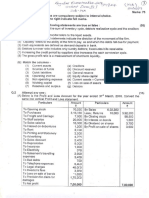

1. The Balance sheet of a company are as follows: Net profit for the year was Rs.

Net profit for the year was Rs. 40000 and dividend declared during the year was Rs.

Equities 2072 Rs. 2073 Rs. Assets 2072 Rs. 2073 Rs. 30000. 5% Debenture were redeemed at 10% premium.Required: Cash flow from

Share capital 400000 630000 Land & building 360000 425000 financing activities

8% debenture 300000 150000 Plant & equipment 270000 370000

Current Liabilities 80000 112400 Inventory 90000 60000 3. The balance sheet and income statement of a company for two years are given below:

Profit & loss a/c 30000 77600 Book debts 35000 45000 Balance Sheet

Cash at bank 55000 70000 Liabilities Year 4 Year 5 Assets Year 4 Year 5

Total 810000 970000 Total 810000 970000 Share capital 400000 500000 Plant and 500000 550000

machinery

The income statement of 2073 is as follows: Share premium 40000 50000 Investment 120000 70000

Particulars Rs. Rs. Profit and loss a/c 40000 120000 Book debts 100000 120000

Sales 600000 Debenture 250000 100000 Stock 175000 125000

Less: Cost of goods sold: Creditors 80000 50000 Prepaid 10000 15000

Opening inventory 90000 expenses

Purchase of Materials 160000 Provision for 50000 35000 Bank 165000 205000

dividend

Closing inventory (60000)

Accumulated 210000 230000

190000 depreciation

Wages 120000 310000 1070000 108500 1070000 1085000

Gross profit 290000 0

Less: Operating expenses 90000

Depreciation 30000 120000 Income statement for year 5

170000 Sales revenue 10,00,000

Less: Interest on debenture 24000 Less: Cost of goods sold:

146000 Beginning stock 90000

Less: Tax 58400 Add: Purchase 400000

87600 Less: Ending stock 120000

Less: Dividend 40000 370000

Retained earnings 47600 Wages 230000 600000

Gross profit 400000

Required:

a) Cash flow statement using direct method (170000,(195000),40000) Less: Operating expenses:

b) Comment on cash flow from Operating, Investing and Financing activities. General expenses 170000

c) If you were a financial manager of this company what would be your comment Depreciation 50000

regarding the financial performance of this company. Interest 25000

Premium on debenture retired 15000

2. The following opening and closing balances are extracted from the Balance Sheet of Provision for dividend 40000 300000

a company 100000

Add: Gain on sale of plant (Cost Rs. 100000

Opening Balance Closing Balance accumulated depreciation Rs. 30000) 25000

Rs. Rs. 125000

5% Debenture 80000 50000 Less: Loss on sale of investment 10000

Long Term Bank Loan 25000 40000 115000

Provision for dividend 30000 40000 Less: Tax 35000

Plant and equipment 150000 225000 Net income 80000

Share capital 200000 300000 Required:

Share premium 40000 50000 a. Cash flow statement using direct approach

Retained earning 20000 30000 (Ans: CFOA = Rs. 165000; CFIA = Rs. (15000); CFFA = Rs. (110000))

b. Comment each of the components of a cash flows statement.

� c. As a financial manager of this company, how do you comment about this

company?

4. The balance sheet and income statement of a company for two years are given below: 5. The balance sheet and income statement of a company for two years are given below:

Balance Sheet Balance Sheet

Liabilities Year 2 Year 1 Assets Year 2 Year 1 Liabilities Year 1 Year 2 Assets Year 1 Year 2

Share capital 1200000 1000000 Plant 1600000 1200000 Share capital 700000 1000000 Fixed assets 1090000 1630000

Share premium 120000 100000 Inventories 200000 100000 Share premium 70000 100000 Inventory 100000 130000

10% Debenture 100000 200000 Account receivable 200000 300000 12% Debenture 200000 100000 Account

Bills payable 80000 100000 Cash 100000 200000 Provision for tax 20000 40000 Receivable 80000 60000

