You might also like

- Notes To Margin of SafetyDocument19 pagesNotes To Margin of SafetyTshi21100% (10)

- Accounting Ratio'sDocument26 pagesAccounting Ratio'sRajesh Jyothi100% (1)

- GenMathG11 Q2 Mod8 Basic Concepts of Stocks and Bonds Version2Document25 pagesGenMathG11 Q2 Mod8 Basic Concepts of Stocks and Bonds Version2Glaiza Dalayoan Flores100% (12)

- Tutorial On Ratio AnalysisDocument4 pagesTutorial On Ratio AnalysisRajyaLakshmiNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Limited Liability PartnershipDocument7 pagesLimited Liability PartnershipMaygie KeiNo ratings yet

- Solution:: Equity and LiabilitiesDocument4 pagesSolution:: Equity and LiabilitiesNIMROD MOCHAHARINo ratings yet

- AFM-Assignment-2021: Trial Balance As On 31 March 2015Document1 pageAFM-Assignment-2021: Trial Balance As On 31 March 2015SILLA SAIKUMARNo ratings yet

- PART-B Analysis Test YtDocument8 pagesPART-B Analysis Test YtRiddhi GuptaNo ratings yet

- DocumentDocument4 pagesDocumentTûshar ThakúrNo ratings yet

- Cash Flow Statement Collage SPCC Term 2 PDFDocument11 pagesCash Flow Statement Collage SPCC Term 2 PDFTaaran ReddyNo ratings yet

- Class 12 Accountancy CBSE Cash Flow StatementDocument7 pagesClass 12 Accountancy CBSE Cash Flow StatementSarvesh SreedharNo ratings yet

- Master of Business Administration (M.B.A.) Semester-I (C.B.C.S.) Examination Accounting For Managers Compulsory Paper-3Document4 pagesMaster of Business Administration (M.B.A.) Semester-I (C.B.C.S.) Examination Accounting For Managers Compulsory Paper-3Namrata RamgadeNo ratings yet

- Additional Questions 5Document13 pagesAdditional Questions 5Sanjay SiddharthNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument25 pages© The Institute of Chartered Accountants of IndiacdNo ratings yet

- Sums On Cash Flow StatementDocument5 pagesSums On Cash Flow StatementAstha ParmanandkaNo ratings yet

- 1 Financial Statements of CompaniesDocument21 pages1 Financial Statements of CompaniesShivaram ShivaramNo ratings yet

- 9 Consolidated Financial StatementsDocument20 pages9 Consolidated Financial StatementsArpan SinghNo ratings yet

- 12 Accountancy Notes CH12 Cash Flow Statement 02Document28 pages12 Accountancy Notes CH12 Cash Flow Statement 02Gourab GoraiNo ratings yet

- Cash Flow StatementDocument10 pagesCash Flow Statementvsy9926No ratings yet

- Cash Flow Statement of AmulDocument6 pagesCash Flow Statement of AmulArav Sarin60% (5)

- Cash Flow Statement Test Paper IIDocument2 pagesCash Flow Statement Test Paper IIRaman SachdevaNo ratings yet

- Accountancy Board Practical Paper - 2020-2021 Class - Xii Time: 1 Hour Max. Marks: 12Document3 pagesAccountancy Board Practical Paper - 2020-2021 Class - Xii Time: 1 Hour Max. Marks: 12Kairav KhuranaNo ratings yet

- Proposed DividebdDocument34 pagesProposed DividebdPiyush SrivastavaNo ratings yet

- Cash Flow Statement Activity Wise 05-02-24Document7 pagesCash Flow Statement Activity Wise 05-02-24navyabindra28No ratings yet

- © The Institute of Chartered Accountants of IndiaDocument25 pages© The Institute of Chartered Accountants of IndiaShobhit JalanNo ratings yet

- Fund Flow Statement-FR FSADocument27 pagesFund Flow Statement-FR FSADãrk LïghtNo ratings yet

- FR Suggested May 2018Document31 pagesFR Suggested May 2018Rahul NandurkarNo ratings yet

- Accounting MBA Sem I 2018Document4 pagesAccounting MBA Sem I 2018yogeshgharpureNo ratings yet

- Xii AccDocument4 pagesXii AccSanjayNo ratings yet

- Revision Questions XiiDocument11 pagesRevision Questions XiiSahej Kaur AroraNo ratings yet

