You might also like

- YeahDocument41 pagesYeahBenjamin ShortNo ratings yet

- IKO968959021 Auth LetterDocument3 pagesIKO968959021 Auth LetterGero0412No ratings yet

- Implied Volatility Spreadsheet (Zero Dividend Model) : Data InputsDocument3 pagesImplied Volatility Spreadsheet (Zero Dividend Model) : Data InputsFerreiraNo ratings yet

- Reason Codes: ImportantDocument5 pagesReason Codes: ImportantNabila PramestiNo ratings yet

- FunctionDocument66 pagesFunctionapi-616455436No ratings yet

- TOP-50 MOST IMPORTANT SQL QUERIES - How To Use SQL To Work With Data in A Relational Database Today. (SQL Skills Book 1)Document30 pagesTOP-50 MOST IMPORTANT SQL QUERIES - How To Use SQL To Work With Data in A Relational Database Today. (SQL Skills Book 1)Melvin MarchenaNo ratings yet

- World IP Address Ranges. Total: 619,079 Ip Ranges. Date: January 2016Document55 pagesWorld IP Address Ranges. Total: 619,079 Ip Ranges. Date: January 2016robi docoNo ratings yet

- Oracle Virtual Box FromDocument81 pagesOracle Virtual Box FromDHIVYA SNo ratings yet

- CVVDocument6 pagesCVVappuamreddyNo ratings yet

- Gufran.S@Agile-mgt - Com H G Namitha - Manager InfoQuestDocument5 pagesGufran.S@Agile-mgt - Com H G Namitha - Manager InfoQuestmanojjshahNo ratings yet

- Click Here Click HereDocument3 pagesClick Here Click HereRathinavel Dass100% (1)

- Script GreenvilleDocument14 pagesScript Greenvillemangaanimee4685No ratings yet

- Zong Corporate Bulk Sms APIDocument11 pagesZong Corporate Bulk Sms APITas Pro50% (2)

- Ckyc & Kra Kyc FormDocument27 pagesCkyc & Kra Kyc FormPerumal SNo ratings yet

- Scaling: Business Research MethodsDocument23 pagesScaling: Business Research MethodsSatyajit GhoshNo ratings yet

- 5 Camrolla TradingDocument5 pages5 Camrolla TradingViswanath PalyamNo ratings yet

- View Full Version:: ZTE MF626 Unlock FreeDocument11 pagesView Full Version:: ZTE MF626 Unlock Freemendes.davidNo ratings yet

- Simply Bank - Checking AccountDocument2 pagesSimply Bank - Checking Accountmcginnis wayneNo ratings yet

- Custom capital strategies from 5L-50LDocument6 pagesCustom capital strategies from 5L-50LAlgo TraderNo ratings yet

- Imagine A Reward: Every Time You RedeemDocument1 pageImagine A Reward: Every Time You RedeemD SathwikNo ratings yet

- Annual financial statement analysis of assets, equity and liabilities from 2019-2021Document4 pagesAnnual financial statement analysis of assets, equity and liabilities from 2019-2021Muhammad AkmalNo ratings yet

- InvertedDocument3 pagesInvertedShrikant KeskarNo ratings yet

- Card No: 462490XXXXXX7541 Sanctioned Credit LimitDocument3 pagesCard No: 462490XXXXXX7541 Sanctioned Credit Limitstar work YJNo ratings yet

- Edfora - Order - FormDocument4 pagesEdfora - Order - FormSwetha MaguluriNo ratings yet

- Dumps Latest (8 Files Merged)Document121 pagesDumps Latest (8 Files Merged)nÄzeer ViratianNo ratings yet

- IMDA DCA Form PDFDocument1 pageIMDA DCA Form PDFDaps PounchNo ratings yet

- SM-A037 UM LTN SS Eng Rev.1.0 220720Document112 pagesSM-A037 UM LTN SS Eng Rev.1.0 220720José LuizNo ratings yet

- Airtel Bill AprilDocument3 pagesAirtel Bill AprilHiten ChudasamaNo ratings yet

- Patternz Screener-RT 1 WEEK MY OPTIONDocument2 pagesPatternz Screener-RT 1 WEEK MY OPTIONbhargavaNo ratings yet

- Future and Options in Forex TradingDocument9 pagesFuture and Options in Forex TradingBearStreetNo ratings yet

- Open Trading Account FormDocument38 pagesOpen Trading Account FormManjunath GaddiNo ratings yet

- LF 9 RSer Co PYu SLagDocument4 pagesLF 9 RSer Co PYu SLagsarvani PNo ratings yet

