You might also like

- SAP Sales Document TypesDocument30 pagesSAP Sales Document TypesSaurabh KumarNo ratings yet

- Conversion and Interface Technical Doc Oracle APPSDocument65 pagesConversion and Interface Technical Doc Oracle APPSsrivastavabhisekNo ratings yet

- VAT-ADDED TAXDocument22 pagesVAT-ADDED TAXDiossaNo ratings yet

- 2 Tips & Tricks For MSMEs Tax Compliance Handouts PDFDocument79 pages2 Tips & Tricks For MSMEs Tax Compliance Handouts PDFGetty Reagan DyNo ratings yet

- Shipment CostDocument26 pagesShipment Costsreenusr100% (4)

- Merchandising Operations GuideDocument108 pagesMerchandising Operations GuideLovely Rose VillarNo ratings yet

- VAT-ADDED TAX EXPLAINEDDocument20 pagesVAT-ADDED TAX EXPLAINEDJerlene Sydney Centeno100% (1)

- Vat With TrainDocument16 pagesVat With TrainElla QuiNo ratings yet

- Vat PDFDocument28 pagesVat PDFJovelyn Villasenor33% (3)

- Coral Bay Tax DigestDocument3 pagesCoral Bay Tax DigestJonathan Dela Cruz100% (1)

- Shared Information/Data (SID) Model: Release 6.0Document122 pagesShared Information/Data (SID) Model: Release 6.0MAGISTERSCNo ratings yet

- Cir vs. Amex, GR No. 152609Document5 pagesCir vs. Amex, GR No. 152609Jani MisterioNo ratings yet

- 1tscm60 Questions1Document25 pages1tscm60 Questions1Hanry Kumala100% (1)

- Value Added Tax Ust PDFDocument23 pagesValue Added Tax Ust PDFcalliemozartNo ratings yet

- Fort Bonifacio vs CIR Case Digest on Transitional Input Tax CreditDocument3 pagesFort Bonifacio vs CIR Case Digest on Transitional Input Tax Creditminri72150% (4)

- Eastern Telecommunications Philippines Inc Vs CirDocument4 pagesEastern Telecommunications Philippines Inc Vs CirAerwin AbesamisNo ratings yet

- VAT Casasola NotesDocument7 pagesVAT Casasola NotesCharm AgripaNo ratings yet

- CPAR VAT (Batch 93) - HandoutDocument38 pagesCPAR VAT (Batch 93) - HandoutJuan Miguel UngsodNo ratings yet

- Kepco Philippines Corporation Vs. CIR VAT Refund CaseDocument4 pagesKepco Philippines Corporation Vs. CIR VAT Refund CaseWhere Did Macky GallegoNo ratings yet

- Fort Bonifacio Vs CIRDocument2 pagesFort Bonifacio Vs CIRCessy Ciar KimNo ratings yet

- Fort Bonifacio Development vs. CIRDocument23 pagesFort Bonifacio Development vs. CIRred gynNo ratings yet

- JRA vs. CIRDocument2 pagesJRA vs. CIRTheodore0176No ratings yet

- CIR vs. CA - G.R. No. 125355 (Digest)Document7 pagesCIR vs. CA - G.R. No. 125355 (Digest)Karen Gina DupraNo ratings yet

- Landmark VAT Cases on Zero-Rated Sales and Franchise OperationsDocument12 pagesLandmark VAT Cases on Zero-Rated Sales and Franchise OperationsJudeRamosNo ratings yet

- OpenText Vendor Invoice Management For SAP Solutions 7.5 SP6 - User Guid...Document130 pagesOpenText Vendor Invoice Management For SAP Solutions 7.5 SP6 - User Guid...CristobalAlcaldeAguirre100% (1)

- FSCM PPTDocument34 pagesFSCM PPTManohar G Shankar100% (1)

- Eatern Telecom v. CIR DigestDocument4 pagesEatern Telecom v. CIR DigestKristineSherikaChyNo ratings yet

- Logistics PowerpointDocument68 pagesLogistics PowerpointMary Mendoza100% (1)

