You might also like

- 10 Commandments of Option Trading For Income PDFDocument31 pages10 Commandments of Option Trading For Income PDFGaro OhanogluNo ratings yet

- 22 Power of Ideas Term Sheet EssentialsDocument1 page22 Power of Ideas Term Sheet Essentialssantosh kumar pandaNo ratings yet

- Regulatory framework for business transactions and corporate voting requirementsDocument2 pagesRegulatory framework for business transactions and corporate voting requirementsMarissaNo ratings yet

- Expected Credit LossDocument6 pagesExpected Credit Losstunlinoo.067433No ratings yet

- Harrison FA IFRS 11e CH06 SMDocument86 pagesHarrison FA IFRS 11e CH06 SMJingjing ZhuNo ratings yet

- Enterprise Risk ManagementDocument14 pagesEnterprise Risk Managementsophiawright008100% (2)

- ABM II KEY CORRECTIONSDocument4 pagesABM II KEY CORRECTIONSJomar Villena100% (1)

- Revision Questions XiiDocument11 pagesRevision Questions XiiSahej Kaur AroraNo ratings yet

- Problem Set of Cash Flow StatementDocument1 pageProblem Set of Cash Flow StatementpriyankaNo ratings yet

- Cash Flow Statement of AmulDocument6 pagesCash Flow Statement of AmulArav Sarin60% (5)

- Cash Flow ProbDocument3 pagesCash Flow Probbimbee 13No ratings yet

- DocumentDocument4 pagesDocumentTûshar ThakúrNo ratings yet

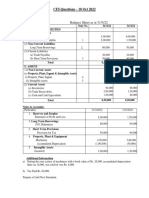

- CFS Questions - 18 - OCT - 2022Document5 pagesCFS Questions - 18 - OCT - 2022Kartik SujanNo ratings yet

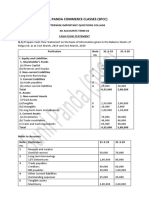

- Cash Flow Statement Collage SPCC Term 2 PDFDocument11 pagesCash Flow Statement Collage SPCC Term 2 PDFTaaran ReddyNo ratings yet

- Accounting concepts and statutory auditDocument4 pagesAccounting concepts and statutory auditNamrata RamgadeNo ratings yet

- 9 Consolidated Financial StatementsDocument20 pages9 Consolidated Financial StatementsArpan SinghNo ratings yet

- Internal ReconstructionDocument26 pagesInternal ReconstructionRajesh NangaliaNo ratings yet

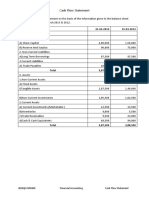

- Cash Flow Statement - 2Document9 pagesCash Flow Statement - 2Midhun PerozhiNo ratings yet

- Cash Flow Statement Xtra Qns Raja Ma'am RecDocument8 pagesCash Flow Statement Xtra Qns Raja Ma'am RecReedhima SrivastavaNo ratings yet

- AFM Assignment 2021Document7 pagesAFM Assignment 2021NARENDRA PATTELANo ratings yet

- Accountancy Board Practical Paper - 2020-2021 Class - Xii Time: 1 Hour Max. Marks: 12Document3 pagesAccountancy Board Practical Paper - 2020-2021 Class - Xii Time: 1 Hour Max. Marks: 12Kairav KhuranaNo ratings yet

- 12 Acs (S) - Set A 19.7.2021Document3 pages12 Acs (S) - Set A 19.7.2021Sakshi NagotkarNo ratings yet

- 12 Accountancy Notes CH12 Cash Flow Statement 02Document28 pages12 Accountancy Notes CH12 Cash Flow Statement 02Gourab GoraiNo ratings yet

- Proposed DividebdDocument34 pagesProposed DividebdPiyush SrivastavaNo ratings yet

- Additional Questions 5Document13 pagesAdditional Questions 5Sanjay SiddharthNo ratings yet

- Solution:: Equity and LiabilitiesDocument4 pagesSolution:: Equity and LiabilitiesNIMROD MOCHAHARINo ratings yet

- Acc Practical QuestionsDocument6 pagesAcc Practical QuestionsyogochkeNo ratings yet

- Cash Flow Statement: Particular 31-03-2013 31-03-2012Document2 pagesCash Flow Statement: Particular 31-03-2013 31-03-2012bimbee 13No ratings yet

- Cash Flow Statement TestDocument2 pagesCash Flow Statement TestHitesh SemwalNo ratings yet

- Accounting for Managers: Cash Budget and Financial StatementsDocument4 pagesAccounting for Managers: Cash Budget and Financial StatementsyogeshgharpureNo ratings yet

