You might also like

- Cryptrillionaire: A Beginner's Road Map to Generating Wealth with Bitcoin and Other Digital AssetsFrom EverandCryptrillionaire: A Beginner's Road Map to Generating Wealth with Bitcoin and Other Digital AssetsNo ratings yet

- Digital Money Demystified: Go From Cash to Crypto® Safely, Legally, and ConfidentlyFrom EverandDigital Money Demystified: Go From Cash to Crypto® Safely, Legally, and ConfidentlyNo ratings yet

- Before Babylon, Beyond Bitcoin: From Money that We Understand to Money that Understands UsFrom EverandBefore Babylon, Beyond Bitcoin: From Money that We Understand to Money that Understands UsNo ratings yet

- Digital Cash: The Unknown History of the Anarchists, Utopians, and Technologists Who Created CryptocurrencyFrom EverandDigital Cash: The Unknown History of the Anarchists, Utopians, and Technologists Who Created CryptocurrencyRating: 4 out of 5 stars4/5 (9)

- Let's Meet Blockchain: Technology Changing for Working, Creating, and PlayingFrom EverandLet's Meet Blockchain: Technology Changing for Working, Creating, and PlayingNo ratings yet

- Bitcoin for Nonmathematicians:: Exploring the Foundations of Crypto PaymentsFrom EverandBitcoin for Nonmathematicians:: Exploring the Foundations of Crypto PaymentsNo ratings yet

- Attack of the 50 Foot Blockchain: Bitcoin, Blockchain, Ethereum & Smart ContractsFrom EverandAttack of the 50 Foot Blockchain: Bitcoin, Blockchain, Ethereum & Smart ContractsRating: 3.5 out of 5 stars3.5/5 (5)

- Cryptocurrency Investment Handbook: How to Benefit from the Next Big Technology after the InternetFrom EverandCryptocurrency Investment Handbook: How to Benefit from the Next Big Technology after the InternetRating: 4.5 out of 5 stars4.5/5 (3)

- Cryptocurrency 101: Everything You Need to Know About Digital Currencies and Blockchain TechnologyFrom EverandCryptocurrency 101: Everything You Need to Know About Digital Currencies and Blockchain TechnologyNo ratings yet

- Decoding Tomorrow's Currency: An In-Depth Exploration of the Future of CryptocurrencyFrom EverandDecoding Tomorrow's Currency: An In-Depth Exploration of the Future of CryptocurrencyNo ratings yet

- 21st Century Finance for Women: Empowering Women Through CryptocurrencyFrom Everand21st Century Finance for Women: Empowering Women Through CryptocurrencyNo ratings yet

- Crypto Treasure Map: A Guide To Investing In Bitcoin And CryptocurrenciesFrom EverandCrypto Treasure Map: A Guide To Investing In Bitcoin And CryptocurrenciesNo ratings yet

- Mock 15Document13 pagesMock 15Alejandro Rengel BarragánNo ratings yet

- Eview: Book ReviewDocument3 pagesEview: Book ReviewElena AlexandruNo ratings yet

- Cryptocurrencies: Invest Wisely in the Most Profitable and Trusted Cryptocurrencies to Make MoneyFrom EverandCryptocurrencies: Invest Wisely in the Most Profitable and Trusted Cryptocurrencies to Make MoneyNo ratings yet

- Let's Make Some Money - R.MDocument39 pagesLet's Make Some Money - R.MKwame JordanNo ratings yet

- Getting Started with Cryptocurrency: An introduction to digital assets and blockchainFrom EverandGetting Started with Cryptocurrency: An introduction to digital assets and blockchainNo ratings yet

- 21CryptosMagazine 2018august PDFDocument100 pages21CryptosMagazine 2018august PDFhesiluNo ratings yet

- History, Future of NFTsDocument4 pagesHistory, Future of NFTsIshaq GbengaNo ratings yet

- Cryptocurrency Remote Viewed Book Four: Cryptocurrency Remote Viewed, #4From EverandCryptocurrency Remote Viewed Book Four: Cryptocurrency Remote Viewed, #4No ratings yet

- Summary of Easy Money By Ben Mckenzie : Cryptocurrency, Casino Capitalism, and the Golden Age of FraudFrom EverandSummary of Easy Money By Ben Mckenzie : Cryptocurrency, Casino Capitalism, and the Golden Age of FraudNo ratings yet

- Let Them Eat Crypto: The Blockchain Scam That's Ruining the WorldFrom EverandLet Them Eat Crypto: The Blockchain Scam That's Ruining the WorldRating: 5 out of 5 stars5/5 (1)

