You might also like

- Role of RBI in Control of Credit - Economics Project Class 12 (2019-20)Document22 pagesRole of RBI in Control of Credit - Economics Project Class 12 (2019-20)Anonymous JbDKaC78% (134)

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- SHARVILDocument19 pagesSHARVILSharvil ChoudharyNo ratings yet

- RBI's Role as Lender of Last ResortDocument20 pagesRBI's Role as Lender of Last ResortGarima AgrawalNo ratings yet

- Export & ImportDocument17 pagesExport & ImportIhsan Ullah Himmat B-124No ratings yet

- Banking LawsDocument18 pagesBanking Lawsmilindm.workNo ratings yet

- Banking LawsDocument18 pagesBanking Lawsmilindm.workNo ratings yet

- Economics Final Pro. 2sem-2Document14 pagesEconomics Final Pro. 2sem-2Thakur Manu PratapNo ratings yet

- Economics ProjectDocument28 pagesEconomics ProjectSanstubh SonkarNo ratings yet

- RBI Lender of Last ResortDocument18 pagesRBI Lender of Last ResortHemantVermaNo ratings yet

- National Law University, OdishaDocument16 pagesNational Law University, OdishaTanmayNo ratings yet

- Reserve Bank of India Act 1934 and RBIDocument8 pagesReserve Bank of India Act 1934 and RBIαиgєl ѕєlєиαNo ratings yet

- Acfrogazzjejoc1moktw9rsas6fatyjvhtnbv3ad5faapd28rnkhgf Hfwmg4bcq Nsrwme8d H3v1it5h2txfkji0vyc4gkzfpj 5l87a1sbznawivaah2mkybogemycicm2k1pzoqgcnsycvfwDocument17 pagesAcfrogazzjejoc1moktw9rsas6fatyjvhtnbv3ad5faapd28rnkhgf Hfwmg4bcq Nsrwme8d H3v1it5h2txfkji0vyc4gkzfpj 5l87a1sbznawivaah2mkybogemycicm2k1pzoqgcnsycvfwdilipkumar.1267No ratings yet

- RESERVE BANK OF INDIA (Shivam)Document6 pagesRESERVE BANK OF INDIA (Shivam)nishantarya283No ratings yet

- Economics Project - Sem 4Document20 pagesEconomics Project - Sem 4rudrakshi raiNo ratings yet

- Reserve Bank of India: An Analysis of Banking Vis A Vis GlobalizationDocument11 pagesReserve Bank of India: An Analysis of Banking Vis A Vis Globalizationarko banerjeeNo ratings yet

- Roles & Functions of RBIDocument24 pagesRoles & Functions of RBIAvanishNo ratings yet

- PDF of RBIs STRUCTURE MANAGEMEN PDFDocument12 pagesPDF of RBIs STRUCTURE MANAGEMEN PDFalizaNo ratings yet

- Working of RBI: Supervised By: DR - Anjana AttriDocument25 pagesWorking of RBI: Supervised By: DR - Anjana AttriKajal ChaudharyNo ratings yet

- RBI PROJECTDocument11 pagesRBI PROJECTShalini SonkarNo ratings yet

- Structure and Functions of Rbi: Download Ebook NowDocument6 pagesStructure and Functions of Rbi: Download Ebook NowDipanshu SinhaNo ratings yet

- Role of Indian banks and financial institutionsDocument22 pagesRole of Indian banks and financial institutionsAshish SinghNo ratings yet

- Banking ProjectDocument14 pagesBanking ProjectSnehashreeHotaNo ratings yet

- RBI FunctionsDocument2 pagesRBI Functionssakshi singhNo ratings yet

- Rbi and Its Monetary PolicyDocument5 pagesRbi and Its Monetary PolicyPravin NisharNo ratings yet

- Pbi PresentationDocument25 pagesPbi Presentationanuragmahakhud03No ratings yet

- RBI's Role in Regulating BankingDocument13 pagesRBI's Role in Regulating BankingAmbreen ShamsiNo ratings yet

