You might also like

- Trinidad and Tobago National Budget 2022Document60 pagesTrinidad and Tobago National Budget 2022brandon davidNo ratings yet

- Zambia Introduces Fiscal Measures To Mitigate Impact of COVID-19Document4 pagesZambia Introduces Fiscal Measures To Mitigate Impact of COVID-19harryNo ratings yet

- Testing Times Ahead: #Budget 2020Document48 pagesTesting Times Ahead: #Budget 2020DarwinNo ratings yet

- Risk-Based Audit-A Tool For Voluntary Tax ComplianceDocument4 pagesRisk-Based Audit-A Tool For Voluntary Tax ComplianceOmotayo AlabiNo ratings yet

- Internally Generated Revenue Revolution in Kaduna State Nigeria: Emerging Revenue Sources and StrategiesDocument6 pagesInternally Generated Revenue Revolution in Kaduna State Nigeria: Emerging Revenue Sources and StrategiesInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- PWCDocument47 pagesPWCDefimediagroup Ldmg100% (1)

- Laporan Tahunan DJP 2020 - EnglishDocument256 pagesLaporan Tahunan DJP 2020 - EnglishHaryo BagaskaraNo ratings yet

- Finance Act Era Critical Evaluation 1 1Document22 pagesFinance Act Era Critical Evaluation 1 1Folawiyo AgbokeNo ratings yet

- Union Budget 2021Document58 pagesUnion Budget 2021Mexico EnglishNo ratings yet

- The Effect of Liquidity, Leverage and Determined Tax Load On Profitability With Profit Management As Moderating VariablesDocument13 pagesThe Effect of Liquidity, Leverage and Determined Tax Load On Profitability With Profit Management As Moderating VariablesInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- In Tax Budget Expectations NoexpDocument32 pagesIn Tax Budget Expectations NoexpMayurNo ratings yet

- Section 2Document14 pagesSection 2Hafiz TajuddinNo ratings yet

- Taxation of The Digital Economy - Evaluating The Nigerian and Global Approach - Lexology - Alliance Law FirmDocument5 pagesTaxation of The Digital Economy - Evaluating The Nigerian and Global Approach - Lexology - Alliance Law FirmMabruk Kunmi-OlayiwolaNo ratings yet

- Highlights Tax Policy ReformsDocument9 pagesHighlights Tax Policy Reformsvoyager8002No ratings yet

- YojanaMarch2020summary Part11586344521 PDFDocument29 pagesYojanaMarch2020summary Part11586344521 PDFVikin JainNo ratings yet

- Ey Mena Quarterly Banking Report q2 2020Document26 pagesEy Mena Quarterly Banking Report q2 2020Mira Hout100% (1)

- Tax and Business Strategy - Impact of New Ghanaian Tax LawsDocument6 pagesTax and Business Strategy - Impact of New Ghanaian Tax LawsM ArmahNo ratings yet

- Law Number 11 of 2020 Eases Tax BurdenDocument14 pagesLaw Number 11 of 2020 Eases Tax Burdentonitoni27No ratings yet

- Finance Act 2021 - PWC Insight Series and Sector Analysis Interactive 2Document25 pagesFinance Act 2021 - PWC Insight Series and Sector Analysis Interactive 2Oyeleye TofunmiNo ratings yet

- COVID 19: 4 Strategies to Help Businesses Recover from the PandemicDocument16 pagesCOVID 19: 4 Strategies to Help Businesses Recover from the PandemicGilbert LomofioNo ratings yet

- Capital Gains Taxes and Offshore Indirect TransfersDocument30 pagesCapital Gains Taxes and Offshore Indirect TransfersReagan SsebbaaleNo ratings yet

- 002-article-A002-enDocument11 pages002-article-A002-enLaurenNo ratings yet

- 02 OraclDocument12 pages02 OraclJuan Carlos MtzNo ratings yet

- Economic Impact of Relief Package in PakistanDocument10 pagesEconomic Impact of Relief Package in PakistanNadia Farooq100% (1)

- Probable RRLDocument3 pagesProbable RRLCharrey Leigh T. FORMARANNo ratings yet

- Trinidad and Tobago 2022 Budget HighlightsDocument6 pagesTrinidad and Tobago 2022 Budget Highlightsbrandon davidNo ratings yet

- Ken Ofori Atta Finance Statement To Parliament On Domestic Debt ExchangeDocument9 pagesKen Ofori Atta Finance Statement To Parliament On Domestic Debt ExchangeThe Independent GhanaNo ratings yet

- Federal Budget Summary - 1Document23 pagesFederal Budget Summary - 1Osama AtifNo ratings yet

