You might also like

- San Beda College Alabang Homework Exercise-Act851RDocument4 pagesSan Beda College Alabang Homework Exercise-Act851RJomel BaptistaNo ratings yet

- Sabina Company Quiz #1 Questions and SolutionsDocument6 pagesSabina Company Quiz #1 Questions and SolutionsJames Daniel SwintonNo ratings yet

- Problems: Problem 1-1Document4 pagesProblems: Problem 1-1Gwen Cornet Pugal Alimo-ot0% (1)

- Examination About Investment 7Document3 pagesExamination About Investment 7BLACKPINKLisaRoseJisooJennieNo ratings yet

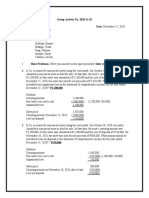

- Group Activity No. 2-Noncurrent Asset Held For Sale-2Document3 pagesGroup Activity No. 2-Noncurrent Asset Held For Sale-2Jericho VillalonNo ratings yet

- Baliuag University CPA Review Problems on Discontinued Operations and Noncurrent Assets Held for SaleDocument64 pagesBaliuag University CPA Review Problems on Discontinued Operations and Noncurrent Assets Held for SaleKezNo ratings yet

- FdsedjwhajdhkudshdhxDocument28 pagesFdsedjwhajdhkudshdhxJoylyn CombongNo ratings yet

- Sacrosanct Company Problem 26 - 5 (INTACCS Problem)Document1 pageSacrosanct Company Problem 26 - 5 (INTACCS Problem)Ya NaNo ratings yet

- Activity in E3 - LiabilitiesDocument9 pagesActivity in E3 - LiabilitiesPaupau100% (1)

- Warranty Liability Lesson on Accrual and Expense RecognitionDocument15 pagesWarranty Liability Lesson on Accrual and Expense RecognitionCirelle Faye Silva0% (1)

- Accounting 132Document2 pagesAccounting 132Anne Marieline BuenaventuraNo ratings yet

- IA2 ProvisionDocument21 pagesIA2 ProvisionMitchie Faustino100% (1)

- Hotcake Mix Premium Expense and Liability CalculationDocument4 pagesHotcake Mix Premium Expense and Liability CalculationChristian N MagsinoNo ratings yet

- 62230126Document20 pages62230126ROMULO CUBIDNo ratings yet

- Worsksheet #1Document4 pagesWorsksheet #1Sharmin ReulaNo ratings yet

- Charisma Company Required 1 Date Interest Received Interest Income Discount Amortization Carrying AmountDocument2 pagesCharisma Company Required 1 Date Interest Received Interest Income Discount Amortization Carrying AmountAnonnNo ratings yet

- ProblemsDocument7 pagesProblemsHanna Mae Arcilla67% (6)

- This Study Resource Was: Assessment Task 3Document5 pagesThis Study Resource Was: Assessment Task 3maria evangelistaNo ratings yet

- Assignment 7 On Chapt 3 Problem 3 17 On Page 93Document2 pagesAssignment 7 On Chapt 3 Problem 3 17 On Page 93Joylyn CombongNo ratings yet

- Compileeee Business CombiDocument14 pagesCompileeee Business CombiEddie Mar JagunapNo ratings yet

- 5APRACTICE QUIZ - SHARE-BASED COMPENSATION (Share Options)Document2 pages5APRACTICE QUIZ - SHARE-BASED COMPENSATION (Share Options)Cath.PernNo ratings yet

- Toyota CompanyDocument2 pagesToyota Companykel data100% (2)

- Chapter 24 Answer KeyDocument3 pagesChapter 24 Answer KeyShane TabunggaoNo ratings yet

- Cabug-Os, Lovely A. (Assignment 9)Document2 pagesCabug-Os, Lovely A. (Assignment 9)Joylyn CombongNo ratings yet

- Seatwork 2B ASSIGNDocument5 pagesSeatwork 2B ASSIGNYzzabel Denise L. Tolentino100% (1)