- JETIR1903C18Document15 pagesJETIR1903C18endlessnobi181229No ratings yet

- Bfi RbiDocument32 pagesBfi RbiLalit ShahNo ratings yet

- RBIDocument22 pagesRBIआकाश स्व.No ratings yet

- National Law Institute University Bhopal, M.P.: A Project of Banking Law On The TopicDocument14 pagesNational Law Institute University Bhopal, M.P.: A Project of Banking Law On The TopicAjita NadkarniNo ratings yet

- Project of Banking Law: Central University of South BiharDocument12 pagesProject of Banking Law: Central University of South BiharAnjali SinhaNo ratings yet

- CHAPTER 3 RBI and Monetary PolicyDocument27 pagesCHAPTER 3 RBI and Monetary PolicyPraveen KumarNo ratings yet

- IBFS WRITE UPDocument13 pagesIBFS WRITE UPmeparamtoshNo ratings yet

- Reserve Bank of IndiaDocument16 pagesReserve Bank of IndiaAlpa GhoshNo ratings yet

- Reserve Bank of India Act, 1934: EstablishmentDocument4 pagesReserve Bank of India Act, 1934: Establishmentagrawalvaibhav729No ratings yet

- 1st Sem Economics ProjectDocument11 pages1st Sem Economics ProjectDevendra DhruwNo ratings yet

- Reserve Bank of India: HistoryDocument4 pagesReserve Bank of India: HistoryEku Nahoi HoilepeNo ratings yet

- RBI and SEBI - A Brief History of India's Central Banking and Securities Market RegulatorsDocument7 pagesRBI and SEBI - A Brief History of India's Central Banking and Securities Market Regulatorsprv3No ratings yet

- RBI (Basic Info.)Document4 pagesRBI (Basic Info.)Gowher MajidNo ratings yet

- RBI's Role in Regulating India's Banking & Financial SystemDocument20 pagesRBI's Role in Regulating India's Banking & Financial SystemSophiya KhanamNo ratings yet

- RESERVE BANK OF INDIA Its Origin, Structure and Function - ReportDocument11 pagesRESERVE BANK OF INDIA Its Origin, Structure and Function - ReportAnirban DebNo ratings yet

- RBI's Main Activities to Sustain Economic GrowthDocument9 pagesRBI's Main Activities to Sustain Economic GrowthPrateek GuptaNo ratings yet

- The Complete Guide About Reserve Bank of India (RBI)Document19 pagesThe Complete Guide About Reserve Bank of India (RBI)Rakesh Kumar LenkaNo ratings yet

- CONCLUSIONDocument12 pagesCONCLUSIONAniket ShigwanNo ratings yet

- Good MorningDocument24 pagesGood MorningManoj KumarNo ratings yet

- Financial Market and Commercial Banking Code: RMB FM 03: UNIT-2Document118 pagesFinancial Market and Commercial Banking Code: RMB FM 03: UNIT-2Ankur SharmaNo ratings yet

- Rbi Structure and Function Subsidiaries of Rbi Final 83Document4 pagesRbi Structure and Function Subsidiaries of Rbi Final 83sonam1991No ratings yet

- Reserve Bank of IndiaDocument21 pagesReserve Bank of IndiaAcchu BajajNo ratings yet

- PROF. S. K. Datta Buddh Pratap RathoreDocument15 pagesPROF. S. K. Datta Buddh Pratap RathoreBuddhapratap RathoreNo ratings yet

- Indian Banking SystemDocument57 pagesIndian Banking Systemsamadhandamdhar6109100% (1)

- P TybbiDocument50 pagesP TybbiPriyanka YadavNo ratings yet

- Madhusmita Kananika Pradhan Assgn - 1Document21 pagesMadhusmita Kananika Pradhan Assgn - 1smartvicky4uNo ratings yet

- History and Functions of the Reserve Bank of IndiaDocument5 pagesHistory and Functions of the Reserve Bank of IndiaJay Ram100% (1)