- VAT ZERO-RATED SALES - CIR V ToshibaDocument6 pagesVAT ZERO-RATED SALES - CIR V ToshibaChristine Gel MadrilejoNo ratings yet

- Revised VAT Guidelines for Philippine TaxpayersDocument15 pagesRevised VAT Guidelines for Philippine Taxpayersdencave1No ratings yet

- Invoicing and Regn FlyerDocument2 pagesInvoicing and Regn FlyerMie TotNo ratings yet

- Excel Professional Services, Inc.: Management Firm of Professional Review and Training Center (PRTC)Document3 pagesExcel Professional Services, Inc.: Management Firm of Professional Review and Training Center (PRTC)Mae Angiela TansecoNo ratings yet

- Lesson 8 BtaxDocument4 pagesLesson 8 Btaxdin matanguihanNo ratings yet

- Vat - 1Document20 pagesVat - 1biburaNo ratings yet

- Vat Summary Notes Business TaxationDocument34 pagesVat Summary Notes Business TaxationNinNo ratings yet

- Frequently Asked Questions On VatDocument9 pagesFrequently Asked Questions On VatSteve SantillanNo ratings yet

- Chapter 22Document25 pagesChapter 22Rachel Pepito BaladjayNo ratings yet

- Business-Tax VAT FAQsDocument11 pagesBusiness-Tax VAT FAQsBryan VidalNo ratings yet

- 2 Value Added TaxDocument216 pages2 Value Added TaxnichNo ratings yet

- RMC No. 24-2022Document13 pagesRMC No. 24-2022arnulfojr hicoNo ratings yet

- (VAT) in To: Clarifying (RR) No. The The Tax of (TaxDocument13 pages(VAT) in To: Clarifying (RR) No. The The Tax of (TaxShiela Marie Maraon100% (1)

- CPAR VAT (Batch 92) - HandoutDocument38 pagesCPAR VAT (Batch 92) - HandoutVan DahuyagNo ratings yet

- National Assembly passes tax amendment billDocument11 pagesNational Assembly passes tax amendment billMuhammad Hassan AliNo ratings yet

- VAT Concepts Tax 321Document28 pagesVAT Concepts Tax 321justineNo ratings yet

- 5.0 Intro To Income TaxDocument31 pages5.0 Intro To Income TaxAllan BacudioNo ratings yet

- Taxation Value-Added-TAX ExplainedDocument21 pagesTaxation Value-Added-TAX ExplainediBEAYNo ratings yet

- Facts:: Book ValueDocument2 pagesFacts:: Book Valueultra gayNo ratings yet

- Understanding VAT: A Business Tax, Its Computation, Registration RequirementsDocument24 pagesUnderstanding VAT: A Business Tax, Its Computation, Registration RequirementsPeter AhNo ratings yet

- Who To File RPTDocument9 pagesWho To File RPTLacie Hohenheim (Doraemon)No ratings yet

- VAT 12 Fort Bonifacio Dev. Corp. Vs CIRDocument2 pagesVAT 12 Fort Bonifacio Dev. Corp. Vs CIRMarivic EspiaNo ratings yet

- INPUT & OUTPUT TAX - FORT BONIFACIO DEVELOPMENT CORPORATION vs. CIR DIGESTDocument3 pagesINPUT & OUTPUT TAX - FORT BONIFACIO DEVELOPMENT CORPORATION vs. CIR DIGESTthinkbeforeyoutalkNo ratings yet

- Frequently Asked QuestionsDocument40 pagesFrequently Asked Questionsroy rebosuraNo ratings yet

- Deductions From Gross Income: Basis Ceiling RuleDocument8 pagesDeductions From Gross Income: Basis Ceiling RuleFabiano JoeyNo ratings yet

- BUSTAX SepDocument4 pagesBUSTAX SepReniva KhingNo ratings yet

- Value Added Tax (VAT) : Transfer and Business TaxDocument58 pagesValue Added Tax (VAT) : Transfer and Business TaxRizzle RabadillaNo ratings yet

