You might also like

- The Basics of Life Insurance: The Answer to What Life Insurance is and How It Works: Personal Finance, #1From EverandThe Basics of Life Insurance: The Answer to What Life Insurance is and How It Works: Personal Finance, #1No ratings yet

- Q - 13 Insurance PolicyDocument26 pagesQ - 13 Insurance PolicyMAHENDRA SHIVAJI DHENAKNo ratings yet

- Life Insurance Products & Terms PDFDocument16 pagesLife Insurance Products & Terms PDFSuman SinhaNo ratings yet

- Term Life Insurance ExplainedDocument3 pagesTerm Life Insurance ExplainedAbhishek TendulkarNo ratings yet

- INSURANCEDocument28 pagesINSURANCEcharuNo ratings yet

- Unit 5 Life and Health InsuranceDocument19 pagesUnit 5 Life and Health InsuranceMahlet AbrahaNo ratings yet

- Risk CH 5 PDFDocument14 pagesRisk CH 5 PDFWonde BiruNo ratings yet

- Lecture - 6 Life InsuranceDocument15 pagesLecture - 6 Life Insurancegyanprakashdeb302No ratings yet

- Money Back PolicyDocument58 pagesMoney Back PolicyUppal Patel83% (6)

- Chap 5Document18 pagesChap 5yhikmet613No ratings yet

- Types of Life Insurance PoliciesDocument21 pagesTypes of Life Insurance PoliciesDivya PillaiNo ratings yet

- Wa0006.Document3 pagesWa0006.Sonu AnandNo ratings yet

- 1 Types of Life Insurance Plans & ULIPSDocument40 pages1 Types of Life Insurance Plans & ULIPSJaswanth Singh RajpurohitNo ratings yet

- CHAP5Life HealthDocument10 pagesCHAP5Life HealthEbsa AdemeNo ratings yet

- Session 3 Life Insurance Products: Conventional Plans - Non Participating PlansDocument30 pagesSession 3 Life Insurance Products: Conventional Plans - Non Participating Plansm_dattaiasNo ratings yet

- Banking and InsuranceDocument20 pagesBanking and Insurancebeena antuNo ratings yet

- Life Insurance ProductsDocument7 pagesLife Insurance ProductsalaguNo ratings yet

- Life Insurance Basics EbookDocument11 pagesLife Insurance Basics Ebooknoexam1100% (3)

- Meaning of Life Insurance and It Types of PoliciesDocument2 pagesMeaning of Life Insurance and It Types of Policiesshakti ranjan mohanty100% (1)

- Icici PrudentialDocument33 pagesIcici PrudentialDiksha KukrejaNo ratings yet

- Handbook On Life InsuranceDocument17 pagesHandbook On Life InsuranceDeeptiNo ratings yet

- 8 (22) (Read-Only)Document54 pages8 (22) (Read-Only)Kookie ShresthaNo ratings yet

- RISK Chapter 5Document19 pagesRISK Chapter 5Taresa AdugnaNo ratings yet

- Life insurance typesDocument6 pagesLife insurance typesrahulNo ratings yet

- Group members and life insurance definitionsDocument20 pagesGroup members and life insurance definitionsMilton Rosario MoraesNo ratings yet

- Life Insurance BasicsDocument10 pagesLife Insurance BasicsRitika SharmaNo ratings yet

- Life InsuranceDocument7 pagesLife Insurancerupesh_kanabar1604100% (8)

- Types of Life Insurance PoliciesDocument11 pagesTypes of Life Insurance PoliciesOsman GaniNo ratings yet

- #14 Aesthetic MintDocument37 pages#14 Aesthetic MintPahilangco, ErikaNo ratings yet

- Types of Life InsuranceDocument5 pagesTypes of Life InsuranceFatema KhambatiNo ratings yet

- Types of InsuranceDocument2 pagesTypes of InsuranceS GaneshNo ratings yet

- Everything You Need to Know About Life Insurance Types and PlansDocument25 pagesEverything You Need to Know About Life Insurance Types and PlansWaheed AliNo ratings yet

- Insurance Commission Exam ReviewerDocument5 pagesInsurance Commission Exam ReviewerApolinar Alvarez Jr.97% (38)

- Insurance ServiceDocument31 pagesInsurance Servicepjsv12345No ratings yet

- Term Life Insurance FinalDocument10 pagesTerm Life Insurance FinalsearchingnobodyNo ratings yet

