You might also like

- The Certified Six Sigma: Govind RamuDocument4 pagesThe Certified Six Sigma: Govind Ramuoxovxkuptrxdomumsy29% (7)

- Adult Webcam Studio 101 - A Money Making Guide For E-Pimps (PDFDrive)Document756 pagesAdult Webcam Studio 101 - A Money Making Guide For E-Pimps (PDFDrive)Kristin Monavik60% (5)

- SDM Case Analysis: ABB and Caterpillar (A) : Key Account ManagementDocument5 pagesSDM Case Analysis: ABB and Caterpillar (A) : Key Account Managementmahtaabk100% (1)

- Tax ReviewerDocument62 pagesTax ReviewerFelixberto Jr. BaisNo ratings yet

- 9001-2008 To 9001-2015 To IATF 16949 - Rev1 - 02-17-17Document8 pages9001-2008 To 9001-2015 To IATF 16949 - Rev1 - 02-17-17normalNo ratings yet

- Statement 04oct2019Document4 pagesStatement 04oct2019Viorel OpreaNo ratings yet

- CDR.06 The New Modeled, Subtractive, Multiple Base MIP 3.9 Forensic Schedule Analysis ProtocolDocument23 pagesCDR.06 The New Modeled, Subtractive, Multiple Base MIP 3.9 Forensic Schedule Analysis ProtocolПредраг ПетронијевићNo ratings yet

- Bac03-Chapter 5Document25 pagesBac03-Chapter 5Rea Mariz JordanNo ratings yet

- RR 13-2000Document4 pagesRR 13-2000doraemoan100% (1)

- Disruption Innovation in ElectricityDocument6 pagesDisruption Innovation in ElectricityPrateekGuptaNo ratings yet

- Supply and Demand - Inside The BreakoutDocument5 pagesSupply and Demand - Inside The BreakoutMichael Mario100% (3)

- Clarification of Issues On The Imposition ofDocument8 pagesClarification of Issues On The Imposition ofReymund S BumanglagNo ratings yet

- UntitledDocument127 pagesUntitledemielyn lafortezaNo ratings yet

- National TaxationDocument18 pagesNational TaxationShiela Joy CorpuzNo ratings yet

- 119242-2003-China Banking Corp. v. Court of AppealsDocument17 pages119242-2003-China Banking Corp. v. Court of AppealsColleen GuimbalNo ratings yet

- DHGFHGHDocument45 pagesDHGFHGHmifajNo ratings yet

- Tax-Free Exchanges That Are Not Subject To Income Tax, Capital Gains Tax, Documentary Stamp Tax And/or Value-Added Tax, As The Case May BeDocument7 pagesTax-Free Exchanges That Are Not Subject To Income Tax, Capital Gains Tax, Documentary Stamp Tax And/or Value-Added Tax, As The Case May BeJouhara ObeñitaNo ratings yet

- Taxation of Passed-On' GRTDocument3 pagesTaxation of Passed-On' GRTjeorgiaNo ratings yet

- 2015 PRACTICE NOTES 2 Withholding Tax17022015095605 PDFDocument18 pages2015 PRACTICE NOTES 2 Withholding Tax17022015095605 PDFtendaicrosby100% (1)

- Let's Talk TaxDocument4 pagesLet's Talk TaxFiel Aldous EvidenteNo ratings yet

- Percentage TAX: Prepared By: Mrs. Nelia I. Tomas, Cpa, LPTDocument37 pagesPercentage TAX: Prepared By: Mrs. Nelia I. Tomas, Cpa, LPTTokis SabaNo ratings yet

- Finance Act 1991Document6 pagesFinance Act 1991Govardhan VaranasiNo ratings yet

- Revenue and Other Receipts: Revenue From Exchange TransactionsDocument6 pagesRevenue and Other Receipts: Revenue From Exchange TransactionsMaria Cecilia ReyesNo ratings yet