- RbiDocument21 pagesRbixx69dd69xxNo ratings yet

- Agricultural Finance and Project Management: Reserve Bank of IndiaDocument41 pagesAgricultural Finance and Project Management: Reserve Bank of IndiaPràßhánTh Aɭoŋɘ ɭovɘʀNo ratings yet

- Rbi PDFDocument4 pagesRbi PDFUmar AbdullahNo ratings yet

- Role of RBI Under Banking Regulation Act, 1949Document11 pagesRole of RBI Under Banking Regulation Act, 1949Jay Ram100% (1)

- Banking India: Accepting Deposits for the Purpose of LendingFrom EverandBanking India: Accepting Deposits for the Purpose of LendingNo ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Rights and Responsibilities of Finders of Lost GoodsDocument12 pagesRights and Responsibilities of Finders of Lost GoodsDevendra DhruwNo ratings yet

- Preventive Detention and Individual Liberty in IndiaDocument14 pagesPreventive Detention and Individual Liberty in IndiaDevendra DhruwNo ratings yet

- Assessment of Undisclosed Income ActDocument18 pagesAssessment of Undisclosed Income ActDevendra DhruwNo ratings yet

- 11 - Chapter 6Document61 pages11 - Chapter 6Devendra DhruwNo ratings yet

- IpcDocument16 pagesIpcDevendra DhruwNo ratings yet

- Bolar Exemption For Infringement of Patent: Hidayatullah National Law University Uparwara, New Raipur (C.G.)Document22 pagesBolar Exemption For Infringement of Patent: Hidayatullah National Law University Uparwara, New Raipur (C.G.)Devendra DhruwNo ratings yet

- Sem5.international Relations - Sumit.157Document19 pagesSem5.international Relations - Sumit.157Devendra DhruwNo ratings yet

- UN's Role in Maintaining Global PeaceDocument35 pagesUN's Role in Maintaining Global PeaceDevendra DhruwNo ratings yet

- Sumit - IRDocument34 pagesSumit - IRDevendra DhruwNo ratings yet

- A Project On: "Sale and Agreement To Sell"Document14 pagesA Project On: "Sale and Agreement To Sell"Devendra DhruwNo ratings yet

- Cultural Growth in Toffler's PerspectiveDocument17 pagesCultural Growth in Toffler's PerspectiveDevendra DhruwNo ratings yet

- Cultural Growth in Toffler's PerspectiveDocument17 pagesCultural Growth in Toffler's PerspectiveDevendra DhruwNo ratings yet

- HC32 2021 Intermediate Macro I 1Document3 pagesHC32 2021 Intermediate Macro I 1I ain't grootNo ratings yet

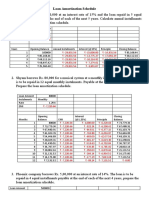

- Solution Time Value of Money 5 Loan Amortization Schedule and PV of Perpetual Annuity and PV Growing Annuity 3PVyvICyHiDocument5 pagesSolution Time Value of Money 5 Loan Amortization Schedule and PV of Perpetual Annuity and PV Growing Annuity 3PVyvICyHiShareshth JainNo ratings yet

- Chap021newDocument36 pagesChap021newNguyễn Cẩm HươngNo ratings yet

- Work: Waterproofing Works For The Proposed 'Residential & Commercial Complex at Mohili, Sakinaka Mumbai 400 072' ContractorDocument11 pagesWork: Waterproofing Works For The Proposed 'Residential & Commercial Complex at Mohili, Sakinaka Mumbai 400 072' ContractorShubham DubeyNo ratings yet

- The Application of Machine Learning and Deep LearnDocument20 pagesThe Application of Machine Learning and Deep LearnFran MoralesNo ratings yet

- Standardizing Innovation Management: An Opportunity For Smes in The Aerospace IndustryDocument43 pagesStandardizing Innovation Management: An Opportunity For Smes in The Aerospace IndustryDr. Ammar YakanNo ratings yet

- Reading 70 Code of Ethics and Standards of Professional ConductDocument16 pagesReading 70 Code of Ethics and Standards of Professional ConductNeerajNo ratings yet