- 1Document6 pages1Lalosa Fritz Angela R.No ratings yet

- Life Insurance:: Principles & Practices of Insurance Unit 3Document6 pagesLife Insurance:: Principles & Practices of Insurance Unit 3ashishsinghashishNo ratings yet

- Insurance TutorialDocument11 pagesInsurance TutorialSadhvi SinghNo ratings yet

- Chapter Five Life and Health InsuranceDocument10 pagesChapter Five Life and Health InsuranceHayelom Tadesse GebreNo ratings yet

- InsuranceDocument2 pagesInsurancesobhencNo ratings yet

- How Life Insurance Differ From OtherDocument2 pagesHow Life Insurance Differ From OtherishwarNo ratings yet

- Top 4 Life Insurance TypesDocument6 pagesTop 4 Life Insurance Typesdipen007No ratings yet

- Term Life Insurance PolicyDocument4 pagesTerm Life Insurance PolicyShubham NamdevNo ratings yet

- Life Insurance Products - I: Chapter IntroductionDocument7 pagesLife Insurance Products - I: Chapter IntroductionMaulik PanchmatiaNo ratings yet

- Unit - 3 Bilp Types of Life Insurance - Features - ConditionsDocument9 pagesUnit - 3 Bilp Types of Life Insurance - Features - ConditionsYashika GuptaNo ratings yet

- 8-Life InsuranceDocument51 pages8-Life InsuranceKartik BhartiaNo ratings yet

- Life Assurance 225 KDocument18 pagesLife Assurance 225 KRiajul islamNo ratings yet

- Insurance Law Module- 2Document15 pagesInsurance Law Module- 2xakij19914No ratings yet

- Origin of The Company: Meaning and Definition Nature and Scope Importance of Insurance Objectives of The StudyDocument32 pagesOrigin of The Company: Meaning and Definition Nature and Scope Importance of Insurance Objectives of The Studypav_deshpande8055No ratings yet

- Poi New 1Document6 pagesPoi New 1Anil Bhard WajNo ratings yet

- Rashdullah Shah 133Document14 pagesRashdullah Shah 133Rashdullah Shah 133No ratings yet

- Insurance Promotion - IIDocument12 pagesInsurance Promotion - IIAditi JainNo ratings yet

- What Is Life Insurance in 40 CharactersDocument7 pagesWhat Is Life Insurance in 40 CharactersAustin MathiasNo ratings yet

- B&I Unit 5Document19 pagesB&I Unit 5saisri nagamallaNo ratings yet

- Product & ServiceDocument11 pagesProduct & ServicefarrukhNo ratings yet

- Insurance basics explained in 40 charactersDocument5 pagesInsurance basics explained in 40 charactersDebasis NayakNo ratings yet

- Insurance Is A Cover Used For Protecting Oneself From The Risk of A Financial LossDocument7 pagesInsurance Is A Cover Used For Protecting Oneself From The Risk of A Financial Losspepsico_shabnamNo ratings yet

- Life InsuranceDocument13 pagesLife Insurancesmiley12345678910No ratings yet

- Personal Finance-Types of Life InsuranceDocument12 pagesPersonal Finance-Types of Life InsurancePriyaNo ratings yet

- Company Profile BirlaDocument31 pagesCompany Profile BirlaShivayu VaidNo ratings yet

- TallyDocument1 pageTallyPriya ShindeNo ratings yet

- Risk Management Tools for Retirement Planning and Employee BenefitsDocument30 pagesRisk Management Tools for Retirement Planning and Employee BenefitsPriya ShindeNo ratings yet

- Capital & Financial MarketsDocument14 pagesCapital & Financial MarketsPriya ShindeNo ratings yet

- Unit 2 Public Speaking e BookDocument19 pagesUnit 2 Public Speaking e BookPriya ShindeNo ratings yet

- Problem Solving and Decision Making SkillsDocument11 pagesProblem Solving and Decision Making SkillsPriya ShindeNo ratings yet

- Priyanka Dattatray Shinde: Skills EducationDocument1 pagePriyanka Dattatray Shinde: Skills EducationPriya ShindeNo ratings yet

- Unit 9Document19 pagesUnit 9Priya ShindeNo ratings yet

- Security Analysis & Portfolio ManagementDocument18 pagesSecurity Analysis & Portfolio ManagementPriya ShindeNo ratings yet

