You might also like

- Intermediate Accounting By: Valix SOLUTION MANUAL 2020 EditionDocument19 pagesIntermediate Accounting By: Valix SOLUTION MANUAL 2020 EditionJoyce Anne Garduque100% (1)

- The Tier 4 Microfinance Institutions and Money Lenders Money Lenders RegulationDocument26 pagesThe Tier 4 Microfinance Institutions and Money Lenders Money Lenders RegulationCHARLES ODOKI OKELLANo ratings yet

- Contract of Sale: Franklin Lopez Accounting Education Department Rmmc-MiDocument14 pagesContract of Sale: Franklin Lopez Accounting Education Department Rmmc-MiRazel Tercino100% (2)

- TIA 2/FM Seminar A.1 ProblemsDocument23 pagesTIA 2/FM Seminar A.1 ProblemsPrisco SayNo ratings yet

- First Model Test Paper Part - B Time: 40 Minutes Accountancy M.M. 20Document2 pagesFirst Model Test Paper Part - B Time: 40 Minutes Accountancy M.M. 20surbhi singhalNo ratings yet

- Accountancy Board Practical Paper - 2020-2021 Class - Xii Time: 1 Hour Max. Marks: 12Document3 pagesAccountancy Board Practical Paper - 2020-2021 Class - Xii Time: 1 Hour Max. Marks: 12Kairav KhuranaNo ratings yet

- Financial Reporting & Financial Statement Analysis Paper - Dse 6.1A FM - 80 Group - A (5x3 15)Document5 pagesFinancial Reporting & Financial Statement Analysis Paper - Dse 6.1A FM - 80 Group - A (5x3 15)tanmoy sardarNo ratings yet

- Solution:: Equity and LiabilitiesDocument4 pagesSolution:: Equity and LiabilitiesNIMROD MOCHAHARINo ratings yet

- Important QuestionsDocument3 pagesImportant QuestionsNayan JainNo ratings yet

- Cash Flow Statement Collage SPCC Term 2 PDFDocument11 pagesCash Flow Statement Collage SPCC Term 2 PDFTaaran ReddyNo ratings yet

- Adobe Scan 19 Mar 2024Document5 pagesAdobe Scan 19 Mar 2024anilarsha18No ratings yet

- Proposed DividebdDocument34 pagesProposed DividebdPiyush SrivastavaNo ratings yet

- Additional Illustrations-5Document19 pagesAdditional Illustrations-5goyalmanasvi06No ratings yet

- AFM Assignment 2021Document7 pagesAFM Assignment 2021NARENDRA PATTELANo ratings yet

- CMA Final CFR MarathonDocument30 pagesCMA Final CFR MarathonRamanpreet KaurNo ratings yet

- Accounts DDocument13 pagesAccounts DRahit MitraNo ratings yet

- Preparation of Financial Statements - QBDocument26 pagesPreparation of Financial Statements - QBHindutav arya100% (1)

- Accounting concepts and statutory auditDocument4 pagesAccounting concepts and statutory auditNamrata RamgadeNo ratings yet

- Cash Flow Statement for John & Joe LtdDocument4 pagesCash Flow Statement for John & Joe LtdSanjayNo ratings yet

- Additional Questions 5Document13 pagesAdditional Questions 5Sanjay SiddharthNo ratings yet

- Cash Flow Statement - 2Document9 pagesCash Flow Statement - 2Midhun PerozhiNo ratings yet

- IPS Academy, IBMR Session Jan-June 2020 BBA II Semester: Assignment Of: Financial ManagementDocument6 pagesIPS Academy, IBMR Session Jan-June 2020 BBA II Semester: Assignment Of: Financial ManagementDrShailesh Singh ThakurNo ratings yet

- Master Questions, Advance Level Questions and Additional Questions-Chapter 4Document18 pagesMaster Questions, Advance Level Questions and Additional Questions-Chapter 4manmeet0001No ratings yet

- EXERCISE Cashflow of The CompanyDocument41 pagesEXERCISE Cashflow of The CompanyDev lakhaniNo ratings yet

- CFS 2023 PyqDocument15 pagesCFS 2023 PyqAnshul JainNo ratings yet

- Accounts Important Questions by Rajat Jain SirDocument31 pagesAccounts Important Questions by Rajat Jain SirRajiv JhaNo ratings yet

- Cash Flow Statement Activity Wise 05-02-24Document7 pagesCash Flow Statement Activity Wise 05-02-24navyabindra28No ratings yet

- Cash Flow StatementDocument19 pagesCash Flow StatementROHIT SHANo ratings yet

- Management Accouting Assignment4 Manish Chauhan (09-1128) .Document17 pagesManagement Accouting Assignment4 Manish Chauhan (09-1128) .manishNo ratings yet