- CHAPTER 6 Final Income Taxation (Module)Document14 pagesCHAPTER 6 Final Income Taxation (Module)Shane Mark CabiasaNo ratings yet

- Faqs Withholding TaxDocument50 pagesFaqs Withholding TaxHarryNo ratings yet

- CIR v. Bank of CommerceDocument6 pagesCIR v. Bank of Commerceamareia yapNo ratings yet

- BL04 - Chapter 9 ModuleDocument8 pagesBL04 - Chapter 9 ModuleAriel A. YusonNo ratings yet

- Vat Faq EnglishDocument6 pagesVat Faq EnglishNobinNo ratings yet

- Business Income Tax (Schedule C)Document12 pagesBusiness Income Tax (Schedule C)Jichang HikNo ratings yet

- Business Tax - Chapter 5Document37 pagesBusiness Tax - Chapter 5Anie MartinezNo ratings yet

- Tax ReviewerDocument17 pagesTax ReviewerSab CardNo ratings yet

- Revisiting The Rules On Offsetting ArrangementsDocument4 pagesRevisiting The Rules On Offsetting ArrangementsRufino Gerard Moreno IIINo ratings yet

- Summary Notes Gross Receipts TaxDocument2 pagesSummary Notes Gross Receipts Taxalmira garciaNo ratings yet

- Facts:: Book ValueDocument2 pagesFacts:: Book Valueultra gayNo ratings yet

- Investment Management#2 2010Document34 pagesInvestment Management#2 2010M M PanditNo ratings yet

- Income TaxationDocument23 pagesIncome TaxationJhermaine SantiagoNo ratings yet

- M5 - Final Income TaxationDocument31 pagesM5 - Final Income TaxationTERRIUS Ace100% (1)

- Tax 05 Final Taxes Part 1Document5 pagesTax 05 Final Taxes Part 1Panda CocoNo ratings yet

- Final Income Taxation: Lesson 5Document28 pagesFinal Income Taxation: Lesson 5lc50% (4)

- Tax Treatment of Stocklending/Sale and Repurchase (Repo) TransactionsDocument5 pagesTax Treatment of Stocklending/Sale and Repurchase (Repo) TransactionsWasis SusilaNo ratings yet

- PM Reyes 2015 Bar SupplementDocument14 pagesPM Reyes 2015 Bar SupplementStarr WeigandNo ratings yet

- Department of Finance v. Asia United BankDocument19 pagesDepartment of Finance v. Asia United BankMarj BaquialNo ratings yet

- Deductibility of Interest ExpenseDocument2 pagesDeductibility of Interest ExpenseFerjeanie BernandinoNo ratings yet

- Ruling On LendingDocument3 pagesRuling On LendingRheneir MoraNo ratings yet

- Actual Receipt VS Constructive ReceiptDocument2 pagesActual Receipt VS Constructive ReceiptEduard RiparipNo ratings yet

- Taxation Report Vina MarieDocument12 pagesTaxation Report Vina MarieAnonymous gmDxRbnwONo ratings yet

- Individual Income TaxDocument19 pagesIndividual Income TaxShopee PhilippinesNo ratings yet

- BASICS OF TAXATION (Income Tax Ordinance, 1984) Updated Till Finance Act. 2013 by Prof. Mahbubur RahmanDocument14 pagesBASICS OF TAXATION (Income Tax Ordinance, 1984) Updated Till Finance Act. 2013 by Prof. Mahbubur RahmansaadmansheedyNo ratings yet

- 24-2011 RMCDocument12 pages24-2011 RMCJacobfranNo ratings yet

- Tds GuidelineDocument23 pagesTds GuidelineYash BhayaniNo ratings yet

- TAXSDocument10 pagesTAXSEmmanuelNo ratings yet

- Classroom Notes On DSTDocument6 pagesClassroom Notes On DSTLalaine ReyesNo ratings yet