- Kenya's FY 2020/21 Budget Statement focuses on economic stimulusDocument86 pagesKenya's FY 2020/21 Budget Statement focuses on economic stimulusOscar MasindeNo ratings yet

- Taxjournal July 2020Document60 pagesTaxjournal July 2020Venkatesh PrabhuNo ratings yet

- Acquisory News Chronicle September 2020Document8 pagesAcquisory News Chronicle September 2020Acquisory Consulting LLPNo ratings yet

- Budget Highlights - Crowe Nepal (78-79)Document72 pagesBudget Highlights - Crowe Nepal (78-79)binuNo ratings yet

- GRA 2022 Annual ReportDocument85 pagesGRA 2022 Annual ReportKaahwa VivianNo ratings yet

- 2902 10778 1 PBDocument11 pages2902 10778 1 PBOlivia OchaNo ratings yet

- Covid-19 Effect On Tax CollectionDocument7 pagesCovid-19 Effect On Tax Collectionannemorano126No ratings yet

- Treasury's Covid-19 Economic ScenariosDocument16 pagesTreasury's Covid-19 Economic ScenariosHenry Cooke100% (1)

- Strategies of Local Government Units (LGUs) To Improve Business Tax Collections During The Covid-19 PandemicDocument5 pagesStrategies of Local Government Units (LGUs) To Improve Business Tax Collections During The Covid-19 PandemicKomal sharmaNo ratings yet

- National Budget Bulletin 2022 23Document85 pagesNational Budget Bulletin 2022 23Lalit SinghNo ratings yet

- Deloitte Mauritius Covid Measures-Unlocked PDFDocument14 pagesDeloitte Mauritius Covid Measures-Unlocked PDFAvnish BassantNo ratings yet

- Tax Glimpses 2019Document97 pagesTax Glimpses 2019DarshanaNo ratings yet

- Indian BudgetDocument60 pagesIndian BudgetNirav SolankiNo ratings yet

- Namibias-National-Budget-2023_24.pdf-webDocument12 pagesNamibias-National-Budget-2023_24.pdf-webAmogh KothariNo ratings yet

- Nigeria Budget 2012Document6 pagesNigeria Budget 2012Mark allenNo ratings yet

- FinalDocument20 pagesFinalSonam Peldon (Business) [Cohort2020 RTC]No ratings yet

- ATR 3 - 1 - 82-92 - WordDocument11 pagesATR 3 - 1 - 82-92 - WordAkingbesote VictoriaNo ratings yet

- Time_has_come_to_rein_in_spiralling_public_debt___Cape_Times_The_Cape_Town_South_Africa___September_18_2023__p1Document2 pagesTime_has_come_to_rein_in_spiralling_public_debt___Cape_Times_The_Cape_Town_South_Africa___September_18_2023__p1elihlefass0No ratings yet

- Saputra (2022)Document24 pagesSaputra (2022)nita_andriyani030413No ratings yet

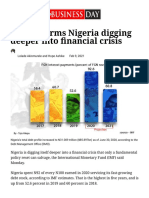

- IMF Confirms Nigeria Digging Deeper Into Financial Crisis - Businessday NGDocument4 pagesIMF Confirms Nigeria Digging Deeper Into Financial Crisis - Businessday NGAnneNo ratings yet

- 2022 Tax Expenditure Report FinalDocument43 pages2022 Tax Expenditure Report FinalKirimi StanleyNo ratings yet

- Concept Paper - Mandanas Ruling and The Lgu's Bigger Budget This Fy 2022Document3 pagesConcept Paper - Mandanas Ruling and The Lgu's Bigger Budget This Fy 2022Analou Agustin Villeza100% (2)

- 220 - PSU - Supporting MSMEs Digitalization Amid COVID-19Document9 pages220 - PSU - Supporting MSMEs Digitalization Amid COVID-19Francis Loie RepuelaNo ratings yet

- Namibia Announces Economic Stimulus PackageDocument4 pagesNamibia Announces Economic Stimulus PackageharryNo ratings yet

- Federal Budget 2020Document15 pagesFederal Budget 2020Muhammad FarazNo ratings yet

- Addressing Pakistan's Economic Challenges Through Budget 2020-21Document9 pagesAddressing Pakistan's Economic Challenges Through Budget 2020-21Asim EhsanNo ratings yet

- SBN 64 Merchant Loan ProgramDocument5 pagesSBN 64 Merchant Loan ProgramJSTNo ratings yet

- Policies To Supports SMEs - Korea - FinalDocument2 pagesPolicies To Supports SMEs - Korea - FinalYasmin AruniNo ratings yet

- MOSELESSON3Document2 pagesMOSELESSON3Sherry MoseNo ratings yet

- Investigacion Final MacroDocument12 pagesInvestigacion Final Macrodaniel servellonNo ratings yet

