument45 pagesUM20MB551-Corporate Finance: DR C Sivashanmugam Sivashanmugam@pes - EduRU ShenoyNo ratings yet

- Company Acc B.com Sem Iv...Document8 pagesCompany Acc B.com Sem Iv...Sarah ShelbyNo ratings yet

- Capital StructureDocument6 pagesCapital StructureHarinder KaurNo ratings yet

- Chapter 2 - Part 4 - Shares & Loan CapitalDocument24 pagesChapter 2 - Part 4 - Shares & Loan Capital2022885126No ratings yet

- R22 Financial Statement Analysis IFT NotesDocument15 pagesR22 Financial Statement Analysis IFT NotesIndustrial Trainig EAGNo ratings yet

- M&a Basic Internal Reconstruction QDocument7 pagesM&a Basic Internal Reconstruction Qayushi aggarwalNo ratings yet

- IntroductionDocument8 pagesIntroductionGustavo Alexandre GustavoNo ratings yet

- Balance Sheet: Manac I Session 2Document32 pagesBalance Sheet: Manac I Session 2Dhana Sekar SrinivasanNo ratings yet

- Capital StructureDocument31 pagesCapital StructureBagusSuciptoNo ratings yet

- C8 Statement of Financial PositionDocument14 pagesC8 Statement of Financial PositionAllaine ElfaNo ratings yet

- LM06 Cost of Capital-Foundational TopicsDocument12 pagesLM06 Cost of Capital-Foundational TopicsSYED HAIDER ABBAS KAZMINo ratings yet

- Solution Manual For Essentials of Investments 9th Edition by BodieDocument36 pagesSolution Manual For Essentials of Investments 9th Edition by Bodiepasserby.bedouinmm42i100% (46)

- Accounting 2 Statement of Financial Position Balance SheetDocument5 pagesAccounting 2 Statement of Financial Position Balance SheetNoah HNo ratings yet

- Dayalbagh Educational Institute Faculty of Commerce Abm 801: Financial Management & Analysis Question BankDocument9 pagesDayalbagh Educational Institute Faculty of Commerce Abm 801: Financial Management & Analysis Question BankneetamoniNo ratings yet

- Group Three (3) : Capital StructureDocument22 pagesGroup Three (3) : Capital StructurenagumsiNo ratings yet

- Capital StructureDocument9 pagesCapital StructureShrinivasan IyengarNo ratings yet

- Business Studies Class 12 Study Material Chapter 9Document17 pagesBusiness Studies Class 12 Study Material Chapter 9YashNo ratings yet

- 01.dividend ModuleDocument35 pages01.dividend ModuleVaidyanathan Ravichandran100% (2)

- The Passive and Active Stances: Bond Portfolio ManagementDocument41 pagesThe Passive and Active Stances: Bond Portfolio ManagementvaibhavNo ratings yet

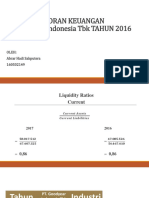

- Analisis Laporan Keuangan PT. Goodyear Indonesia TBK TAHUN 2016 DAN 2017Document34 pagesAnalisis Laporan Keuangan PT. Goodyear Indonesia TBK TAHUN 2016 DAN 2017Tri AmbarNo ratings yet

- Aubank 26042022164457 Ausfb Outcome BMDocument23 pagesAubank 26042022164457 Ausfb Outcome BMrkumar_81No ratings yet

- Investment Analysis and Portfolio ManagementDocument5 pagesInvestment Analysis and Portfolio ManagementMuhammad QasimNo ratings yet

- TK BAI2Document23 pagesTK BAI2saurabh_565No ratings yet

- Mba50 Wa4 Key 202223Document7 pagesMba50 Wa4 Key 202223serepasfNo ratings yet

- SimexDocument3 pagesSimexRoland Ron BantilanNo ratings yet

- Stock Exchange: by Huda A.S. QureshiDocument27 pagesStock Exchange: by Huda A.S. Qureshistd_10225No ratings yet

- ICB Mutual FundDocument10 pagesICB Mutual FundDipock MondalNo ratings yet

- Mutual FundDocument9 pagesMutual Fund05550No ratings yet

- Portfolio Management Portfolio Management Portfolio ManagementDocument4 pagesPortfolio Management Portfolio Management Portfolio ManagementAbhishek MishraNo ratings yet

- Financial Statement Analysis UpdatedDocument8 pagesFinancial Statement Analysis UpdatedEmmanuel PenullarNo ratings yet

- Merchant BankingDocument21 pagesMerchant BankinghksanthoshNo ratings yet

- The Balance of Payments, Exchange Rates, and Trade Deficits: Mcgraw-Hill/IrwinDocument15 pagesThe Balance of Payments, Exchange Rates, and Trade Deficits: Mcgraw-Hill/IrwinMonjur MorshedNo ratings yet

- Golden Line English VisionDocument32 pagesGolden Line English VisionZaim AkoNo ratings yet

- 2000 5000 Company Update 20220224Document54 pages2000 5000 Company Update 20220224Contra Value BetsNo ratings yet

- GIS - Non Stock v.2013 081413Document6 pagesGIS - Non Stock v.2013 081413nelida.tondoNo ratings yet

- Eastern Bank LTD: Effective Date: Exchange RateDocument2 pagesEastern Bank LTD: Effective Date: Exchange RateMAHMUDUR RAHMANNo ratings yet

- Course Planner: GC University FaisalabadDocument3 pagesCourse Planner: GC University Faisalabadgoharmahmood203No ratings yet

- Off Balance SheetDocument15 pagesOff Balance SheetHussain khawajaNo ratings yet

- Edelweiss Financial ServicesDocument68 pagesEdelweiss Financial Servicessarmistha sahooNo ratings yet

- 20220910170939HCTAN008C6b Topic6b Risk - MGTDocument57 pages20220910170939HCTAN008C6b Topic6b Risk - MGTnicholas wijayaNo ratings yet

- Gamma Scalping 101 Gamma Theta TradingDocument13 pagesGamma Scalping 101 Gamma Theta Tradingcecatoh228No ratings yet

- Materi Sekuritas Delutif LPSDocument52 pagesMateri Sekuritas Delutif LPSyn sagalaNo ratings yet

- Fixed Income Assignment 1Document3 pagesFixed Income Assignment 1Rattan Preet SinghNo ratings yet