- Class 12 Accountancy CBSE Cash Flow StatementDocument7 pagesClass 12 Accountancy CBSE Cash Flow StatementSarvesh SreedharNo ratings yet

- Adobe Scan 05 Mar 2022Document5 pagesAdobe Scan 05 Mar 2022Titiksha Joshi100% (1)

- Adobe Scan 02 Nov 2023Document2 pagesAdobe Scan 02 Nov 2023umangchh2306No ratings yet

- Accounts Important Questions by Rajat Jain SirDocument31 pagesAccounts Important Questions by Rajat Jain SirRajiv JhaNo ratings yet

- Cash Flow Statement for John & Joe LtdDocument4 pagesCash Flow Statement for John & Joe LtdSanjayNo ratings yet

- Ratio Analysis Ex 1Document2 pagesRatio Analysis Ex 1dZOAVIT GamingNo ratings yet

- Cash Flow Statement Activity Wise 05-02-24Document7 pagesCash Flow Statement Activity Wise 05-02-24navyabindra28No ratings yet

- Screenshot 2023-09-20 at 11.30.51 AMDocument1 pageScreenshot 2023-09-20 at 11.30.51 AMprince bhatiaNo ratings yet

- CBCS BCOM GENERAL Sem-5 COMMERCE DSE-5.2-A CORPORATE-ACCOUNTING-10988Document12 pagesCBCS BCOM GENERAL Sem-5 COMMERCE DSE-5.2-A CORPORATE-ACCOUNTING-10988Sayantan DebnathNo ratings yet

- PART-B Analysis Test YtDocument8 pagesPART-B Analysis Test YtRiddhi GuptaNo ratings yet

- 1 Financial Statements of CompaniesDocument21 pages1 Financial Statements of CompaniesShivaram ShivaramNo ratings yet

- Imp QuestionDocument5 pagesImp QuestionKrish PaganiNo ratings yet

- Important QuestionsDocument3 pagesImportant QuestionsNayan JainNo ratings yet

- Q.1) From The Following Balance Sheet of Kiero Ltd. and The Additional Information As On 31-3-2018 Prepare A Cash Flow StatementDocument5 pagesQ.1) From The Following Balance Sheet of Kiero Ltd. and The Additional Information As On 31-3-2018 Prepare A Cash Flow StatementNoor SehgalNo ratings yet

- Adobe Scan Jan 30, 2023Document6 pagesAdobe Scan Jan 30, 2023Karan RajakNo ratings yet

- Accounting For Holding Co. (Lecture 3) : Total 12,00,000 6,00,000Document6 pagesAccounting For Holding Co. (Lecture 3) : Total 12,00,000 6,00,000Michael JimNo ratings yet

- 3 Solution Q.5Document4 pages3 Solution Q.5Aayush AgrawalNo ratings yet

- Additional Illustrations-5Document19 pagesAdditional Illustrations-5goyalmanasvi06No ratings yet

- DB Renews Private Limited: Provisionalbalance Sheet As at 31stmarch, 2019Document8 pagesDB Renews Private Limited: Provisionalbalance Sheet As at 31stmarch, 2019Anonymous btsj64wRNo ratings yet

- First Model Test Paper Part - B Time: 40 Minutes Accountancy M.M. 20Document2 pagesFirst Model Test Paper Part - B Time: 40 Minutes Accountancy M.M. 20surbhi singhalNo ratings yet

- Cash Flow Statement Numericals QDocument3 pagesCash Flow Statement Numericals QDheeraj BholaNo ratings yet

- Current Assets and Current Liabilities 2Document3 pagesCurrent Assets and Current Liabilities 2Jasmine Ahmed Joty (161011023)No ratings yet

- Sums On Cash Flow StatementDocument5 pagesSums On Cash Flow StatementAstha ParmanandkaNo ratings yet

- Solution 18preparation of Financial Statements Company Final AccDocument2 pagesSolution 18preparation of Financial Statements Company Final AccKajal BindalNo ratings yet

- Preparation of Financial Statements - QBDocument26 pagesPreparation of Financial Statements - QBHindutav arya100% (1)

- 232 FM AssignmentDocument17 pages232 FM Assignmentbhupesh joshiNo ratings yet

- Net Working Capital Current Assets - Current LiabilitiesDocument11 pagesNet Working Capital Current Assets - Current LiabilitiesRahul YadavNo ratings yet

- 12th cbse accounts paper 10 06 2017Document2 pages12th cbse accounts paper 10 06 2017Harpreet Singh SainiNo ratings yet

- Particulars Note No. 31 Mar, 2020 31 Mar, 2019: ST STDocument5 pagesParticulars Note No. 31 Mar, 2020 31 Mar, 2019: ST STAmit sinhaNo ratings yet

- 2021 Business AccountingDocument5 pages2021 Business AccountingVISHESH 0009No ratings yet

