You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- My PHP GeneratorDocument305 pagesMy PHP GeneratorsatmaniaNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Data Modeling With Graph DatabasesDocument68 pagesData Modeling With Graph Databasessatmania100% (2)

- Agreement of SaleDocument3 pagesAgreement of SaleAYAN AHMEDNo ratings yet

- Unit 2 Cost Concepts and Classifications (BBA)Document25 pagesUnit 2 Cost Concepts and Classifications (BBA)Aayushi KothariNo ratings yet

- In Gold We Trust Report 2020 Extended Version EnglishDocument356 pagesIn Gold We Trust Report 2020 Extended Version EnglishTFMetals100% (3)

- Idc Seagate Dataage Whitepaper PDFDocument28 pagesIdc Seagate Dataage Whitepaper PDFsatmaniaNo ratings yet

- Business PlanDocument12 pagesBusiness PlanRyzer AmahitNo ratings yet

- Pages From Unified-Log-Zk-Nov15-2 - Part3Document2 pagesPages From Unified-Log-Zk-Nov15-2 - Part3satmaniaNo ratings yet

- Pages From Unified-Log-Zk-Nov15-3 - Part1Document2 pagesPages From Unified-Log-Zk-Nov15-3 - Part1satmaniaNo ratings yet

- Pages From Unified-Log-Zk-Nov15-3 - Part3Document2 pagesPages From Unified-Log-Zk-Nov15-3 - Part3satmaniaNo ratings yet

- 06 Machine LearningDocument24 pages06 Machine LearningsatmaniaNo ratings yet

- Pages From Unified Log ZK Nov15 4 - Part2Document2 pagesPages From Unified Log ZK Nov15 4 - Part2satmaniaNo ratings yet

- Pages From Unified-Log-Zk-Nov15-5Document5 pagesPages From Unified-Log-Zk-Nov15-5satmaniaNo ratings yet

- DATASETS GPS DataDocument3 pagesDATASETS GPS DatasatmaniaNo ratings yet

- hw09 Monitoring Best PracticesDocument6 pageshw09 Monitoring Best PracticessatmaniaNo ratings yet

- Oracke ContainerDocument1 pageOracke ContainersatmaniaNo ratings yet

- CS246 Proof ProbabilityDocument13 pagesCS246 Proof ProbabilitysatmaniaNo ratings yet

- HW4 TutorialDocument17 pagesHW4 TutorialsatmaniaNo ratings yet

- Fillatre Big DataDocument98 pagesFillatre Big DatasatmaniaNo ratings yet

- The Forrester Wave™ - Big Data Fabric Q2 2018 PDFDocument18 pagesThe Forrester Wave™ - Big Data Fabric Q2 2018 PDFsatmaniaNo ratings yet

- Idc Digital Universe 2014 PDFDocument17 pagesIdc Digital Universe 2014 PDFsatmaniaNo ratings yet

- Conference Presentation TipsDocument28 pagesConference Presentation Tipssatmania0% (1)

- Swarm and Evolutionary Computation: ACM Transactions On Knowledge Discovery From DataDocument1 pageSwarm and Evolutionary Computation: ACM Transactions On Knowledge Discovery From DatasatmaniaNo ratings yet

- Cie1931 RGBDocument70 pagesCie1931 RGBsatmaniaNo ratings yet

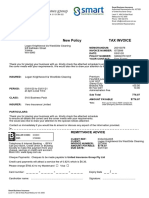

- Tax InvoiceDocument1 pageTax InvoiceᴘᴇᴀᴄᴏᴄᴋNo ratings yet

- Chapter Four-Part I: Accounting For Governmental FundsDocument28 pagesChapter Four-Part I: Accounting For Governmental FundsabateNo ratings yet

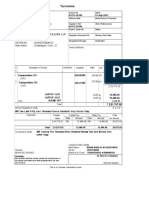

- Logan Knightwood Ta WestSide Cleaning (033LOGA005) - Tax InvoiceDocument4 pagesLogan Knightwood Ta WestSide Cleaning (033LOGA005) - Tax InvoiceLoki KingNo ratings yet