- Gmail - (Payment Receipt) Booking Checked-Out - OYO 2756 Hotel Virasat - Booking No. - DVEM5189Document1 pageGmail - (Payment Receipt) Booking Checked-Out - OYO 2756 Hotel Virasat - Booking No. - DVEM5189varunkumar415100% (1)

- Commodities Account Opening Form: Document Significance PAGE(s)Document47 pagesCommodities Account Opening Form: Document Significance PAGE(s)sreehari dineshNo ratings yet

- Minor Attaining Majority Form EditableDocument5 pagesMinor Attaining Majority Form EditableDivNo ratings yet

- April 2019Document72 pagesApril 2019Sunil UndarNo ratings yet

- x9203 SK Scrapped by @AsmSafoneDocument158 pagesx9203 SK Scrapped by @AsmSafonearakplaygamesNo ratings yet

- Gmon WlanDocument140 pagesGmon Wlanroy croffNo ratings yet

- DSL Bill 01195484010 DSL 751019805Document5 pagesDSL Bill 01195484010 DSL 751019805Ranjan KhandelwalNo ratings yet

- AppValley MobileconfigDocument52 pagesAppValley MobileconfigJosé Matías González AlzateNo ratings yet

- 2023 NAIDC FINAL HotelsDocument6 pages2023 NAIDC FINAL HotelsJennifer KoenemundNo ratings yet

- Monthly Bank Statement SummaryDocument2 pagesMonthly Bank Statement Summarykunjal mistryNo ratings yet

- Free Web Hosting With PHP and MySQL - InfinityFreeDocument1 pageFree Web Hosting With PHP and MySQL - InfinityFreeAhmet Selim YakutNo ratings yet

- Master Stroke Booklet 2023-24Document368 pagesMaster Stroke Booklet 2023-24muzeebur rahmanNo ratings yet

- Voucher NH2003069007378Document3 pagesVoucher NH2003069007378Thalapathy VenkatNo ratings yet

- 2C2P-Airline Payment v1 5 6Document43 pages2C2P-Airline Payment v1 5 6wmarasigan2610No ratings yet

- Portfolio overview and performance trackerDocument6 pagesPortfolio overview and performance trackerAsifayiroorNo ratings yet

- Technidex: Stock Futures IndexDocument3 pagesTechnidex: Stock Futures IndexRaya DuraiNo ratings yet

- Electronic Reservation Slip IRCTC E-Ticketing Service (Agent)Document3 pagesElectronic Reservation Slip IRCTC E-Ticketing Service (Agent)Shahbaz ahmadNo ratings yet

- Clover - PreApplication NEWDocument1 pageClover - PreApplication NEWgreat augustNo ratings yet

- Invoice IataDocument1 pageInvoice IataCuma NiatNo ratings yet

- Document 150683822Document2 pagesDocument 150683822Shawn LyonsNo ratings yet

- 12k Yahoo Login2023Document170 pages12k Yahoo Login2023Michael miguel Torres morelNo ratings yet

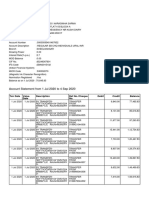

- Cell D2 Cell D1: Maximum Point Is The Maximum "Closing" ValueDocument106 pagesCell D2 Cell D1: Maximum Point Is The Maximum "Closing" ValuersdprasadNo ratings yet

- Top Technical Indicators for TV ChartsDocument2 pagesTop Technical Indicators for TV Chartsabsar ahmedNo ratings yet

- Document 2Document5 pagesDocument 2rosaNo ratings yet

- IRCTC E-Ticketing ServiceDocument3 pagesIRCTC E-Ticketing ServiceMr. Saurabh SinghNo ratings yet

- RSI - VWAP - strategy 只做多 牛市最牛逼策略Document6 pagesRSI - VWAP - strategy 只做多 牛市最牛逼策略高鴻No ratings yet

- Internet Banking and Mobile Banking Through Ussd PosterDocument1 pageInternet Banking and Mobile Banking Through Ussd PosterCash monkeyNo ratings yet

- 6 F 193483165 D 13 F 6255 ADocument15 pages6 F 193483165 D 13 F 6255 Aapi-616455436No ratings yet

- Coding HWDocument87 pagesCoding HWapi-616455436No ratings yet

- Homework 110071607 林郁揚: %Bsprice.MDocument31 pagesHomework 110071607 林郁揚: %Bsprice.Mapi-616455436No ratings yet

- 6 F 193483165 D 13 F 6255 ADocument15 pages6 F 193483165 D 13 F 6255 Aapi-616455436No ratings yet

- F 57 C 3268293 Ee 1 e 74 B 49Document83 pagesF 57 C 3268293 Ee 1 e 74 B 49api-616455436No ratings yet