- BH Vat and Frequently Asked QuestionsDocument6 pagesBH Vat and Frequently Asked QuestionsJamesNo ratings yet

- G.R. No. 147375 June 26, 2006 Commissioner of Internal Revenue, Petitioner, Bank of The Philippine Islands, RespondentDocument11 pagesG.R. No. 147375 June 26, 2006 Commissioner of Internal Revenue, Petitioner, Bank of The Philippine Islands, RespondentShie DiazNo ratings yet

- Taxation IIDocument3 pagesTaxation IIAnonymous BNrz1arNo ratings yet

- G.R. No. 147375 June 26, 2006 Commissioner of Internal Revenue, Petitioner, Bank of The Philippine Islands, RespondentDocument39 pagesG.R. No. 147375 June 26, 2006 Commissioner of Internal Revenue, Petitioner, Bank of The Philippine Islands, RespondentMadel PresquitoNo ratings yet

- Chapter 13 Lecture Notes (TA 2020) - Non-Financial and Current LiabilitiesDocument20 pagesChapter 13 Lecture Notes (TA 2020) - Non-Financial and Current LiabilitiesTSEvansNo ratings yet

- Vat On BanksDocument4 pagesVat On BanksRolando VasquezNo ratings yet

- Cir Vs Bank of Commerce DigestDocument3 pagesCir Vs Bank of Commerce Digestwaws20No ratings yet

- Case DigestsDocument67 pagesCase DigestsCattleyaNo ratings yet

- MASB5 Cash Flow Statements Pg3Document2 pagesMASB5 Cash Flow Statements Pg3hyraldNo ratings yet

- CIR v. AmEx (Digest)Document3 pagesCIR v. AmEx (Digest)Tini GuanioNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- CPA Financial Accounting and Reporting: Second EditionFrom EverandCPA Financial Accounting and Reporting: Second EditionNo ratings yet

- Arta Ad StarDocument3 pagesArta Ad StarMarc Myer De AsisNo ratings yet

- Team Bok Annual Biga 2022 - FinalDocument2 pagesTeam Bok Annual Biga 2022 - FinalMarc Myer De AsisNo ratings yet

- Cta 3D CV 08962 D 2016jul22 RefDocument20 pagesCta 3D CV 08962 D 2016jul22 RefMarc Myer De AsisNo ratings yet

- Team Bok Annual Biga 2022Document2 pagesTeam Bok Annual Biga 2022Marc Myer De AsisNo ratings yet

- Cta Eb CV 00499 D 2009nov26 RefDocument17 pagesCta Eb CV 00499 D 2009nov26 RefMarc Myer De AsisNo ratings yet

- BSP Report SuperduperfinalDocument57 pagesBSP Report SuperduperfinalMarc Myer De AsisNo ratings yet

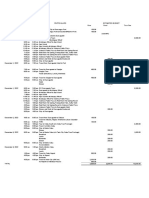

- Date Purchased Particulars Unit Price QTY: Cargo Button Down 140.00 0Document12 pagesDate Purchased Particulars Unit Price QTY: Cargo Button Down 140.00 0Marc Myer De AsisNo ratings yet

- Bangko Sentral NG Pilipinas - Report EconDocument46 pagesBangko Sentral NG Pilipinas - Report EconMarc Myer De AsisNo ratings yet

- Iloilo Enhanced DRR - Cca PDPFP 2014-2020-CompressedDocument432 pagesIloilo Enhanced DRR - Cca PDPFP 2014-2020-CompressedMarc Myer De Asis100% (1)

- Iloilo Investment and DevelopmentDocument17 pagesIloilo Investment and DevelopmentMarc Myer De AsisNo ratings yet

- Iloilo Investment and DevelopmentDocument51 pagesIloilo Investment and DevelopmentMarc Myer De AsisNo ratings yet

- Reviewer in Business ResearchDocument4 pagesReviewer in Business ResearchMarc Myer De AsisNo ratings yet

