You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Determinants of Efficiency of Fiji's Commercial Banks: An Empirical Study: 2002-16Document20 pagesDeterminants of Efficiency of Fiji's Commercial Banks: An Empirical Study: 2002-16Rahul ChandNo ratings yet

- National Income StasticsDocument18 pagesNational Income StasticsKudzanai KudziNo ratings yet

- TFA - Chapter 40 - DepreciationDocument6 pagesTFA - Chapter 40 - DepreciationAsi Cas JavNo ratings yet

- Gurukripa's Guideline Answers To Nov 2013 Exam Questions CA Inter (IPC) Group I AccountingDocument14 pagesGurukripa's Guideline Answers To Nov 2013 Exam Questions CA Inter (IPC) Group I AccountingAbhishek ChowdhuryNo ratings yet

- Student Material-U3L2-IncomeDocument95 pagesStudent Material-U3L2-IncomeBrooke GoshornNo ratings yet

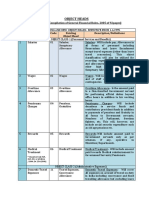

- Object Head List PDFDocument6 pagesObject Head List PDFLal ZahawmaNo ratings yet

- Integrated and Non Integrated Accounting System: Amazing Journey of Logic and ConceptsDocument17 pagesIntegrated and Non Integrated Accounting System: Amazing Journey of Logic and ConceptsSafal BhandariNo ratings yet

- Accounting Research Paper ExampleDocument8 pagesAccounting Research Paper Examplexmniibvkg100% (1)

- Cricket Gloves Out of Waste, REUSE, REDUCE, RECYCLEDocument12 pagesCricket Gloves Out of Waste, REUSE, REDUCE, RECYCLEAmisha NaharNo ratings yet

- Ias 16Document33 pagesIas 16Kiri chris100% (1)

- 25 Edited PRJCTDocument79 pages25 Edited PRJCTMubeenNo ratings yet

- Tax Alert (April 2020) FinalDocument30 pagesTax Alert (April 2020) FinalRheneir MoraNo ratings yet

- Everyday Millionaires: by Chris HoganDocument7 pagesEveryday Millionaires: by Chris HoganDhrithiNo ratings yet

- Mitsubishi Electric Annual ReportDocument21 pagesMitsubishi Electric Annual ReportAbhinavHarshalNo ratings yet

- MAA Sample QPDocument8 pagesMAA Sample QPankitNo ratings yet

- Marriott Corporation (A) Harvard Business School Case 9-394-085 Courseware 9-307-703Document3 pagesMarriott Corporation (A) Harvard Business School Case 9-394-085 Courseware 9-307-703CH NAIR100% (1)

- Tax Rev Income Tax Syllabus With Assignment of CaesesDocument4 pagesTax Rev Income Tax Syllabus With Assignment of CaesesCzarina Joy PenaNo ratings yet

- FAS C2 - Hedging Currency Risk at TT TextilesDocument2 pagesFAS C2 - Hedging Currency Risk at TT TextilesVani SondhiNo ratings yet

- Demetrious Dabadee 08-15-2023-3Document1 pageDemetrious Dabadee 08-15-2023-3Irfan khanNo ratings yet

- Specialized Accounting TechniquesDocument5 pagesSpecialized Accounting TechniquesFridah Apondi100% (1)

- Quizzers 12Document13 pagesQuizzers 12Niña Yna Franchesca PantallaNo ratings yet

- FABM1 Q3 Module-3Document17 pagesFABM1 Q3 Module-3Jillian CuisonNo ratings yet

- CH 3 Job Order CostingDocument87 pagesCH 3 Job Order CostingCool MomNo ratings yet

- Campus Theater Adjusts Its Accounts Every MonthDocument2 pagesCampus Theater Adjusts Its Accounts Every MonthHenock AbyotNo ratings yet

- MBOF912D-Financial Management-Assignment-1Document15 pagesMBOF912D-Financial Management-Assignment-1Utkarsh Singh0% (1)

- lý thuyết cuối kì MNCDocument6 pageslý thuyết cuối kì MNCPhan Minh KhuêNo ratings yet

- Job Costing Question Bank SSDocument6 pagesJob Costing Question Bank SSTamaraNo ratings yet

- 2021 Turbo Tax ReturnDocument4 pages2021 Turbo Tax ReturnEmonee WellsNo ratings yet

- Merchandising OperationsDocument5 pagesMerchandising OperationsGeraldNo ratings yet

- Csec Poa January 2012 p2Document9 pagesCsec Poa January 2012 p2Renelle RampersadNo ratings yet