- Accounting For Holding Co. (Lecture 3) : Total 12,00,000 6,00,000Document6 pagesAccounting For Holding Co. (Lecture 3) : Total 12,00,000 6,00,000Michael JimNo ratings yet

- CAFM FULL SYLLABUS FREE TEST DEC 23-Executive-RevisionDocument7 pagesCAFM FULL SYLLABUS FREE TEST DEC 23-Executive-Revisionyogeetha saiNo ratings yet

- Additional Illustrations-5Document19 pagesAdditional Illustrations-5goyalmanasvi06No ratings yet

- Problems On Balance Sheet of A Company As Per Revised Schedule VI of The Companies ActDocument7 pagesProblems On Balance Sheet of A Company As Per Revised Schedule VI of The Companies ActNithyananda PatelNo ratings yet

- CMA Final CFR MarathonDocument30 pagesCMA Final CFR MarathonRamanpreet KaurNo ratings yet

- Problem Set of Cash Flow StatementDocument1 pageProblem Set of Cash Flow StatementpriyankaNo ratings yet

- EXERCISE Cashflow of The CompanyDocument41 pagesEXERCISE Cashflow of The CompanyDev lakhaniNo ratings yet

- First Model Test Paper Part - B Time: 40 Minutes Accountancy M.M. 20Document2 pagesFirst Model Test Paper Part - B Time: 40 Minutes Accountancy M.M. 20surbhi singhalNo ratings yet

- Cash Flow ProbDocument3 pagesCash Flow Probbimbee 13No ratings yet

- Cap III Group I RTP Dec 2023Document111 pagesCap III Group I RTP Dec 2023meme.arena786No ratings yet

- Preparation of Financial Statements - QBDocument26 pagesPreparation of Financial Statements - QBHindutav arya100% (1)

- Management Accouting Assignment4 Manish Chauhan (09-1128) .Document17 pagesManagement Accouting Assignment4 Manish Chauhan (09-1128) .manishNo ratings yet

- Imp QuestionDocument5 pagesImp QuestionKrish PaganiNo ratings yet

- Accounts Important Questions by Rajat Jain SirDocument31 pagesAccounts Important Questions by Rajat Jain SirRajiv JhaNo ratings yet

- Accounts DDocument13 pagesAccounts DRahit MitraNo ratings yet

- Accounts ProjectDocument29 pagesAccounts ProjectazeemNo ratings yet

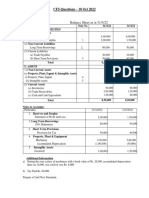

- CFS Questions - 18 - OCT - 2022Document5 pagesCFS Questions - 18 - OCT - 2022Kartik SujanNo ratings yet

- Cash Flow Statement - 2Document9 pagesCash Flow Statement - 2Midhun PerozhiNo ratings yet

- Master Questions, Advance Level Questions and Additional Questions-Chapter 4Document18 pagesMaster Questions, Advance Level Questions and Additional Questions-Chapter 4manmeet0001No ratings yet

- Important QuestionsDocument3 pagesImportant QuestionsNayan JainNo ratings yet

- FR (New) A MTP Final Mar 2021Document17 pagesFR (New) A MTP Final Mar 2021ritz meshNo ratings yet

- 12 DRT AccDocument2 pages12 DRT AccDeeran DhayanithiRPNo ratings yet

- Balance Sheet CompanyDocument16 pagesBalance Sheet CompanyNidhi ShahNo ratings yet

- Acc Practical QuestionsDocument6 pagesAcc Practical QuestionsyogochkeNo ratings yet

- 232 FM AssignmentDocument17 pages232 FM Assignmentbhupesh joshiNo ratings yet

- Test - Section B - Corporate AccountingDocument3 pagesTest - Section B - Corporate AccountingNathoNo ratings yet

- 05 Corporate LiquidationDocument4 pages05 Corporate LiquidationEric CauilanNo ratings yet

- Particulars Debit Credit: © The Institute of Chartered Accountants of IndiaDocument46 pagesParticulars Debit Credit: © The Institute of Chartered Accountants of IndiaOveyaaNo ratings yet

- CBCS BCOM GENERAL Sem-5 COMMERCE DSE-5.2-A CORPORATE-ACCOUNTING-10988Document12 pagesCBCS BCOM GENERAL Sem-5 COMMERCE DSE-5.2-A CORPORATE-ACCOUNTING-10988Sayantan DebnathNo ratings yet

