You might also like

- What Risk Is and Why It Is ImportantDocument17 pagesWhat Risk Is and Why It Is ImportantBela Indah PrastiwiNo ratings yet

- Security Leader Insights for Risk Management: Lessons and Strategies from Leading Security ProfessionalsFrom EverandSecurity Leader Insights for Risk Management: Lessons and Strategies from Leading Security ProfessionalsNo ratings yet

- Risk Management M-2. Approaches To Defining RisksDocument4 pagesRisk Management M-2. Approaches To Defining RisksEngelie Mae ColloNo ratings yet

- RM PrelimDocument14 pagesRM PrelimJazper InocNo ratings yet

- Risk Management Module 1 and 2Document19 pagesRisk Management Module 1 and 2John Rey MercurioNo ratings yet

- Introduction To Risk Management Chapter One Basic Concepts of RiskDocument32 pagesIntroduction To Risk Management Chapter One Basic Concepts of RiskYehualashet MekonninNo ratings yet

- Risk Management Part 1 IntroductionDocument32 pagesRisk Management Part 1 IntroductionJessica LileNo ratings yet

- Agbm 404 Topic 1 HandoutDocument17 pagesAgbm 404 Topic 1 HandoutDennis kiptooNo ratings yet

- Unit - %Document14 pagesUnit - %402 ABHINAYA KEERTHINo ratings yet

- RM Lesson #1 (Jan 28 2022)Document16 pagesRM Lesson #1 (Jan 28 2022)SonnyNo ratings yet

- UNEC__1695844500.pptxDocument22 pagesUNEC__1695844500.pptxnicatmamedov794No ratings yet

- Introduction To Risk: After Going Through The Chapter Student Shall Be Able To UnderstandDocument23 pagesIntroduction To Risk: After Going Through The Chapter Student Shall Be Able To UnderstandPrincess SoniyaNo ratings yet

- Rsik ManagementDocument221 pagesRsik ManagementNirmal ShresthaNo ratings yet

- T1-FRM-1-Ch1-Risk-Mgmt-v3.3 - Study NotesDocument21 pagesT1-FRM-1-Ch1-Risk-Mgmt-v3.3 - Study NotescristianoNo ratings yet

- Introduction To Risk Management: Annalyn Mallari-Caymo, LPT, Maed-Edma LecturerDocument22 pagesIntroduction To Risk Management: Annalyn Mallari-Caymo, LPT, Maed-Edma LecturerNicole OcampoNo ratings yet

- Managerial EconomicsDocument59 pagesManagerial EconomicsJaishan KashyapNo ratings yet

- Risk ManagementDocument12 pagesRisk ManagementParasYadavNo ratings yet

- InsuranceDocument53 pagesInsuranceRohit VkNo ratings yet

- UNEC__1695844500.pptxDocument22 pagesUNEC__1695844500.pptxnicatmamedov794No ratings yet

- Risk ManagementDocument14 pagesRisk ManagementMateta Elie100% (2)

- Risk Management Theoretical Approaches and ClassificationsDocument21 pagesRisk Management Theoretical Approaches and ClassificationsAndreeaEne100% (2)

- Understanding RiskDocument4 pagesUnderstanding RiskJef PerezNo ratings yet

- 21 - Rsik Management1Document93 pages21 - Rsik Management1rajesh bathulaNo ratings yet

- Chapter 1 Risk ManagementDocument17 pagesChapter 1 Risk ManagementKhadar Abdi Hassan "Dholayare"No ratings yet

- Module 1 - Introduction of Risk ManagementDocument14 pagesModule 1 - Introduction of Risk ManagementBANDOY, Crezelda Mae V.No ratings yet

- ENGLEZA Dizertatie Management RiscDocument38 pagesENGLEZA Dizertatie Management RiscProiectulTauNo ratings yet

- Group 7: OF Management StudiesDocument7 pagesGroup 7: OF Management StudiesKarthik SoundarajanNo ratings yet

- Enterprise Risk ManagementDocument51 pagesEnterprise Risk ManagementKajal Tiwary100% (2)

- CHAPTER - 1 INTRODocument41 pagesCHAPTER - 1 INTRONidhin SathishNo ratings yet

- An Overview of Risk Management in Banking PDFDocument77 pagesAn Overview of Risk Management in Banking PDFSweta Kanguri SonulkarNo ratings yet

- Risk Management Section 1Document43 pagesRisk Management Section 1ayariseifallah100% (1)

- Chapter 1 Introduction To RiskDocument17 pagesChapter 1 Introduction To RiskBrenden KapoNo ratings yet

- Risk Management Executive SummaryDocument53 pagesRisk Management Executive SummaryRohit VkNo ratings yet

- Financial Risk ManagementDocument21 pagesFinancial Risk ManagementLianne Esco100% (4)

- SynopsisDocument3 pagesSynopsisRehaan DanishNo ratings yet

- Module 5 - Risk Management 1Document14 pagesModule 5 - Risk Management 1Teresa BuracNo ratings yet

- Risk ManagementDocument26 pagesRisk ManagementRajaPal80% (5)