- Social Support For Expatriates Through Virtual Platforms: Exploring The Role of Online and Offline ParticipationDocument33 pagesSocial Support For Expatriates Through Virtual Platforms: Exploring The Role of Online and Offline ParticipationAniss AitallaNo ratings yet

- Journal Homepage: - : IntroductionDocument9 pagesJournal Homepage: - : IntroductionNikhita KrishnaiahNo ratings yet

- Swot of AbinbevDocument3 pagesSwot of AbinbevSanjeev Kumar SharmaNo ratings yet

- ABBA - Annual Report 2019Document232 pagesABBA - Annual Report 2019Bambang HarsonoNo ratings yet

- Intermodal Transportation System in An Evolving Economy: Research PaperDocument7 pagesIntermodal Transportation System in An Evolving Economy: Research PaperUsiwo FranklinNo ratings yet

- Presentation on Puma Brand Life CycleDocument24 pagesPresentation on Puma Brand Life Cyclenicks1988No ratings yet

- OCD-LGU MOA for Isolation Facility ConstructionDocument8 pagesOCD-LGU MOA for Isolation Facility ConstructionORLANDO GIL FAJICULAY FAJARILLO Jr.No ratings yet

- Department of Labor checklist for construction safety evaluationDocument1 pageDepartment of Labor checklist for construction safety evaluationKevin BasaNo ratings yet

- Company Profile - Tri-Wall IndiaDocument35 pagesCompany Profile - Tri-Wall IndiaPrateek Singh SengarNo ratings yet

- PLDT Inc - 17a 2019Document381 pagesPLDT Inc - 17a 2019Kylie Luigi Leynes BagonNo ratings yet

- The Platinum Card®: Page 1 of 4Document4 pagesThe Platinum Card®: Page 1 of 4Emma ChanNo ratings yet

- EssentialismDocument1 pageEssentialismMehrdad FereydoniNo ratings yet

- Do a SWOT analysis for business ideasDocument4 pagesDo a SWOT analysis for business ideasOliver SyNo ratings yet

- Group Assignment - A211 QUESTIONNAIREDocument9 pagesGroup Assignment - A211 QUESTIONNAIREMuhammad NafisNo ratings yet

- Milk Tea Industry: An Exploratory Study: February 2020Document9 pagesMilk Tea Industry: An Exploratory Study: February 2020NING ANGELNo ratings yet

- Shrimp Farming in Pakistan Urdu GuideDocument17 pagesShrimp Farming in Pakistan Urdu GuidesohailauhNo ratings yet

- CIR v. PDI (Waiver)Document30 pagesCIR v. PDI (Waiver)Jerwin DaveNo ratings yet

- Trends in Ethics in Computing Assignment # 05 Sap Ids of Group MembersDocument2 pagesTrends in Ethics in Computing Assignment # 05 Sap Ids of Group Memberswardah mukhtarNo ratings yet

- The One Percent Podcast With Vishal Khandelwal Ep. 1 Manish Chokhani TranscriptDocument25 pagesThe One Percent Podcast With Vishal Khandelwal Ep. 1 Manish Chokhani TranscriptCinelsoyNo ratings yet

- Income Tax Agadan PrapatraDocument3 pagesIncome Tax Agadan Prapatraat.amitkumarbstNo ratings yet

- Indian Film Manufacturers Adding Capacities To Meet Growing Demand For Bopp and BopetDocument8 pagesIndian Film Manufacturers Adding Capacities To Meet Growing Demand For Bopp and BopetSanjay Kumar ShahiNo ratings yet

- Neoclassical Economics: Economic Science, To DistinguishDocument35 pagesNeoclassical Economics: Economic Science, To DistinguishWan Sek ChoonNo ratings yet

- Marketing Plan Final ReMarketing Plan of ACME Agrovet Beverage LTD PortDocument84 pagesMarketing Plan Final ReMarketing Plan of ACME Agrovet Beverage LTD PortNafiz FahimNo ratings yet