- Managerial Economics Assessment-2: Model SolutionDocument10 pagesManagerial Economics Assessment-2: Model SolutionR K SinghNo ratings yet

- Nanavati Ventures Limited: TH RDDocument25 pagesNanavati Ventures Limited: TH RDContra Value BetsNo ratings yet

- 01 ABM Financial Accounting Session1Document36 pages01 ABM Financial Accounting Session1DentatusNo ratings yet

- Hand Hygiene Action Plan - Final Draft For IPCGDocument10 pagesHand Hygiene Action Plan - Final Draft For IPCGAnton NaingNo ratings yet

- Chapter One Introduction To Accounting and BusinessDocument16 pagesChapter One Introduction To Accounting and Businessasnfkas100% (1)

- SPP Back Architional PDFDocument8 pagesSPP Back Architional PDFROMMEL VICTORINONo ratings yet

- FEM Transfer or Issue of Any Foreign Security Regulations Kampanisidhant17 Gmailcom 20211006 131928 1 25Document25 pagesFEM Transfer or Issue of Any Foreign Security Regulations Kampanisidhant17 Gmailcom 20211006 131928 1 25Sidhant KampaniNo ratings yet

- C13 Audit Question BankDocument27 pagesC13 Audit Question BankVINUS DHANKHARNo ratings yet

- Assignment ON Cadbury Report AND The RecomendationsDocument9 pagesAssignment ON Cadbury Report AND The RecomendationsSonam LodayNo ratings yet

- 7Document62 pages7BilalNo ratings yet

- Taxman CAFM ScannerDocument491 pagesTaxman CAFM Scannerdroom8521No ratings yet

- Oboase Crew ConstitutionDocument7 pagesOboase Crew Constitutionibrahimalhassan00233No ratings yet

- CA Final - Advanced Auditing StandardsDocument64 pagesCA Final - Advanced Auditing StandardsPraneethNo ratings yet

- Certification Company ProfileDocument20 pagesCertification Company ProfileFirman NugrahaNo ratings yet

- View The Un Audited Financial Results For The Second Quarter 30 September 2022 and Press Release - 0Document16 pagesView The Un Audited Financial Results For The Second Quarter 30 September 2022 and Press Release - 0Shradha mamNo ratings yet

- Practical Workbook - IsO27001 Lead Implementor CourseDocument24 pagesPractical Workbook - IsO27001 Lead Implementor CourseJacktone SikoliaNo ratings yet

- CHAPTER 8 - Financial Reporting and Management Reporting SystemsDocument6 pagesCHAPTER 8 - Financial Reporting and Management Reporting SystemsAngela Marie PenarandaNo ratings yet

- Aaud Cfap 6Document8 pagesAaud Cfap 6Muhammad AhmedNo ratings yet

- ASAL Accounting Workbook Starter PackDocument26 pagesASAL Accounting Workbook Starter Packcthiruvazhmarban100% (1)

- Procedure System of Control Procedure For AuditingDocument10 pagesProcedure System of Control Procedure For AuditingImtiyaz AkhtarNo ratings yet

- Implementation of The Balanced ScorecardDocument39 pagesImplementation of The Balanced ScorecardKeith WardenNo ratings yet

- Week 3 HomeworkDocument11 pagesWeek 3 Homeworkchaitrasuhas100% (1)

- AML Compliance Program GuideDocument11 pagesAML Compliance Program GuidelarissarovaneNo ratings yet

- Know Your JurisdictionDocument10 pagesKnow Your JurisdictionsamaadhuNo ratings yet

- DTLDocument5 pagesDTLBharat Natti RawatNo ratings yet

- 02 Code of EthicsDocument3 pages02 Code of EthicscarloNo ratings yet

- ACC111 Course CompactDocument2 pagesACC111 Course CompactKehindeNo ratings yet

- Responses To Norvan Reports 26.01.22Document3 pagesResponses To Norvan Reports 26.01.22Fuaad DodooNo ratings yet

- BSBFIM501 AAP v2.0Document135 pagesBSBFIM501 AAP v2.0Alicia AlmeidaNo ratings yet

- CPA Review Problems - Audit of LiabilitiesTITLE Philippines CPA Exam Questions on Auditing Liabilities TITLE Audit Liabilities Problems for CPA Review SchoolDocument6 pagesCPA Review Problems - Audit of LiabilitiesTITLE Philippines CPA Exam Questions on Auditing Liabilities TITLE Audit Liabilities Problems for CPA Review SchoolSirNo ratings yet

- Latihan Ac010 FicoDocument3 pagesLatihan Ac010 Ficonanasari85No ratings yet