- 12 Accountancy Notes CH12 Cash Flow Statement 02Document28 pages12 Accountancy Notes CH12 Cash Flow Statement 02Gourab GoraiNo ratings yet

- Accounting for Managers: Cash Budget and Financial StatementsDocument4 pagesAccounting for Managers: Cash Budget and Financial StatementsyogeshgharpureNo ratings yet

- Revision Questions XiiDocument11 pagesRevision Questions XiiSahej Kaur AroraNo ratings yet

- DocumentDocument4 pagesDocumentTûshar ThakúrNo ratings yet

- 232 FM AssignmentDocument17 pages232 FM Assignmentbhupesh joshiNo ratings yet

- Accounts AIP FINALDocument14 pagesAccounts AIP FINALManthanNo ratings yet

- Consolidated Balance Sheet of Hold and SubDocument31 pagesConsolidated Balance Sheet of Hold and SubRahul NandurkarNo ratings yet

- 1001 Practice QuestionsDocument95 pages1001 Practice QuestionsMohamad El-JadayelNo ratings yet

- CAFM FULL SYLLABUS FREE TEST DEC 23-Executive-RevisionDocument7 pagesCAFM FULL SYLLABUS FREE TEST DEC 23-Executive-Revisionyogeetha saiNo ratings yet

- Worksheet-4 On CFSDocument6 pagesWorksheet-4 On CFSNavya KhemkaNo ratings yet

- Dabur Segment Revenue and Profit AnalysisDocument29 pagesDabur Segment Revenue and Profit AnalysisazeemNo ratings yet

- Unit IIIDocument9 pagesUnit IIIkuselvNo ratings yet

- Sums On Cash Flow StatementDocument5 pagesSums On Cash Flow StatementAstha ParmanandkaNo ratings yet

- Particulars Debit Credit: © The Institute of Chartered Accountants of IndiaDocument46 pagesParticulars Debit Credit: © The Institute of Chartered Accountants of IndiaOveyaaNo ratings yet

- Class 12 Accountancy CBSE Cash Flow StatementDocument7 pagesClass 12 Accountancy CBSE Cash Flow StatementSarvesh SreedharNo ratings yet

- Analysis of Financial StatementDocument23 pagesAnalysis of Financial StatementMohammad Tariq AnsariNo ratings yet

- Adobe Scan 05 Mar 2022Document5 pagesAdobe Scan 05 Mar 2022Titiksha Joshi100% (1)

- Q.1) From The Following Balance Sheet of Kiero Ltd. and The Additional Information As On 31-3-2018 Prepare A Cash Flow StatementDocument5 pagesQ.1) From The Following Balance Sheet of Kiero Ltd. and The Additional Information As On 31-3-2018 Prepare A Cash Flow StatementNoor SehgalNo ratings yet

- QP CODE: 22100973: Reg No: NameDocument6 pagesQP CODE: 22100973: Reg No: NameSajithaNo ratings yet

- Tutorial On Ratio AnalysisDocument4 pagesTutorial On Ratio AnalysisRajyaLakshmiNo ratings yet

- Management Accounitng - 104 (I)Document4 pagesManagement Accounitng - 104 (I)Rudraksh PareyNo ratings yet

- Isc Mock 2Document14 pagesIsc Mock 2anshikajain3474No ratings yet

- Cash Flow Statement of AmulDocument6 pagesCash Flow Statement of AmulArav Sarin60% (5)

- Problems Set On Ratio AnalysisDocument7 pagesProblems Set On Ratio AnalysispriyankaNo ratings yet

- CASH FLOW 2024 SPCCDocument54 pagesCASH FLOW 2024 SPCCTCPS UNFILTEREDNo ratings yet

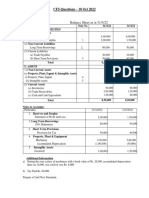

- CFS Questions - 18 - OCT - 2022Document5 pagesCFS Questions - 18 - OCT - 2022Kartik SujanNo ratings yet

- 12 DRT AccDocument2 pages12 DRT AccDeeran DhayanithiRPNo ratings yet

- CR Assignemt Unit 3Document25 pagesCR Assignemt Unit 3Calida SoaresNo ratings yet

- Valuation of GoodwillDocument15 pagesValuation of Goodwillbtsa1262013No ratings yet

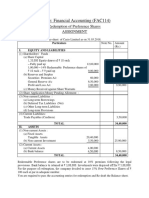

- FAC114 Financial Accounting Redemption of Preference SharesDocument4 pagesFAC114 Financial Accounting Redemption of Preference SharesDhairya ShahNo ratings yet