- Eastern Telecommunications Philippines, Inc., Petitioner, vs. Commissioner of Internal Revenue, RespondentDocument5 pagesEastern Telecommunications Philippines, Inc., Petitioner, vs. Commissioner of Internal Revenue, RespondentMimi KasukaNo ratings yet

- MAT and AMT ExplainedDocument17 pagesMAT and AMT ExplainedNitin ChoudharyNo ratings yet

- How to Compute VAT Payable in the PhilippinesDocument5 pagesHow to Compute VAT Payable in the PhilippinesTere Ypil100% (1)

- Income Tax Law Lecture on NTN, ROI Filing, and Audit BenefitsDocument39 pagesIncome Tax Law Lecture on NTN, ROI Filing, and Audit BenefitsAatir ImranNo ratings yet

- Quiz 4 6 CompilationDocument8 pagesQuiz 4 6 CompilationShelleyNo ratings yet

- (ESCRA) - CIR vs. Cebu Toyo Corp.Document18 pages(ESCRA) - CIR vs. Cebu Toyo Corp.Guiller C. MagsumbolNo ratings yet

- Special Tax Regime For TradersDocument5 pagesSpecial Tax Regime For TradersArsalan LobaniyaNo ratings yet

- Income Tax Amendment Draft Bill 2016Document10 pagesIncome Tax Amendment Draft Bill 2016Muhammad KashifNo ratings yet

- CIR v. Toshiba Information Equipment (Phils.) IncDocument2 pagesCIR v. Toshiba Information Equipment (Phils.) IncEJ PajaroNo ratings yet

- Petitioner Respondent Litigation Division (BIR) Avisado Agan Montenegro & AssociatesDocument17 pagesPetitioner Respondent Litigation Division (BIR) Avisado Agan Montenegro & AssociatesRobert Jayson UyNo ratings yet

- Tax Review Notes 2018 19 Part 6 PDFDocument24 pagesTax Review Notes 2018 19 Part 6 PDFKeziah HuelarNo ratings yet

- Cir VS CebuDocument18 pagesCir VS CebuJAMNo ratings yet

- RMO 47-2020 - Consolidated VAT RefundDocument36 pagesRMO 47-2020 - Consolidated VAT Refunduno_01No ratings yet

- RMC No. 09-87Document1 pageRMC No. 09-87김비앙카No ratings yet

- Assume That Mr. JMLH Breached The VAT Threshold On October of 2018. Optional Standard DeductionDocument1 pageAssume That Mr. JMLH Breached The VAT Threshold On October of 2018. Optional Standard Deduction김비앙카No ratings yet

- 8% Tax - General RulesDocument1 page8% Tax - General Rules김비앙카No ratings yet

- Super Nutrition 4Document1 pageSuper Nutrition 4김비앙카No ratings yet

- 8% Tax - General RulesDocument1 page8% Tax - General Rules김비앙카No ratings yet

- 8% Tax - Important Rules:: ST RDDocument1 page8% Tax - Important Rules:: ST RD김비앙카No ratings yet

- Tax 3Document1 pageTax 3김비앙카No ratings yet

- Bar 2021 - PropertyDocument4 pagesBar 2021 - Property김비앙카No ratings yet

- Table of Legitimes1Document1 pageTable of Legitimes1김비앙카No ratings yet

- Bar 2021 - Family CodeDocument3 pagesBar 2021 - Family Code김비앙카No ratings yet

- Table of Legitimes2Document1 pageTable of Legitimes2김비앙카No ratings yet

- Table of Legitimes3Document1 pageTable of Legitimes3김비앙카No ratings yet

- Key Combination Function: BasicsDocument2 pagesKey Combination Function: Basics김비앙카No ratings yet

- Bar 2021 - Data Privacy ActDocument7 pagesBar 2021 - Data Privacy Act김비앙카No ratings yet

- VAWC1Document1 pageVAWC1김비앙카No ratings yet

- A. Rights and Obligations of Couples in Intimate Relationships (Rep. Act No. 9262) 1. Vawc ActsDocument1 pageA. Rights and Obligations of Couples in Intimate Relationships (Rep. Act No. 9262) 1. Vawc Acts김비앙카No ratings yet