- Risk and Uncertainty: An IntroductionDocument240 pagesRisk and Uncertainty: An IntroductionRishi RajNo ratings yet

- RM List of Key TermsDocument7 pagesRM List of Key TermsMantenimiento GuatemalaNo ratings yet

- Risk Management Is The Identification, Assessment, and Prioritization of Risks Followed by Coordinated andDocument7 pagesRisk Management Is The Identification, Assessment, and Prioritization of Risks Followed by Coordinated andDilipkumar DornaNo ratings yet

- Irm (Module-1) Bcom 16-19 GenDocument6 pagesIrm (Module-1) Bcom 16-19 GenAstro BoyNo ratings yet

- Module 1 - Introduction To Risk Management 2023Document22 pagesModule 1 - Introduction To Risk Management 2023mjibranali18No ratings yet

- Module 1 Unit I Principles of Risk and Risk ManagementDocument15 pagesModule 1 Unit I Principles of Risk and Risk ManagementGracia SuratosNo ratings yet

- cp1 PDFDocument22 pagescp1 PDFNATURE123No ratings yet

- Introduction To Risk: Learning OutcomesDocument22 pagesIntroduction To Risk: Learning OutcomesChristen CastilloNo ratings yet

- Risk Managent FinalDocument212 pagesRisk Managent FinalZainNo ratings yet

- Risk Management OverviewDocument59 pagesRisk Management OverviewKrishia MendozaNo ratings yet

- Project Risk Management - PM0007 SET-1Document5 pagesProject Risk Management - PM0007 SET-1mbaguideNo ratings yet

- Topic Eight Risk ManagementDocument24 pagesTopic Eight Risk ManagementKelvin mwaiNo ratings yet

- beninsDocument5 pagesbeninsCjade MamarilNo ratings yet

- Effect of Uncertainty On Objectives) Followed by Coordinated and Economical Application of Resources ToDocument6 pagesEffect of Uncertainty On Objectives) Followed by Coordinated and Economical Application of Resources ToKatrina Vianca DecapiaNo ratings yet

- 451520663-FINANCIAL-RISK-MANAGEMENT (1)Document21 pages451520663-FINANCIAL-RISK-MANAGEMENT (1)azeddine daoudiNo ratings yet

- Risk Management Process & TypesDocument35 pagesRisk Management Process & Typessdfghjk100% (2)

- WHO Corporate Risk RegisterDocument10 pagesWHO Corporate Risk RegisterRifa FauziyyahNo ratings yet

- Methods of Risk Management Prepared By:-Dr Gunjan BahetiDocument8 pagesMethods of Risk Management Prepared By:-Dr Gunjan BahetiTwinkal chakradhariNo ratings yet

- Risk Management Insurance CourseDocument140 pagesRisk Management Insurance CourseSagni Belachew DukNo ratings yet

- Germic 1 3Document74 pagesGermic 1 3Mark CorpuzNo ratings yet

- GATLABAYAN - Module 2. SW1Document6 pagesGATLABAYAN - Module 2. SW1Al Dominic GatlabayanNo ratings yet

- Adv 1 - 6 - Intercompany Profit Transactions - Plant Assets - Handout #1Document12 pagesAdv 1 - 6 - Intercompany Profit Transactions - Plant Assets - Handout #1ria fransiscaieNo ratings yet

- ABS ISPS Company - Vessel Audit ChecklistDocument1 pageABS ISPS Company - Vessel Audit ChecklistredchaozNo ratings yet

- JPMorgan Chase London Whale GDocument15 pagesJPMorgan Chase London Whale GMaksym ShodaNo ratings yet

- K WaterDocument113 pagesK WaterAmri Rifki FauziNo ratings yet

- Po - Komal Spare Parts (00000002)Document9 pagesPo - Komal Spare Parts (00000002)Navdeep Singh GrewalNo ratings yet

- Financial Literacy Levels of Small Businesses Owners and It Correlation With Firms' Operating PerformanceDocument72 pagesFinancial Literacy Levels of Small Businesses Owners and It Correlation With Firms' Operating PerformanceRod SisonNo ratings yet

- ONLINE QUIZ Pledge Morgage and AntichresisDocument2 pagesONLINE QUIZ Pledge Morgage and AntichresisSophia PerezNo ratings yet

- Chapter 7 (Basic Elements of Planning and Decision Making)Document21 pagesChapter 7 (Basic Elements of Planning and Decision Making)babon.eshaNo ratings yet

- Tax Invoice-Cum-Receipt: Railtel Corporation of India Limited. Gstin PanDocument1 pageTax Invoice-Cum-Receipt: Railtel Corporation of India Limited. Gstin PanAshihsNo ratings yet

- Andhra Pradesh Board Fee Payment FormDocument1 pageAndhra Pradesh Board Fee Payment FormM JEEVARATHNAM NAIDUNo ratings yet

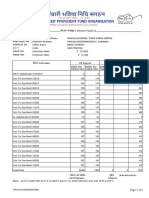

- Member Passbook DetailsDocument2 pagesMember Passbook DetailsNaveen SinghNo ratings yet