- Cash Flow StatementDocument19 pagesCash Flow StatementROHIT SHANo ratings yet

- Financial Reporting & Financial Statement Analysis Paper - Dse 6.1A FM - 80 Group - A (5x3 15)Document5 pagesFinancial Reporting & Financial Statement Analysis Paper - Dse 6.1A FM - 80 Group - A (5x3 15)tanmoy sardarNo ratings yet

- Clavax Power - TAR - 2023 - Provisional - 10.09Document7 pagesClavax Power - TAR - 2023 - Provisional - 10.09Naresh nath MallickNo ratings yet

- DE - Dirk Bliesener - Hengeler MuellerDocument54 pagesDE - Dirk Bliesener - Hengeler MuellerarohiNo ratings yet

- Annual Report 2017-18 PDFDocument141 pagesAnnual Report 2017-18 PDFAkshitaNo ratings yet

- Ifrs 16 Example Initial Measurement of Right-Of-use Asset and Lease LiabilityDocument4 pagesIfrs 16 Example Initial Measurement of Right-Of-use Asset and Lease Liabilityaldwin006No ratings yet

- STMT 17840200000094 1675686158440Document10 pagesSTMT 17840200000094 1675686158440Rajeev kumar AgarwalNo ratings yet

- Pearsons Federal Taxation 2018 Comprehensive 31st Edition Rupert Test BankDocument45 pagesPearsons Federal Taxation 2018 Comprehensive 31st Edition Rupert Test Bankloanazura7k6bl100% (29)

- Fund FlowDocument21 pagesFund FlowShivangi RaiNo ratings yet

- CIMA Chartered Management Accounting Qualification 2010Document7 pagesCIMA Chartered Management Accounting Qualification 2010lunoguNo ratings yet

- L2 CFA Notes 1Document64 pagesL2 CFA Notes 1simmbNo ratings yet

- A Study On Financial Statement Analysis in HDFC Bank LTD 2013Document85 pagesA Study On Financial Statement Analysis in HDFC Bank LTD 2013Abhirup Ubale100% (1)

- Accounting CyclesDocument11 pagesAccounting CyclesAbdiNo ratings yet

- Chapter 13 - Statement of Cash FlowsDocument165 pagesChapter 13 - Statement of Cash FlowsElio BazNo ratings yet

- What Is Share Capital?: Company Receives Through Their Equity FinancingDocument6 pagesWhat Is Share Capital?: Company Receives Through Their Equity FinancingDominique B. PeronillaNo ratings yet

- Ud Bangunan SaktiDocument18 pagesUd Bangunan SaktiAnonymous FzCL5oNo ratings yet

- Topic: Credit Rating Agencies Section: H and I Year: 3 RD, 6 SemesterDocument29 pagesTopic: Credit Rating Agencies Section: H and I Year: 3 RD, 6 SemesterShama parbinNo ratings yet

- Chapter 4Document52 pagesChapter 4Maharani KumalasariNo ratings yet

- Corporate Finance Report On LegoDocument8 pagesCorporate Finance Report On LegoAnna StoychevaNo ratings yet

- G. S. College of Commerce & Economics, Nagpur: Fundamentals of Accounting StandardsDocument3 pagesG. S. College of Commerce & Economics, Nagpur: Fundamentals of Accounting StandardsRanjhana SahuNo ratings yet

- Preparation of Financial Statement For PublicationDocument21 pagesPreparation of Financial Statement For PublicationRAUDAHNo ratings yet

- RWJ FCF11e Chap 02Document25 pagesRWJ FCF11e Chap 02kaylakshmiNo ratings yet

- IFRS 16 and IAS 36: How Changes in Lease Accounting Will Impact Your Impairment Testing ProcessesDocument4 pagesIFRS 16 and IAS 36: How Changes in Lease Accounting Will Impact Your Impairment Testing ProcessesHamada Asmr Aladham100% (1)

- RAK International Companies Regulations 2006Document85 pagesRAK International Companies Regulations 2006mika095No ratings yet

- Sustainable EnterpreneurshipDocument92 pagesSustainable Enterpreneurshipchukwu solomonNo ratings yet

- HW2Document16 pagesHW2Nevan NovaNo ratings yet

- NFLPA LM-2 - Part2 Player PaymentsaDocument268 pagesNFLPA LM-2 - Part2 Player PaymentsaRobert LeeNo ratings yet

- Tarc Acc t13Document4 pagesTarc Acc t13Shirley VunNo ratings yet

- Introduction To Corporate Finance-Chapter 1Document12 pagesIntroduction To Corporate Finance-Chapter 1Arty MamunNo ratings yet