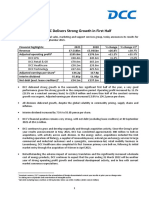

- DCC Delivers Strong Growth in First HalfDocument39 pagesDCC Delivers Strong Growth in First HalfPriya ShindeNo ratings yet

- CamelDocument21 pagesCamelSiva SankariNo ratings yet

- A-Life Joy - Brochure - 6th EditDocument12 pagesA-Life Joy - Brochure - 6th EditYF OngNo ratings yet

- Investment Fundamentals Guide PDFDocument36 pagesInvestment Fundamentals Guide PDFSewale AbateNo ratings yet

- The Economic Outlook For California Pistachios: Steven C. BlankDocument17 pagesThe Economic Outlook For California Pistachios: Steven C. BlankmohammadebrahimiNo ratings yet

- Repositioning Asia After the CrisisDocument34 pagesRepositioning Asia After the Crisischiswick59100% (1)

- B&IDocument11 pagesB&IPravin ThakurNo ratings yet

- Report Mrs. MorenoDocument24 pagesReport Mrs. MorenoRishelle Mae C. AcademíaNo ratings yet

- CourseDocument4 pagesCoursegilberthufana446877No ratings yet

- What is a Credit Default Swap (CDSDocument19 pagesWhat is a Credit Default Swap (CDSPurnima Bhartia BankaNo ratings yet

- Portfolio Restructuring DilemmaDocument7 pagesPortfolio Restructuring DilemmaVarun AgrawalNo ratings yet

- Governance DEFINITIONDocument9 pagesGovernance DEFINITIONCygresy GomezNo ratings yet

- Syllabus For INS ExamsDocument2 pagesSyllabus For INS ExamsNitin Kolte100% (1)

- Smart Scholar - One Pager - BR - New SizeDocument2 pagesSmart Scholar - One Pager - BR - New Sizeraghuvardhan41No ratings yet

- Brazil Syndicate List Q1 2021Document2 pagesBrazil Syndicate List Q1 2021alinNo ratings yet

- M and B 3 Hybrid 3rd Edition Dean Croushore Solutions ManualDocument35 pagesM and B 3 Hybrid 3rd Edition Dean Croushore Solutions Manualallodiumerrantialwmpi100% (22)

- Risk Premia Strategies B 102727740Document29 pagesRisk Premia Strategies B 102727740h_jacobson100% (4)

- Micro Insurance HDocument46 pagesMicro Insurance HNirupa KrishnaNo ratings yet

- Insurance Contract Law NotesDocument10 pagesInsurance Contract Law NotesTay Min Si100% (2)

- HIRARC form risk assessment templateDocument4 pagesHIRARC form risk assessment templateAlexandra Nicole GatdulaNo ratings yet

- VUL Mock Exam 1 - June 6, 2011 Version 1Document11 pagesVUL Mock Exam 1 - June 6, 2011 Version 1Anonymous iOYkz0w73% (44)

- New Microsoft Office Word DocumentDocument18 pagesNew Microsoft Office Word DocumentSubhasish BhattacharjeeNo ratings yet

- Chapter08 InsuransDocument27 pagesChapter08 InsuransChoo Wei shengNo ratings yet

- Project ReportDocument59 pagesProject ReportAnuj YeleNo ratings yet

- Subject: Insurance Law: PROJECT ON: Double Insurance & Re-Insurance - Indian PerspectiveDocument20 pagesSubject: Insurance Law: PROJECT ON: Double Insurance & Re-Insurance - Indian PerspectiveSachin PatelNo ratings yet

- Risk & ReturnDocument26 pagesRisk & ReturnAmit RoyNo ratings yet

- Book1Document8 pagesBook1dhrivsitlani29No ratings yet

- Premco Product Guide 2020-2021 PDFDocument16 pagesPremco Product Guide 2020-2021 PDFCrawford BoydNo ratings yet

- AP3443E 11 13 Outbound Telemarketing Script Auto To HomeDocument2 pagesAP3443E 11 13 Outbound Telemarketing Script Auto To Homedipankar palNo ratings yet

- Risk Management Solution Manual Chapter 03Document8 pagesRisk Management Solution Manual Chapter 03DanielLam71% (7)

- Insurance Law HighlightsDocument9 pagesInsurance Law HighlightsRaquel DoqueniaNo ratings yet