Account payable 300000 200000 Provision for Prepaid

Retained earning 300000 200000 Dividend 10000 20000 Expenses 10000 10000

2100000 1800000 2100000 1800000 Account payable 50000 175000 Cash 20000 50000

Income statement Acc. Depreciation 250000 265000

Sales revenue 12,00,000 Profit and loss a/c - 180000

Less: Cost of goods sold: 700000 1300000 1880000 1300000 1880000

Gross profit 500000

Less: Operating expenses: Income statement for year 5

Depreciation 160000 Sales revenue 10,00,000

Other operating expenses 200000 Less: Cost of goods sold: 300000

Premium on redemption of debenture 20000 380000 700000

Net profit before other income 120000 Wages paid 275000

Add: Profit on sale of plant (Book value 40000) 20000 Gross profit 425000

140000 Less: Operating expenses:

Less: Dividend paid 40000 Administrative expenses 136000

Retained profit 100000 Depreciation 35000

Required: Provision for tax 40000

d. Cash flow statement using direct approach Provision for dividend 20000

(Ans: CFOA = Rs. 380000; CFIA = Rs. (540000); CFFA = Rs. 60000 Interest paid 24000

e. Comment each of the components of a cash flows statement. Premium on redemption of debenture 5000

f. As a financial manager of this company, how do you comment about this Total Operation expenses 260000

company? Net profit 165000

Add: Gain on sale of Fixed assets 15000

Retained profit 180000

Additional information

A plant costing Rs. 40000 with an accumulated depreciation of Rs. 20000 has been

sold for Rs. 35000.

Dividend paid in year 2 is Rs. 10000

Required:

g. Cash flow statement using direct approach

(Ans: CFOA = Rs. 360000; CFIA = Rs. (545000); CFFA = Rs. 215000)

h. Comment each of the components of a cash flows statement.

i. As a financial manager of this company, how do you comment about this

company?

� Cash flow statement (Indirect Method)

8. The balance sheet of a company for the past two years are:

6. Following are the balance sheets of a company as on 31st Chaitra Liabilities Year I Year II Assets Year I Year II

Liabilities Year I Year II Assets Year I Year II Share capital 500000 700000 Land & building (cost) 300000 300000

Share capital 400000 400000 Plant and equipment 240000 400000 Share premium 50000 70000 Plant and machine 360000 630000

Retained Earning 116000 178000 Prepaid expenses 2000 3000 10% Debenture 100000 50000 Trade investment 40000 --------

Sundry Creditors 48000 80000 Marketable Securities 88000 ------- Bank overdraft 50000 100000 Inventories 150000 150000

Accumulated Dep. 80000 108000 Inventories 156000 208000 Account payable 100000 80000 Account receivable 100000 150000

Sundry Debtors 64000 76000 Provision for tax 50000 60000 Cash at bank 50000 70000

Cash 40000 28000 Provision for dividend 50000 70000

Patents 54000 51000 Retained earnings 100000 170000

644000 766000 644000 766000 1000000 1300000 1000000 1300000

Additional information: Additional information:

a. Net income for the period was Rs. 100000 Depreciation on plant and machinery were written off by Rs. 70000. Company paid

b. Dividend declared were Rs. 38000 dividend and taxation of Rs. 50000 each during the period two. Trade investments

c. The marketable securities were sold at a gain of Rs. 12000 were sold for Rs. 80000 and the profit realized was credited to profit and loss

d. Equipment with an original cost of Rs. 16000 and accumulated depreciation account. A premium of 10% was paid to debenture holders at the time of redemption

of Rs. 8000 was sold at on ordinary loss of Rs. 1600 of debenture debts.