- DHL DissertationDocument8 pagesDHL DissertationJahangir AliNo ratings yet

- DetailsNewCreditAssigned Mar23 OthersecuritiesDocument16 pagesDetailsNewCreditAssigned Mar23 OthersecuritiesasamitarannumNo ratings yet

- Pestle AustriaDocument1 pagePestle AustriaRananjay Singh100% (1)

- TQM in Graduate Teacher EducationDocument38 pagesTQM in Graduate Teacher Educationjuditha b. PaunillanNo ratings yet

- Seminar On Central Bank of IndiaDocument23 pagesSeminar On Central Bank of IndiaHarshkinder SainiNo ratings yet

- Tax Question BankDocument109 pagesTax Question BankCalvin Thompson kamukosiNo ratings yet

- Mumias EIADocument35 pagesMumias EIArudiskw456No ratings yet

- Statement of Cash FlowsDocument6 pagesStatement of Cash FlowsJustine VeralloNo ratings yet

- INTERVIEW GUIDE For BMADocument6 pagesINTERVIEW GUIDE For BMAJale Ann A. EspañolNo ratings yet

- Designing The Perfect Procurement Operating Model: OperationsDocument9 pagesDesigning The Perfect Procurement Operating Model: Operationspulsar77No ratings yet

- Solved MAT 2002 Paper With SolutionsDocument59 pagesSolved MAT 2002 Paper With SolutionsAnshuman NarangNo ratings yet

- Fund Cluster 3 (151 Pawcz) December 2022Document40 pagesFund Cluster 3 (151 Pawcz) December 2022Brian KamskyNo ratings yet

- SSRN Id4207171Document39 pagesSSRN Id4207171Nhat LinhNo ratings yet

- Configure Saral PayPack HR & PayrollDocument145 pagesConfigure Saral PayPack HR & PayrollGarry MehrokNo ratings yet

- reading_sample_sap_press_reporting_with_sap_s4hanaDocument32 pagesreading_sample_sap_press_reporting_with_sap_s4hanaCharles SantosNo ratings yet

- Accomplishment February 2019Document8 pagesAccomplishment February 2019saphire donsolNo ratings yet

- Problem 9-21 (Pp. 420-421) : 1. Should The Owner Feel Frustrated With The Variance Reports? ExplainDocument3 pagesProblem 9-21 (Pp. 420-421) : 1. Should The Owner Feel Frustrated With The Variance Reports? ExplainCj SernaNo ratings yet

- Building Contruction Workers Regulation of Employment and Working Conditions Act 1996Document14 pagesBuilding Contruction Workers Regulation of Employment and Working Conditions Act 1996omarmhusainNo ratings yet

- Whatsapp Download Protect-1Document2 pagesWhatsapp Download Protect-1jaisoumya567No ratings yet

- Business Process Mapping: Improving Customer SatisfactionFrom EverandBusiness Process Mapping: Improving Customer SatisfactionRating: 5 out of 5 stars5/5 (1)

- (ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideFrom Everand(ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideRating: 2.5 out of 5 stars2.5/5 (2)

- The Layman's Guide GDPR Compliance for Small Medium BusinessFrom EverandThe Layman's Guide GDPR Compliance for Small Medium BusinessRating: 5 out of 5 stars5/5 (1)

- A Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersFrom EverandA Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersRating: 4.5 out of 5 stars4.5/5 (11)

- GDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekFrom EverandGDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekNo ratings yet

- Audit. Review. Compilation. What's the Difference?From EverandAudit. Review. Compilation. What's the Difference?Rating: 5 out of 5 stars5/5 (1)

- Guide: SOC 2 Reporting on an Examination of Controls at a Service Organization Relevant to Security, Availability, Processing Integrity, Confidentiality, or PrivacyFrom EverandGuide: SOC 2 Reporting on an Examination of Controls at a Service Organization Relevant to Security, Availability, Processing Integrity, Confidentiality, or PrivacyNo ratings yet

- Electronic Health Records: An Audit and Internal Control GuideFrom EverandElectronic Health Records: An Audit and Internal Control GuideNo ratings yet

- Executive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceFrom EverandExecutive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceRating: 4 out of 5 stars4/5 (1)

- Guidelines for Organization of Working Papers on Operational AuditsFrom EverandGuidelines for Organization of Working Papers on Operational AuditsNo ratings yet

- Financial Statement Fraud Casebook: Baking the Ledgers and Cooking the BooksFrom EverandFinancial Statement Fraud Casebook: Baking the Ledgers and Cooking the BooksRating: 4 out of 5 stars4/5 (1)

- GDPR for DevOp(Sec) - The laws, Controls and solutionsFrom EverandGDPR for DevOp(Sec) - The laws, Controls and solutionsRating: 5 out of 5 stars5/5 (1)

- Mastering Internal Audit Fundamentals A Step-by-Step ApproachFrom EverandMastering Internal Audit Fundamentals A Step-by-Step ApproachRating: 4 out of 5 stars4/5 (1)

- A Pocket Guide to Risk Mathematics: Key Concepts Every Auditor Should KnowFrom EverandA Pocket Guide to Risk Mathematics: Key Concepts Every Auditor Should KnowNo ratings yet