- Unit II Analysis and Interpretation of Financial Statements Vertical Balance Sheet Balance Sheet As On 31/3/2022 Liabilities Rs. Assets RsDocument9 pagesUnit II Analysis and Interpretation of Financial Statements Vertical Balance Sheet Balance Sheet As On 31/3/2022 Liabilities Rs. Assets RsKirti RawatNo ratings yet

- MTP Corporate Financial ReportingDocument24 pagesMTP Corporate Financial ReportingI'm Just FunnyNo ratings yet

- EXERCISE Cashflow of The CompanyDocument41 pagesEXERCISE Cashflow of The CompanyDev lakhaniNo ratings yet

- Performa of Balance SheetDocument2 pagesPerforma of Balance SheetAman hingoraniNo ratings yet

- COMPARATIVE INCOME STATEMENTDocument12 pagesCOMPARATIVE INCOME STATEMENTBISHAL ROYNo ratings yet

- Adobe Scan 10-Jan-2024Document7 pagesAdobe Scan 10-Jan-2024zishanarjunNo ratings yet

- The Basic Tools of Finance QuizDocument4 pagesThe Basic Tools of Finance QuizMinh Châu Tạ ThịNo ratings yet

- Financial Analysis Definition GuideDocument2 pagesFinancial Analysis Definition GuideKumarNo ratings yet

- Acc 223 CB PS3 AkDocument19 pagesAcc 223 CB PS3 AkAeyjay ManangaranNo ratings yet

- History of Accounting Rex VillanuevaDocument3 pagesHistory of Accounting Rex Villanuevalgucabugao treasuryNo ratings yet

- Growth of Corporation Occurs Through 1. Internal Expansion That Is Growth 2. MergersDocument8 pagesGrowth of Corporation Occurs Through 1. Internal Expansion That Is Growth 2. MergersFazul Rehman100% (1)

- Capital Asset Pricing Mode1Document9 pagesCapital Asset Pricing Mode1Shaloo SidhuNo ratings yet

- HDFC Hybrid Equity Fund: Scheme Information DocumentDocument108 pagesHDFC Hybrid Equity Fund: Scheme Information DocumentRadhika SarawagiNo ratings yet

- Suggested Solutions To Practical ExercisesDocument38 pagesSuggested Solutions To Practical ExercisesDavidNo ratings yet

- Module 3 Principles of Accounting 2Document25 pagesModule 3 Principles of Accounting 2Phoebe Jane AbrahamNo ratings yet

- BCG Consulting Task 1Document1 pageBCG Consulting Task 1Simon RydNo ratings yet

- IFRS 9 - Financial Instruments: Search Site..Document3 pagesIFRS 9 - Financial Instruments: Search Site..kæsiiiNo ratings yet

- Solving Some Numerical QuestionsDocument9 pagesSolving Some Numerical QuestionsVEDANT BASNYATNo ratings yet

- Long-Term Debt and Lease Financing: SixteenDocument19 pagesLong-Term Debt and Lease Financing: SixteenNassir CeellaabeNo ratings yet

- Morningstar Report-636d1778e26a17cb57991bbfDocument24 pagesMorningstar Report-636d1778e26a17cb57991bbfdantulo1234No ratings yet

- FinalDocument46 pagesFinalSiddharth DasNo ratings yet

- Investment HomeworkDocument26 pagesInvestment HomeworkĐức HoàngNo ratings yet

- Beams Aa13e PPT 13Document36 pagesBeams Aa13e PPT 13ki100% (1)

- Assignment - DRM Given By: Mr. N P Singh: 1. Interest Rate SwapDocument3 pagesAssignment - DRM Given By: Mr. N P Singh: 1. Interest Rate SwapSahil MittalNo ratings yet

- Securities and Exchange Commission (SEC) by Towhidul AlamDocument11 pagesSecurities and Exchange Commission (SEC) by Towhidul AlamTowhidul Alam Pavel0% (1)

- Ey BRC GuidelineDocument24 pagesEy BRC GuidelineSteven AndersonNo ratings yet

- Chapter - 1 & 2 (Presentations On Introduction To Accounting & The Accounting Equation)Document52 pagesChapter - 1 & 2 (Presentations On Introduction To Accounting & The Accounting Equation)Sattaki RoyNo ratings yet

- Security Analysis and Portfolio Management Prof: C.S. Mishra Department of VGSOM Indian Institute of Technology, KharagpurDocument29 pagesSecurity Analysis and Portfolio Management Prof: C.S. Mishra Department of VGSOM Indian Institute of Technology, KharagpurviswanathNo ratings yet

- FM Unit 6Document9 pagesFM Unit 6bookabdi1No ratings yet