- Note Payable practice exercise FDocument9 pagesNote Payable practice exercise Flana del reyNo ratings yet

- Investment in Bonds / Financial Assets at Amortized CostDocument1 pageInvestment in Bonds / Financial Assets at Amortized CostSteffanie Olivar0% (1)

- Activity 3-4 SB CompensationDocument3 pagesActivity 3-4 SB CompensationNhel Alvaro0% (1)

- Chapter 27Document12 pagesChapter 27Crizel DarioNo ratings yet

- Statement of Comprehensive Income Cost of Goods Sold and Operating Expenses Problem 4-1 (AICPA Adapted)Document11 pagesStatement of Comprehensive Income Cost of Goods Sold and Operating Expenses Problem 4-1 (AICPA Adapted)Clarisse PelayoNo ratings yet

- Land Purchase Journal EntriesDocument1 pageLand Purchase Journal Entrieshae1234No ratings yet

- Note Receivable Part 2Document7 pagesNote Receivable Part 2Carlo VillanNo ratings yet

- AC - IntAcctg1 Quiz 03 With AnswersDocument3 pagesAC - IntAcctg1 Quiz 03 With AnswersSherri BonquinNo ratings yet

- Intermediate Accounting 2Document27 pagesIntermediate Accounting 2CARMINA SANCHEZNo ratings yet

- PAS37 ProbsDocument4 pagesPAS37 ProbsAngelicaNo ratings yet

- Contingent Liability LessonDocument14 pagesContingent Liability LessonJerald Jay Capistrano Catacutan100% (1)

- p2 Guerrero ch15Document30 pagesp2 Guerrero ch15Clarissa Teodoro100% (1)

- Machete Company Requirement: Prepare Journal Entries Debit CreditDocument1 pageMachete Company Requirement: Prepare Journal Entries Debit CreditAnonnNo ratings yet

- Moses Company bond issuance calculation of discount amountDocument3 pagesMoses Company bond issuance calculation of discount amountLouiseNo ratings yet

- Financial Accounting 2 ExamDocument9 pagesFinancial Accounting 2 ExamEzekiel MalazzabNo ratings yet

- LiabilitiesDocument8 pagesLiabilitiesGerald F. SalasNo ratings yet

- IA Activity 6 AssDocument6 pagesIA Activity 6 AssWeStan LegendsNo ratings yet

- Practice Set Review - Current LiabilitiesDocument12 pagesPractice Set Review - Current LiabilitiesKayla MirandaNo ratings yet

- Manufacturing Hypothesis TestingDocument5 pagesManufacturing Hypothesis TestingJessa Delos SantosNo ratings yet

- Accounting 1 - PPEDocument38 pagesAccounting 1 - PPEPortia TurianoNo ratings yet

- FinAcc 3 QuizzesDocument9 pagesFinAcc 3 QuizzesStella SabaoanNo ratings yet

- Razor Company Required Debit Credit 2020Document14 pagesRazor Company Required Debit Credit 2020AnonnNo ratings yet

- 1 LiabilitiesDocument39 pages1 LiabilitiesDiana Faith TaycoNo ratings yet

- CSTC College of Sciences Technology and Communication, IncDocument35 pagesCSTC College of Sciences Technology and Communication, IncJohn Patrick MercurioNo ratings yet

- Chapter 15 Financial Asset at Fair ValueDocument7 pagesChapter 15 Financial Asset at Fair ValueRujean Salar Altejar100% (1)

- Warranties, Provisions and Contingent LiabilitiesDocument31 pagesWarranties, Provisions and Contingent LiabilitiesHazel Jane EsclamadaNo ratings yet

- This Study Resource Was: Chapter 18: Accounts ReceivableDocument7 pagesThis Study Resource Was: Chapter 18: Accounts ReceivableXENA LOPEZNo ratings yet

