You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Business Takeover AgreementDocument4 pagesBusiness Takeover AgreementAlankar NarulaNo ratings yet

- Douglas Walton Relevance in Argumentation 2003 PDFDocument328 pagesDouglas Walton Relevance in Argumentation 2003 PDFIon Banari100% (9)

- By The People: A History of The United StatesDocument36 pagesBy The People: A History of The United StatesAlan DukeNo ratings yet

- Kansya Thali Machine Foot MassageDocument2 pagesKansya Thali Machine Foot MassageNishikant Rayanade100% (3)

- Cost Accountancy - BBA Part II Semester IIIDocument69 pagesCost Accountancy - BBA Part II Semester IIINishikant Rayanade100% (1)

- Cost Accountancy: Bba - Ii Semester - IiiDocument19 pagesCost Accountancy: Bba - Ii Semester - IiiNishikant RayanadeNo ratings yet

- BBA II SEM III Cost Accountancy PPT 1Document22 pagesBBA II SEM III Cost Accountancy PPT 1Nishikant RayanadeNo ratings yet

- Fund Flow Statement: Dr. Varsha RayanadeDocument18 pagesFund Flow Statement: Dr. Varsha RayanadeNishikant RayanadeNo ratings yet

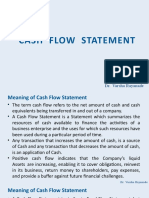

- Cash Flow Statement: Dr. Varsha RayanadeDocument8 pagesCash Flow Statement: Dr. Varsha RayanadeNishikant RayanadeNo ratings yet

- Tr45 Oaths and SwearingDocument8 pagesTr45 Oaths and SwearingWendell RicardoNo ratings yet

- Curriculum Leadership Strategies For Development and Implementation 4th Edition Glatthorn Test BankDocument25 pagesCurriculum Leadership Strategies For Development and Implementation 4th Edition Glatthorn Test BankMrRogerAndersonMDdbkj100% (58)

- Missed Zakat: Your Guide To Understanding and CalculatingDocument20 pagesMissed Zakat: Your Guide To Understanding and CalculatingHnia UsmanNo ratings yet

- Financial Literacy 101 PDFDocument24 pagesFinancial Literacy 101 PDFDenver John Melecio TurtogaNo ratings yet

- Jack Keystone Cat 6 Belden AX104193 PDFDocument3 pagesJack Keystone Cat 6 Belden AX104193 PDFBethsy WinNo ratings yet

- University of Cambridge International Examinations General Certificate of Education Advanced Subsidiary Level and Advanced LevelDocument2 pagesUniversity of Cambridge International Examinations General Certificate of Education Advanced Subsidiary Level and Advanced LevelAsad SyedNo ratings yet

- United States Court of ClaimsDocument22 pagesUnited States Court of ClaimsScribd Government DocsNo ratings yet

- Damages FlowchartDocument1 pageDamages FlowchartRon HusmilloNo ratings yet

- Settlement of International DisputesDocument8 pagesSettlement of International DisputesLata SinghNo ratings yet

- Islamic Personal Law-Ii Gift or Hiba: Ghulam Mujtaba MalikDocument9 pagesIslamic Personal Law-Ii Gift or Hiba: Ghulam Mujtaba MalikJarar AleeNo ratings yet

- Lecture 2 - Terminal Settling VelocityDocument8 pagesLecture 2 - Terminal Settling VelocityMuhammad NaeemNo ratings yet

- Comprehensive Dangerous Drugs Act of 2002 Written ReportDocument35 pagesComprehensive Dangerous Drugs Act of 2002 Written ReportRabelais Medina100% (1)

- T7-R18-P2-Principles-v9.1 - Study NotesDocument12 pagesT7-R18-P2-Principles-v9.1 - Study NotesRanjeev LabhNo ratings yet

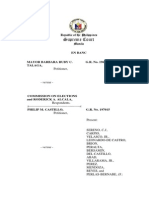

- Talaga v. ComelecDocument26 pagesTalaga v. ComelecKay Ann J GempisNo ratings yet

- Simplifying It Security For DummiesDocument76 pagesSimplifying It Security For DummiesAnonymous 1eZNBWqpB100% (2)

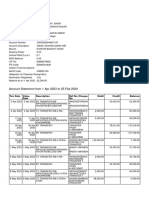

- Account Usage and Recharge Statement From 01-Jul-2021 To 13-Jul-2021Document11 pagesAccount Usage and Recharge Statement From 01-Jul-2021 To 13-Jul-2021Shaista JanNo ratings yet

- K44 ZLR4 JX 0 WVW9 VPDocument4 pagesK44 ZLR4 JX 0 WVW9 VPMaalvika SinghNo ratings yet

- Aston Adam Mbaya 13 The Chambers of The Condemned of Covenants Subconscious Covenants With The DevilDocument4 pagesAston Adam Mbaya 13 The Chambers of The Condemned of Covenants Subconscious Covenants With The DevilChong JoshuaNo ratings yet

- Nat - Res & Environmental Law - Finals ReviewerDocument8 pagesNat - Res & Environmental Law - Finals ReviewerJotham FunclaraNo ratings yet

- Export Management: Difficulties in Export Trade - Fishing in Turbulent WatersDocument2 pagesExport Management: Difficulties in Export Trade - Fishing in Turbulent WatersVIJAYADARSHINI VIDJEANNo ratings yet

- RTE Children With Disabilities PDFDocument3 pagesRTE Children With Disabilities PDFDisability Rights AllianceNo ratings yet

- Massachusetts Institute of Technology: 8.223, Classical Mechanics II Exercises 1Document4 pagesMassachusetts Institute of Technology: 8.223, Classical Mechanics II Exercises 1Uriel MorenoNo ratings yet

- Famous Men of The Middle Ages by Haaren, John H. (John Henry), 1855-1916Document101 pagesFamous Men of The Middle Ages by Haaren, John H. (John Henry), 1855-1916Gutenberg.org100% (1)

- Ecrl FS01 - Tunjung - Ugc - Schedule HDocument14 pagesEcrl FS01 - Tunjung - Ugc - Schedule Hlkt_pestechNo ratings yet

- Master Circular On Exposure NormsDocument30 pagesMaster Circular On Exposure NormssohamNo ratings yet

- Stakeholders 2Document25 pagesStakeholders 2Sebastián Posada100% (1)

- Birth Certificates For Children With Gay Parents. Paula Gerber and Phoebe Irving LindnerDocument53 pagesBirth Certificates For Children With Gay Parents. Paula Gerber and Phoebe Irving LindnerMiguel T. QuirogaNo ratings yet