- ACMA Unit 5 Problems - CFS PDFDocument3 pagesACMA Unit 5 Problems - CFS PDFPrabhat SinghNo ratings yet

- 1 Financial Statements of CompaniesDocument21 pages1 Financial Statements of CompaniesShivaram ShivaramNo ratings yet

- Test - Section B - Corporate AccountingDocument3 pagesTest - Section B - Corporate AccountingNathoNo ratings yet

- General Instructions: All The Questions Are CompulsoryDocument2 pagesGeneral Instructions: All The Questions Are CompulsoryJatin ChaudharyNo ratings yet

- Bank Credit Instruments-Fm122Document27 pagesBank Credit Instruments-Fm122Jade Solante Cervantes100% (1)

- Closing and Worksheet: 20.1 Closing Entries For Revenue AccountsDocument8 pagesClosing and Worksheet: 20.1 Closing Entries For Revenue AccountsZaheer Swati100% (1)

- 2016SEC Form CPIS PDFDocument3 pages2016SEC Form CPIS PDFAndrewJosephBarciaCruzNo ratings yet

- Bad & Provision For Bad Debt HandoutDocument10 pagesBad & Provision For Bad Debt HandoutDajueNo ratings yet

- 1 Semester, 2014/2015 Examination Fin 210: Introduction To Finance Time Allowed 90 Minutes Use For Questions 1 To 5Document22 pages1 Semester, 2014/2015 Examination Fin 210: Introduction To Finance Time Allowed 90 Minutes Use For Questions 1 To 5Daniel AdegboyeNo ratings yet

- J B Gupta Classes: Lease Decisions Lease Decisions Lease Decisions Lease DecisionsDocument51 pagesJ B Gupta Classes: Lease Decisions Lease Decisions Lease Decisions Lease DecisionsTihor LuharNo ratings yet

- Direct Method Cash Flow Statement for PickUp BhdDocument5 pagesDirect Method Cash Flow Statement for PickUp BhdIR WanNo ratings yet

- NCC Bank RatiosDocument20 pagesNCC Bank RatiosRahnoma Bilkis NavaidNo ratings yet

- Acc - No Account Name Debit KreditDocument3 pagesAcc - No Account Name Debit KreditNofi NurlailaNo ratings yet

- 2502201913-Aditya Pratap SinghDocument5 pages2502201913-Aditya Pratap SinghAjay SinghNo ratings yet

- Maturity Instruction: Payment Instruction (Maturity Proceeds/Residual)Document1 pageMaturity Instruction: Payment Instruction (Maturity Proceeds/Residual)Dr. Gollapalli NareshNo ratings yet

- Upkeep Services: Ramsons Plaza 95, Sector-95, Gurgaon-122505, HaryanaDocument1 pageUpkeep Services: Ramsons Plaza 95, Sector-95, Gurgaon-122505, HaryanaRahul BishnoiNo ratings yet

- Transfer of Property Act ExplainedDocument15 pagesTransfer of Property Act ExplainedrubabshaikhNo ratings yet

- Case StudyDocument5 pagesCase StudyMD FAISALNo ratings yet

- Leverage and Capital StructureDocument65 pagesLeverage and Capital StructureMoieenNo ratings yet

- ACW1120-Week 5 Practice Q-Topic 5-Prepare FSDocument8 pagesACW1120-Week 5 Practice Q-Topic 5-Prepare FSGan ZhengweiNo ratings yet

- Kartik MCQ 1Document4 pagesKartik MCQ 1Sathya SeelanNo ratings yet

- Module 4Document4 pagesModule 4AEKONo ratings yet

- Chapter OneDocument8 pagesChapter Onetasfa zNo ratings yet

- Chaper 4 Completing The Accounting CycleDocument41 pagesChaper 4 Completing The Accounting CycleAssassin ClassroomNo ratings yet

- Understanding Due Dates and NPA ClassificationDocument2 pagesUnderstanding Due Dates and NPA ClassificationAFFII MARKETINGNo ratings yet

- Accounting Ae2020Document3 pagesAccounting Ae2020elsana philipNo ratings yet

- Chương 4 Định Giá Dự Án Đầu Tư Và Doanh Nghiệp Với Đòn Bẩy Tài ChínhDocument10 pagesChương 4 Định Giá Dự Án Đầu Tư Và Doanh Nghiệp Với Đòn Bẩy Tài ChínhThảo NguyênNo ratings yet

- 01 - Financial StatementsDocument6 pages01 - Financial Statementsjoubert andresNo ratings yet

- WRD 27e - SE PPT - Ch02 - ADADocument23 pagesWRD 27e - SE PPT - Ch02 - ADANovrissa DianiNo ratings yet

- Mas 1Document1 pageMas 1Tk KimNo ratings yet