- Valix 2 Chapt 24 25 PDFDocument20 pagesValix 2 Chapt 24 25 PDFivyaguasarnaldo4everNo ratings yet

- 9.2 Investment in AssociateDocument6 pages9.2 Investment in AssociateJorufel PapasinNo ratings yet

- Quiz 1 On Mid Term Period - Notes ReceivableDocument3 pagesQuiz 1 On Mid Term Period - Notes ReceivableErille Julianne (Rielianne)No ratings yet

- Worksheet No.1 (02/03/22)Document3 pagesWorksheet No.1 (02/03/22)Sharmin ReulaNo ratings yet

- Module 2Document28 pagesModule 2Jiane SanicoNo ratings yet

- Quiz - Chapter 2.problemsDocument2 pagesQuiz - Chapter 2.problemsQueenie Joy TagupaNo ratings yet

- Prelim Exam - Intermediate AccountingDocument4 pagesPrelim Exam - Intermediate AccountingLea Gabrielle Fariola0% (1)

- Chapter 2 - Premium LiabilityDocument20 pagesChapter 2 - Premium Liabilitymyx enrileNo ratings yet

- SILVA, Cirelle Faye, T. - Journal #4Document1 pageSILVA, Cirelle Faye, T. - Journal #4Cirelle Faye SilvaNo ratings yet

- SIS OLAH HBC 11132021 PPT Final Final FinalDocument55 pagesSIS OLAH HBC 11132021 PPT Final Final FinalCirelle Faye SilvaNo ratings yet

- DYSAS QuestionairesDocument5 pagesDYSAS QuestionairesAngelica Manaois100% (1)

- Lesson10 11 Lessee-AccountingDocument14 pagesLesson10 11 Lessee-AccountingCirelle Faye SilvaNo ratings yet

- HBC Sis. VeronDocument52 pagesHBC Sis. VeronCirelle Faye SilvaNo ratings yet

- Sis Danica HBC Powerpoint DesignDocument30 pagesSis Danica HBC Powerpoint DesignCirelle Faye SilvaNo ratings yet

- Lesson5&6 - Bonds PayableDocument27 pagesLesson5&6 - Bonds PayableCirelle Faye SilvaNo ratings yet

- Lesson8 - Notes PayableDocument13 pagesLesson8 - Notes PayableCirelle Faye SilvaNo ratings yet

- Lesson 8 Notes PayableDocument1 pageLesson 8 Notes PayableCirelle Faye SilvaNo ratings yet

- Lesson9 - Debt RestructureDocument14 pagesLesson9 - Debt RestructureCirelle Faye SilvaNo ratings yet

- Lesson 5 - 6 Bonds Payable - Effective Interest MethodDocument1 pageLesson 5 - 6 Bonds Payable - Effective Interest MethodCirelle Faye SilvaNo ratings yet

- Lesson7 - Compound Financial InstrumentDocument15 pagesLesson7 - Compound Financial InstrumentCirelle Faye SilvaNo ratings yet

- Provisions, Contingent Liabilities and Assets ExplainedDocument18 pagesProvisions, Contingent Liabilities and Assets ExplainedCirelle Faye SilvaNo ratings yet

- Warranty Liability Lesson on Accrual and Expense RecognitionDocument15 pagesWarranty Liability Lesson on Accrual and Expense RecognitionCirelle Faye Silva0% (1)

- Liabilities Technical Knowledge: Lesson 1Document12 pagesLiabilities Technical Knowledge: Lesson 1Cirelle Faye SilvaNo ratings yet

- Nike Financial Analysis - EditedDocument12 pagesNike Financial Analysis - EditedmosesNo ratings yet

- Icse 2024 Specimen 631 CSTDocument7 pagesIcse 2024 Specimen 631 CSTShweta SamantNo ratings yet

- Income and Expense Summaries for PartnershipsDocument18 pagesIncome and Expense Summaries for PartnershipsCrestina100% (3)