- Session_12_Reading_2Document11 pagesSession_12_Reading_2Rana AbdullahNo ratings yet

- Crypto Uncovered: The Evolution of Bitcoin and the Crypto Currency MarketplaceFrom EverandCrypto Uncovered: The Evolution of Bitcoin and the Crypto Currency MarketplaceNo ratings yet

- The Only Crypto Story You Need - Sal BayatDocument8 pagesThe Only Crypto Story You Need - Sal BayatA. O. GilmoreNo ratings yet

- The Executive Guide to Blockchain: Using Smart Contracts and Digital Currencies in your BusinessFrom EverandThe Executive Guide to Blockchain: Using Smart Contracts and Digital Currencies in your BusinessNo ratings yet

- Blockchain & Crypto Use Cases 2024Document27 pagesBlockchain & Crypto Use Cases 2024hcsearch0897No ratings yet

- Rugpulls Genesis: Birth of Crypto's Vulnerabilities: Altcoin Pioneers: The Rise of Bitcoin's Competitors: Rugpulls Unveiled: Untangling the Web of Deceit in Early Crypto, #1From EverandRugpulls Genesis: Birth of Crypto's Vulnerabilities: Altcoin Pioneers: The Rise of Bitcoin's Competitors: Rugpulls Unveiled: Untangling the Web of Deceit in Early Crypto, #1No ratings yet

- Money, Magic, and How to Dismantle a Financial Bomb: Quantum Economics for the Real WorldFrom EverandMoney, Magic, and How to Dismantle a Financial Bomb: Quantum Economics for the Real WorldNo ratings yet

- Where Did All the Cash Go? The Digital Money World. Understanding CBDC and Cryptocurrency; Digital Money, Finance, Bitcoin, Crypto, Cryptocurrency, CBDC, Digital Currency, Money BookFrom EverandWhere Did All the Cash Go? The Digital Money World. Understanding CBDC and Cryptocurrency; Digital Money, Finance, Bitcoin, Crypto, Cryptocurrency, CBDC, Digital Currency, Money BookNo ratings yet

- The Sweet Life with Bitcoin: How I Stopped Worrying about Cryptocurrency and You Should Too!From EverandThe Sweet Life with Bitcoin: How I Stopped Worrying about Cryptocurrency and You Should Too!No ratings yet

- The Ultimate Guide to Cryptocurrency: Navigating the World of Digital AssetsFrom EverandThe Ultimate Guide to Cryptocurrency: Navigating the World of Digital AssetsNo ratings yet

- Crypto Millionaire Handbook: A Comprehensive Guide to Cryptocurrency SuccessFrom EverandCrypto Millionaire Handbook: A Comprehensive Guide to Cryptocurrency SuccessNo ratings yet

- Cryptocurrency: Technical OverviewDocument10 pagesCryptocurrency: Technical OverviewnepretipNo ratings yet

- Monero 2Document29 pagesMonero 2Jon AldekoaNo ratings yet

- The Lost and Found GhostsDocument9 pagesThe Lost and Found GhostscimotaNo ratings yet

- The Raise Investment Club: Get Involved TodayDocument1 pageThe Raise Investment Club: Get Involved TodaycimotaNo ratings yet

- Techstart-Funds-Evaluation-Nispo-Impact-Assessment 2Document131 pagesTechstart-Funds-Evaluation-Nispo-Impact-Assessment 2cimotaNo ratings yet

- Iain's Naval GazerDocument3 pagesIain's Naval GazercimotaNo ratings yet

- FurukontakutoDocument9 pagesFurukontakutocimotaNo ratings yet

- Up The Coast OutlineDocument3 pagesUp The Coast OutlinecimotaNo ratings yet

- Performance Business - Assignment 1Document11 pagesPerformance Business - Assignment 1cimotaNo ratings yet

- Nor Gloom of NightDocument19 pagesNor Gloom of NightcimotaNo ratings yet

- Draft Digital StrategyDocument18 pagesDraft Digital StrategycimotaNo ratings yet

- Cancer Girls PostersDocument4 pagesCancer Girls PosterscimotaNo ratings yet

- ZombiDocument65 pagesZombicimotaNo ratings yet

- ZombiDocument65 pagesZombicimotaNo ratings yet

- Electric CarsDocument3 pagesElectric CarscimotaNo ratings yet

- Architect / Contract Administrator's Instruction: Estimated Revised Contract PriceDocument6 pagesArchitect / Contract Administrator's Instruction: Estimated Revised Contract PriceAfiya PatersonNo ratings yet