- Assign 2 Answer Partnership Operations Millan 2021Document5 pagesAssign 2 Answer Partnership Operations Millan 2021mhikeedelantarNo ratings yet

- L/4Ustn: Rnfrrt6' (D - FlcfusrqwiDocument52 pagesL/4Ustn: Rnfrrt6' (D - FlcfusrqwiBalaji AssociatesNo ratings yet

- Contradictions of Capitalism in The South African Kalahari Indigenous Bushmen Their Brand and Baasskap in TourismDocument17 pagesContradictions of Capitalism in The South African Kalahari Indigenous Bushmen Their Brand and Baasskap in TourismMARIA MARTHA SARMIENTONo ratings yet

- Pdfcoffee LojnkbkbjkmDocument35 pagesPdfcoffee Lojnkbkbjkmdraga pinasNo ratings yet

- Insights Mind Maps: Issues Related To MSPDocument2 pagesInsights Mind Maps: Issues Related To MSPrushikesh dharmadhikariNo ratings yet

- Payslip - 2022 12 31Document1 pagePayslip - 2022 12 31mateivalentin94No ratings yet

- Pakam, Khiezna E. Bsac-1b Assignment 3-FarDocument5 pagesPakam, Khiezna E. Bsac-1b Assignment 3-FarKhiezna PakamNo ratings yet

- Keywords: Small Business, Sustainability, Customer Retention, CRM, Relationship ManagementDocument25 pagesKeywords: Small Business, Sustainability, Customer Retention, CRM, Relationship ManagementFranklyn ChamindaNo ratings yet

- Contemporary World GE3-Module 5 Contemporary World GE3-Module 5Document8 pagesContemporary World GE3-Module 5 Contemporary World GE3-Module 5Erica CanonNo ratings yet

- Region Province Reference Number Learner IDDocument10 pagesRegion Province Reference Number Learner IDLloydie LopezNo ratings yet

- VSPD EpfDocument115 pagesVSPD EpfDIPAK VINAYAK SHIRBHATENo ratings yet

- CORE Finance Project Term 1Document4 pagesCORE Finance Project Term 1ashbornsfragmentNo ratings yet

- BGS Customer Relationship ManagementDocument22 pagesBGS Customer Relationship ManagementaasimchoudharyNo ratings yet

- Sree Susheel Oil IndustriesDocument27 pagesSree Susheel Oil IndustriesDeekshith NNo ratings yet

- Analisis Pengaruh Inflasi, Kurs, Utang Luar Negeri Dan Ekspor Terhadap Cadangan Devisa IndonesiaDocument23 pagesAnalisis Pengaruh Inflasi, Kurs, Utang Luar Negeri Dan Ekspor Terhadap Cadangan Devisa IndonesiaarifNo ratings yet

- The Specific and General External Environmental FactorsDocument3 pagesThe Specific and General External Environmental FactorsMishkatul FerdousNo ratings yet

- NCP CarsDocument7 pagesNCP CarsNayab NoorNo ratings yet

- Proxy PrelimDocument47 pagesProxy PrelimGabriel uyNo ratings yet

- JFC 2021 SEC Sustainability ReportDocument83 pagesJFC 2021 SEC Sustainability Reportgjana4179No ratings yet

- The ONE ThingDocument11 pagesThe ONE ThingNemuel KesslerNo ratings yet

- 01 Quiz 1Document3 pages01 Quiz 1Emperor SavageNo ratings yet

- Bill AckmanDocument729 pagesBill AckmanTheMoneyMitraNo ratings yet

- (Solution Answers) Advanced Accounting by Dayag, Version 2017 - Chapter 2 (Partnership - Continuation) - Solution To Multiple Choice (Part C)Document2 pages(Solution Answers) Advanced Accounting by Dayag, Version 2017 - Chapter 2 (Partnership - Continuation) - Solution To Multiple Choice (Part C)John Carlos DoringoNo ratings yet