- Draft SBLC Icbc Akhir-2Document2 pagesDraft SBLC Icbc Akhir-2PT ANUGRAH ENERGY NUSANTARANo ratings yet

- Cash and Cash Equivalents PDFDocument7 pagesCash and Cash Equivalents PDFFritzey Faye RomeronaNo ratings yet

- 1.4. Partnership LiquidationDocument6 pages1.4. Partnership LiquidationKPoPNyx EditsNo ratings yet

- Final Solution Sybaf Fa QP Code 22810Document11 pagesFinal Solution Sybaf Fa QP Code 22810praveenk1878No ratings yet

- Interim Financial ReportingDocument3 pagesInterim Financial ReportingPaula De RuedaNo ratings yet

- Quality Control ChecklistDocument7 pagesQuality Control Checklistdarma bonarNo ratings yet

- Ray Dalio Consistently Deliver ReturnsDocument2 pagesRay Dalio Consistently Deliver ReturnsnabsNo ratings yet

- An Analysis of Customer PerceptionDocument28 pagesAn Analysis of Customer PerceptionAshis SahooNo ratings yet

- Kings of Capital: An Investment Strategy From Marcellus Investment ManagersDocument36 pagesKings of Capital: An Investment Strategy From Marcellus Investment Managerssiva sagarNo ratings yet

- QuickBooks For BeginnersDocument3 pagesQuickBooks For BeginnersZain U Ddin0% (1)

- URA Payment Slip TitleDocument1 pageURA Payment Slip TitleDaniel Kyeyune MuwangaNo ratings yet

- Principles of AuditingDocument148 pagesPrinciples of AuditingAsteway MesfinNo ratings yet

- 02 Edu91 FM Practice Sheets QuestionsDocument77 pages02 Edu91 FM Practice Sheets Questionsprince soniNo ratings yet

- Chapter Twenty-One: Managing Liquidity Risk On The Balance SheetDocument26 pagesChapter Twenty-One: Managing Liquidity Risk On The Balance SheetSagheer MuhammadNo ratings yet

- General Mathematics Module For ShsDocument9 pagesGeneral Mathematics Module For Shsdiego pakloyNo ratings yet

- Banking and Finance Project Topics and MaterialsDocument3 pagesBanking and Finance Project Topics and MaterialsAlo Peter taiwoNo ratings yet

- T1-FRM-3-Ch3-Governance-v3.1 - Study NotesDocument12 pagesT1-FRM-3-Ch3-Governance-v3.1 - Study NotescristianoNo ratings yet

- Principles: Module 3 - Assumptions and AccountingDocument3 pagesPrinciples: Module 3 - Assumptions and AccountingCriselito EnigrihoNo ratings yet

- Banking Laws 2018 2019 SummerDocument5 pagesBanking Laws 2018 2019 SummerJonathanNo ratings yet

- Credit Rating Agency CraDocument46 pagesCredit Rating Agency CravmktptNo ratings yet

- Question Chapter2 Final 1Document19 pagesQuestion Chapter2 Final 1Tran An KhanhNo ratings yet

- (CPAR2016) TAX-8014 (+llamado Notes - OTHER PERCENTAGE TAXES)Document12 pages(CPAR2016) TAX-8014 (+llamado Notes - OTHER PERCENTAGE TAXES)jamNo ratings yet

- CH - 13 - Central Banks and The Federal Reserve SystemDocument33 pagesCH - 13 - Central Banks and The Federal Reserve SystemVishNo ratings yet

- November 14,2011 VAT Number:PHV/24002311718 Customer: Eleme Petrochemical Limited Eleme, Port Harcourt Rivers StateDocument2 pagesNovember 14,2011 VAT Number:PHV/24002311718 Customer: Eleme Petrochemical Limited Eleme, Port Harcourt Rivers StateDaku JoelNo ratings yet

- Pre-Test Basic FinanceDocument3 pagesPre-Test Basic FinanceMoraya P. CacliniNo ratings yet