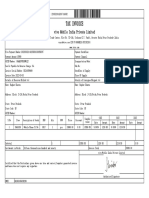

- Tax Invoice: Vivo Mobile India Private LimitedDocument1 pageTax Invoice: Vivo Mobile India Private LimitedRaghav SharmaNo ratings yet

- Microsoft Business Strategy 101Document17 pagesMicrosoft Business Strategy 101Chinmay Chauhan50% (2)

- IRDA Project - Akanksha - LLMDocument9 pagesIRDA Project - Akanksha - LLMPULKIT KHANDELWALNo ratings yet

- Financail Accounting II Frist AssignmentDocument3 pagesFinancail Accounting II Frist AssignmentMuhammad Shahid KhanNo ratings yet

- DocumentDocument1 pageDocumentVanessa GuardadoNo ratings yet

- Suarez, Francis - FORM 1 - 2008 PDFDocument2 pagesSuarez, Francis - FORM 1 - 2008 PDFal_crespoNo ratings yet

- Project InsuranceDocument13 pagesProject InsuranceRohan Raj MishraNo ratings yet

- Lee Mei Peng No 33 Jalan Delima 4A/Ks6 Bandar Parkland Pendamar 41200 KLANGDocument4 pagesLee Mei Peng No 33 Jalan Delima 4A/Ks6 Bandar Parkland Pendamar 41200 KLANGappleNo ratings yet

- Muzammil Qadeer Qureshi Phs Trainee Officer PAY ROLL NO: 21705-0Document25 pagesMuzammil Qadeer Qureshi Phs Trainee Officer PAY ROLL NO: 21705-0Muzammil QureshiiNo ratings yet

- Advanced Bank MamagementDocument43 pagesAdvanced Bank MamagementKarur KumarNo ratings yet

- Lululemon Financial AnalysisDocument14 pagesLululemon Financial Analysismrsammy100% (1)

- Quot PerusahaanDocument4 pagesQuot Perusahaanlady MonnNo ratings yet

- HOBA2019QUIZ1MCDocument10 pagesHOBA2019QUIZ1MCjasfNo ratings yet

- 1109021 (1)Document1 page1109021 (1)Cms Stl CmsNo ratings yet

- Characteristic Features of Financial InstrumentsDocument17 pagesCharacteristic Features of Financial Instrumentsmanoranjanpatra93% (15)

- Fr. Emmanuel Lemelson Letter To Congress Regarding LigandDocument9 pagesFr. Emmanuel Lemelson Letter To Congress Regarding LigandamvonaNo ratings yet

- 1 Van de Brug v. Philippine National BankDocument18 pages1 Van de Brug v. Philippine National BankHannah Keziah MoralesNo ratings yet

- Corporate ScorecardDocument36 pagesCorporate Scorecardgkohli79No ratings yet

- BIWS Atlassian 3 Statement Model - VFDocument8 pagesBIWS Atlassian 3 Statement Model - VFJohnny BravoNo ratings yet

- Iligan Institute of Technology: Mindanao State University Iligan CityDocument4 pagesIligan Institute of Technology: Mindanao State University Iligan Citylairah.mananNo ratings yet

- ECON8Document3 pagesECON8DayLe Ferrer AbapoNo ratings yet

- 3 Famous Personalities of The World - AssignmentDocument3 pages3 Famous Personalities of The World - AssignmentWajahat SheikhNo ratings yet

- Cadillac Ventures Inc.: Consolidated Financial Statements May 31, 2007 and 2006Document22 pagesCadillac Ventures Inc.: Consolidated Financial Statements May 31, 2007 and 2006CadVentNo ratings yet

- Capital Budgeting - Risk Analysis: Questions & AnswersDocument5 pagesCapital Budgeting - Risk Analysis: Questions & AnswersAyush BishtNo ratings yet

- What is Repo Rate, Reverse Repo Rate & their ImpactDocument4 pagesWhat is Repo Rate, Reverse Repo Rate & their ImpactRatnakar AletiNo ratings yet

- Partnership Formation GuideDocument5 pagesPartnership Formation GuideABCNo ratings yet

- RECENT AMENDMENTS TO COMPANIES ACT 2013Document39 pagesRECENT AMENDMENTS TO COMPANIES ACT 2013warner313No ratings yet

- The Current State of The Accounting ProfessionDocument2 pagesThe Current State of The Accounting ProfessionYuliana ArceNo ratings yet

- Ejemplo de Analisis Vertical y Horizontal Caso NikeDocument14 pagesEjemplo de Analisis Vertical y Horizontal Caso NikeDiego Blanco CastroNo ratings yet