You might also like

- Second Division February 14, 2018 - G.R. No. 205693 - REYES, JR., J.: MANUEL M. VENEZUELA, Petitioner People of The Philippines, RespondentDocument9 pagesSecond Division February 14, 2018 - G.R. No. 205693 - REYES, JR., J.: MANUEL M. VENEZUELA, Petitioner People of The Philippines, RespondentpatrickNo ratings yet

- Ocampo Vs Abando With Three IssuesDocument4 pagesOcampo Vs Abando With Three IssuespatrickNo ratings yet

- PP Vs EllasosDocument4 pagesPP Vs EllasospatrickNo ratings yet

- Facts:: Andal vs. Macaraig GR No. 2474, May 30, 1951Document1 pageFacts:: Andal vs. Macaraig GR No. 2474, May 30, 1951Russell Stanley Que GeronimoNo ratings yet

- Arias VS SandiganbayanDocument22 pagesArias VS SandiganbayanpatrickNo ratings yet

- 2 Manaloto Vs VelascoDocument4 pages2 Manaloto Vs VelascopatrickNo ratings yet

- Castaneda Vs AlemanyDocument2 pagesCastaneda Vs AlemanypatrickNo ratings yet

- Paramount Vs CaDocument2 pagesParamount Vs CapatrickNo ratings yet

- PAREDES 21 BARONSMKTvsCADocument2 pagesPAREDES 21 BARONSMKTvsCApatrickNo ratings yet

- RP VS UyDocument2 pagesRP VS UypatrickNo ratings yet

- GPL Vs CADocument5 pagesGPL Vs CApatrickNo ratings yet

- 7 - Parreno Vs CoaDocument1 page7 - Parreno Vs CoapatrickNo ratings yet

- Paramount Vs CADocument2 pagesParamount Vs CApatrickNo ratings yet

- Krivenko Vs Register of DeedsDocument1 pageKrivenko Vs Register of DeedspatrickNo ratings yet

- Rizal Vs Exec SecretaryDocument25 pagesRizal Vs Exec SecretarypatrickNo ratings yet

- Romulo, Mabanta, Buenaventura, Sayoc & de Los Angeles For PetitionerDocument5 pagesRomulo, Mabanta, Buenaventura, Sayoc & de Los Angeles For PetitionerpatrickNo ratings yet

- Cadayona v. CA PDFDocument4 pagesCadayona v. CA PDFNaika Ramos LofrancoNo ratings yet

- Tumalad Vs ViciencioDocument5 pagesTumalad Vs VicienciopatrickNo ratings yet

- CALTEX (PHILIPPINES), INC., Petitioner, vs. The Intermediate Appellate Court and Asia PACIFIC AIRWAYS, INC., RespondentsDocument5 pagesCALTEX (PHILIPPINES), INC., Petitioner, vs. The Intermediate Appellate Court and Asia PACIFIC AIRWAYS, INC., RespondentspatrickNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Diplomatic Laws: Assistant Professor Department of Law University of ChittagongDocument30 pagesDiplomatic Laws: Assistant Professor Department of Law University of ChittagongAfsana AronnaNo ratings yet

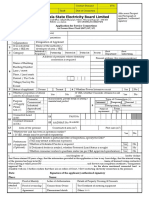

- Kerala State Electricity Board Limited: For Demand Based Tariff (EHT / HT / LT)Document3 pagesKerala State Electricity Board Limited: For Demand Based Tariff (EHT / HT / LT)Joseph VargheseNo ratings yet

- Cyber Crime 2012Document30 pagesCyber Crime 2012Caryl Penarubia100% (1)

- Incident Accident ReportDocument2 pagesIncident Accident ReportDS SystemsNo ratings yet

- Tress PassDocument33 pagesTress PassSHUBH AGRAWALNo ratings yet

- ADR AssignmentDocument2 pagesADR AssignmentDamon SalvatoreNo ratings yet

- Ethics Module 4Document26 pagesEthics Module 4Glorime JunioNo ratings yet

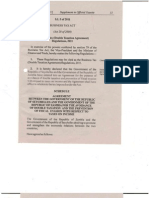

- DTC Agreement Between Zambia and SeychellesDocument31 pagesDTC Agreement Between Zambia and SeychellesOECD: Organisation for Economic Co-operation and DevelopmentNo ratings yet

- Michael and Others V The Chief Constable of 2 - 1942557653Document11 pagesMichael and Others V The Chief Constable of 2 - 1942557653JenniferNo ratings yet

- Brown v. Yambao, 102 Phil. 168Document3 pagesBrown v. Yambao, 102 Phil. 168NEILMAR JARABELO PANISALESNo ratings yet

- Comprehensive Dangerous Drug Act of 2002Document47 pagesComprehensive Dangerous Drug Act of 2002Rey RectoNo ratings yet

- Core Characteristics of A CrimeDocument27 pagesCore Characteristics of A CrimepriscalauraNo ratings yet

- Code Description Remark 4 3 3 2 3 2 3Document1 pageCode Description Remark 4 3 3 2 3 2 3Aljo FernandezNo ratings yet

- LEARNING GUIDE QUESTIONS (Continuation)Document3 pagesLEARNING GUIDE QUESTIONS (Continuation)Joseph ConcepcionNo ratings yet

- Policy Paper 1Document40 pagesPolicy Paper 1Roxanne Datuin UsonNo ratings yet

- Chapter 9 DamagesDocument9 pagesChapter 9 DamagesIan Mual PeterNo ratings yet

- Ramos vs. ImbangDocument4 pagesRamos vs. ImbangDAblue ReyNo ratings yet

- Nagraj ComicDocument13 pagesNagraj ComicJagminder Singh40% (5)

- The Unveiling of The Teachings of The Rosicrucian Order An ExposéDocument187 pagesThe Unveiling of The Teachings of The Rosicrucian Order An ExposéClymer77798% (56)

- Application For Appointment: Mauritius Institute of Training and Development Head OfficeDocument3 pagesApplication For Appointment: Mauritius Institute of Training and Development Head OfficeKervin MooteealooNo ratings yet

- Tuuci v. Fiberbuilt UmbrellasDocument35 pagesTuuci v. Fiberbuilt UmbrellasPriorSmartNo ratings yet

- Advertisement General Manager (Coal)Document9 pagesAdvertisement General Manager (Coal)Kushwaha Auto partNo ratings yet

- To Acquire Higher QualificationsDocument3 pagesTo Acquire Higher QualificationsSangrama PadhiNo ratings yet

- Legal and Ethical Aspect of NursingDocument34 pagesLegal and Ethical Aspect of Nursingyn8jg9fwx6No ratings yet

- Bayan. Their Respective Testimonies Differ Only As To When The Help WasDocument3 pagesBayan. Their Respective Testimonies Differ Only As To When The Help WasMina AragonNo ratings yet

- 10 Takata Philippines v. BLR and SALAMATDocument15 pages10 Takata Philippines v. BLR and SALAMATkimNo ratings yet

- TranslationDocument3 pagesTranslationkaartheekvyyahruti4291No ratings yet

- Saugat Modak Ghy X MXN Train TicketDocument2 pagesSaugat Modak Ghy X MXN Train TicketSaugat ModakNo ratings yet

- Muskan Dosar 1625332826 ResumeDocument3 pagesMuskan Dosar 1625332826 ResumeSatakshi N DixitNo ratings yet

- General Diary in EnglishDocument3 pagesGeneral Diary in EnglishSabrina'sNo ratings yet