- Reviewer in Marketing ManagementDocument16 pagesReviewer in Marketing ManagementMarc Myer De AsisNo ratings yet

- Reviewer in Organization and ManagementDocument3 pagesReviewer in Organization and ManagementMarc Myer De AsisNo ratings yet

- Reviewer in Marketing Management - 2Document4 pagesReviewer in Marketing Management - 2Marc Myer De AsisNo ratings yet

- Service Quality and Customer Satisfaction in Hotel Industry Master ThesisDocument4 pagesService Quality and Customer Satisfaction in Hotel Industry Master Thesisgingermartinerie100% (2)

- Form 21 - Pull-Out and Transfer To Supplier of Gaming Equipment Notification FormDocument4 pagesForm 21 - Pull-Out and Transfer To Supplier of Gaming Equipment Notification FormPio BilazonNo ratings yet

- An Introduction To Cryptocurrency Reading Comprehension NameDocument3 pagesAn Introduction To Cryptocurrency Reading Comprehension NameyassineNo ratings yet

- University of Nairobi Faculty of Business and Management Science Microfinance Assignment Submitted To: Prof Josiah AdudaDocument25 pagesUniversity of Nairobi Faculty of Business and Management Science Microfinance Assignment Submitted To: Prof Josiah AdudaMohamed LibanNo ratings yet

- Thesis Logistics Supply Chain ManagementDocument7 pagesThesis Logistics Supply Chain Managementafktdftdvqtiom100% (1)

- Portfolio and Services - MuradDocument22 pagesPortfolio and Services - Muradronica24sethNo ratings yet

- Mis Test 2 PDFDocument23 pagesMis Test 2 PDFAA BB MMNo ratings yet

- Final Internship ReportDocument28 pagesFinal Internship ReportMd. Mainul IslamNo ratings yet

- The Ultimate B2B E-Commerce GuideDocument21 pagesThe Ultimate B2B E-Commerce Guideviniciusgs9350% (2)

- Whitepaper Ef4d108a4c087eab5358Document8 pagesWhitepaper Ef4d108a4c087eab5358Yerumoh DanielNo ratings yet

- Bank of America NT & Sa, The Commissioner of Internal RevenueDocument4 pagesBank of America NT & Sa, The Commissioner of Internal RevenueHADTUGINo ratings yet

- 28 Days Accounts Challenge-1Document13 pages28 Days Accounts Challenge-1krishnaeatpute777No ratings yet

- ICE JLA Webinar Notice - June 2023 PDFDocument2 pagesICE JLA Webinar Notice - June 2023 PDFRiza SuwondoNo ratings yet

- Workshop Cost EstimatingDocument22 pagesWorkshop Cost EstimatinghasanNo ratings yet

- 5TH.B Provisions, Contingent Liabilities and Contingent AssetsDocument4 pages5TH.B Provisions, Contingent Liabilities and Contingent AssetsAnthony DyNo ratings yet

- Coffee Cafe B Plan 1Document31 pagesCoffee Cafe B Plan 1Dino DizonNo ratings yet

- PGDHRM Paper I Unit 6Document25 pagesPGDHRM Paper I Unit 6sfghNo ratings yet

- Business Plan Report (Jhaa SDN BHD)Document86 pagesBusiness Plan Report (Jhaa SDN BHD)afnanNo ratings yet

- Department of Labor: State Contacts CY 2006Document14 pagesDepartment of Labor: State Contacts CY 2006USA_DepartmentOfLaborNo ratings yet

- Flaw of Averages SummaryDocument2 pagesFlaw of Averages SummaryZofigan khawajaNo ratings yet

- Home Econs J 3Document4 pagesHome Econs J 3wealthiykejephNo ratings yet

- Advanced Financial Management - Spring2018 PDFDocument3 pagesAdvanced Financial Management - Spring2018 PDFPhúc PhanNo ratings yet