CFOA: 107600, CFIA: (169600), CFFA: (38000) CFOA: Rs. 165000, CFIA, Rs. (260000), CFFA: Rs. 115000

9. The balance sheet and related changes on it have been presented below:

7. Following are the balance sheet of a company as on 31st Chaitra

Liabilities Last yr. Inc/Dec Assets Last yr. Inc/Dec

Liabilities Year I Year II Assets Year I Year II Share capital 500000 100000 Land and building 300000 ---------

Share capital 1000000 1200000 Fixed assets 1200000 1400000 Share premium 100000 20000 Plant and machinery 300000 100000

Share premium 200000 240000 Investments 200000 100000 10% Debenture 100000 (50000) Investments 100000 (50000)

10% debenture 200000 100000 Cash 100000 200000 Bills payable 50000 (30000) Cash at bank 50000 50000

Bills payable 300000 340000 Inventories 200000 140000 Account payable 100000 50000 Inventory 100000 (30000)

Retained earnings 100000 200000 Account receivable 100000 240000 Retained 50000 50000 Account receivable 50000 70000

1800000 2080000 1800000 2080000 earnings

900000 900000

Additional information:

Additional information:

Net profit during the year Rs. 160000 a. The company made a profit of Rs. 80000 after charging depreciation

Depreciation on fixed assets Rs. 60000

of Rs. 60000 on plant and machine.

A part of fixed assets (Book value Rs. 100000)

Sold for Rs. 50000 b. A machine costing Rs. 50000 with an accumulated depreciation of

Investments were sold for Rs. Rs. 120000 Rs. 30000 was sold at Rs. 15000 and the loss was charged to profit

Debentures were redeemed at 10% discount and loss account.

c. Debenture were discharged at a premium 10%

Ans: CFOA: Rs. 200000 CFIA: Rs. (190000) CFFA: Rs. 90000 d. Investments were sold for Rs. 60000

Ans: CFOA: Rs. 120000 CFIA: Rs. (105000) CFFA: Rs.35000

� Furniture 50000 20000

Additional information:

Depreciation of Rs. 25000 was charged on plant and machinery during

Basic Problems of cash flow statement the year

1. The following information is provided to you. Land and building were sold at profit of Rs. 10000

Particulars Year I Year II Furniture sold at a loss of Rs. 5000

Sundry debtors Rs. 50000 Rs. 60000 Purchase of plant Rs. 125000

Bills receivables Rs. 30000 Rs. 15000 Required: Cash from investment activities. (Ans: 120000)

Sales Rs. 500000

Required: Cash collection from customer

6. The following items were extracted from the balance sheet of Moonrise

2. The following information is provided to you by a company company

Particulars Year 2014 Year 2015 Assets Year I Year II

Account receivable Rs. 150000 Rs. 200000 Plant and machinery 400000 450000

Bills receivable 50000 60000 Accumulated depreciation (40000) (60000)

Provision for doubtful debt 2000 4000 6% Investment 60000 40000

Bad debt 30000 Land and building 150000 200000

Cash sales 200000 Furniture 30000 20000

Credit sales 150000 Additional information:

Sales return 5000 A Part of plant and machinery costing Rs. 75000 with accumulated

Discount allowed 5000 depreciation of Rs. 10000 was sold for Rs. 50000

Required: Cash collection from customer (Ans: 252000) Investment sold at loss of Rs. 2000

Furniture sold at a profit of Rs. 5000

3. The following information has been extracted from the books of a company Plan and machinery purchased during the year Rs. 125000

Particulars 2071 2072 Required: Cash from investment activities. (Ans: 92000)

Sundry creditors Rs. 50000 Rs. 30000

Bills payable Rs. 70000 Rs. 40000 7. The following items were extracted from the balance sheet of Moonrise

Inventory//stock 100000 150000 company

Cost of goods sold 400000 Assets 2015 2016

Required: Cash paid to suppliers for the year 2072 Share capital 200000 300000

15% debenture 100000 60000

4. The following information has been provided by a company. 6% preference share 55000 35000

Inventory at the beginning Rs. 50000 Retained earning 40000 75000

Cash purchase Rs. 250000 Share premium 20000 30000

Purchase return Rs. 25000 Additional information:

Account payable beginning Rs. 20000 Net profit for the year was Rs. 65000 and dividend paid during the year

Inventory at the end Rs. 70000 was Rs. 30000

Credit purchase Rs. 50000 Required: Cash from financing activities. (Ans: 20000)

Discount received Rs. 10000

Account payable ending Rs. 30000

Required: Cash paid to suppliers (Ans: 255000)

5. The following items were extracted from the balance sheet of Sunrise company

Assets Year I Year II

Plant and machinery 500000 600000

Investment 160000 240000

Land and building 350000 300000