- Table of Legitimes3Document1 pageTable of Legitimes3김비앙카No ratings yet

- VAWC1Document1 pageVAWC1김비앙카No ratings yet

- Table of Legitimes3Document1 pageTable of Legitimes3김비앙카No ratings yet

- Protecting victims through protection ordersDocument1 pageProtecting victims through protection ordersKim SKNo ratings yet

- PersonsDocument2 pagesPersons김비앙카No ratings yet

- Table of Legitimes3Document1 pageTable of Legitimes3김비앙카No ratings yet

- Table of Legitimes3Document1 pageTable of Legitimes3김비앙카No ratings yet

- Table of Legitimes2Document1 pageTable of Legitimes2김비앙카No ratings yet

- Table of Legitimes1Document1 pageTable of Legitimes1김비앙카No ratings yet

- Sap Fresher ResumeDocument3 pagesSap Fresher ResumeLokesh DoraNo ratings yet

- Macam V CADocument2 pagesMacam V CA001nooneNo ratings yet

- Schlage PB74 2013Document398 pagesSchlage PB74 2013Security Lock DistributorsNo ratings yet

- Date Opening Balance Production On Date Total (B+C) Production MTDDocument31 pagesDate Opening Balance Production On Date Total (B+C) Production MTDdhirajsatyam98982285No ratings yet

- Swaroop Enterprises 11.02.2019Document2 pagesSwaroop Enterprises 11.02.2019Sunil AlandNo ratings yet

- Resume for Inventory and Supply Chain ProfessionalDocument5 pagesResume for Inventory and Supply Chain ProfessionalHey MamasNo ratings yet

- CP1W-ETN61 CP1H / CP1L FINS Ethernet Adapter Application and Setup GuideDocument10 pagesCP1W-ETN61 CP1H / CP1L FINS Ethernet Adapter Application and Setup GuidedromerxNo ratings yet

- Sales and billing exits and enhancementsDocument16 pagesSales and billing exits and enhancementsashahmednNo ratings yet

- Hathway Internet BillDocument1 pageHathway Internet BillRamesh V MNo ratings yet

- CST n55-Slvp28nd ManualDocument48 pagesCST n55-Slvp28nd ManualRicardo NovondoNo ratings yet

- Aso ApiDocument62 pagesAso Apishameem_ficsNo ratings yet

- 01 - IIIrd PartyDocument5 pages01 - IIIrd PartyRavindra SNo ratings yet

- Harmonising Border Procedures - Position PaperDocument10 pagesHarmonising Border Procedures - Position PaperPeter SsempebwaNo ratings yet

- Log MM Commodity Ehp6 ConstraintsDocument4 pagesLog MM Commodity Ehp6 ConstraintskalyanNo ratings yet

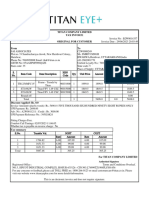

- Titaeye+ BillDocument2 pagesTitaeye+ Billrav prashant SinghNo ratings yet

- Phoenix House Topcliffe Lane Tingley Wakefield WF3 1WEDocument7 pagesPhoenix House Topcliffe Lane Tingley Wakefield WF3 1WEfugzMabugzNo ratings yet

- Tax Invoice for TVsDocument1 pageTax Invoice for TVsAthahNo ratings yet

- TMP 3 AA0Document2 pagesTMP 3 AA0nithiananthiNo ratings yet

- Terms and Conditions: Atria Convergence Technologies Limited, Due Date: 15/11/2020Document2 pagesTerms and Conditions: Atria Convergence Technologies Limited, Due Date: 15/11/2020MaayaBimbamNo ratings yet

- Telephone No Amount Payable Due Date: Bill Mail Service Tax InvoiceDocument3 pagesTelephone No Amount Payable Due Date: Bill Mail Service Tax InvoiceMannknowz JaredaNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)RMNo ratings yet