You might also like

- Interpretation OF STATUTEDocument35 pagesInterpretation OF STATUTEdeepak sharmaNo ratings yet

- Definition of INCOME Under Income Tax (Section 2 (24) )Document7 pagesDefinition of INCOME Under Income Tax (Section 2 (24) )deepak sharmaNo ratings yet

- Public International LawDocument13 pagesPublic International Lawdeepak sharmaNo ratings yet

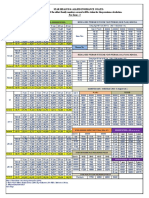

- Zone - 3 Rate With Tax 18 (Rev 1Document1 pageZone - 3 Rate With Tax 18 (Rev 1deepak sharmaNo ratings yet

- Common - Proposal Form Health Policy StarDocument4 pagesCommon - Proposal Form Health Policy Stardeepak sharmaNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Dornbusch 6e Chapter12Document19 pagesDornbusch 6e Chapter12kushalNo ratings yet

- TVOM Theory QuizDocument2 pagesTVOM Theory QuizKim DavilloNo ratings yet

- Account Closure Form2 PDFDocument1 pageAccount Closure Form2 PDFdigant daveNo ratings yet

- 1571306792215Document4 pages1571306792215amol dhobleNo ratings yet

- Math 6 Q2 Module 4Document14 pagesMath 6 Q2 Module 4Leo CerenoNo ratings yet

- Daily Trading Stance - 2010-01-11Document3 pagesDaily Trading Stance - 2010-01-11Trading FloorNo ratings yet

- Iflas and Chapter 11 Classical Islamic Law and Modern BankruptcyDocument27 pagesIflas and Chapter 11 Classical Islamic Law and Modern BankruptcyManfadawi FadawiNo ratings yet

- Invoice - NMC - Voice Conference - Rentals - Mar-2022Document1 pageInvoice - NMC - Voice Conference - Rentals - Mar-2022Sujatha NarasaraopetNo ratings yet

- Alfred C. Morley-The Financial Services Industry - Banks, Thrifts, Insurance Companies, and Securities Firms-AIMR (CFA Institute) (1992) PDFDocument148 pagesAlfred C. Morley-The Financial Services Industry - Banks, Thrifts, Insurance Companies, and Securities Firms-AIMR (CFA Institute) (1992) PDFtariqul21No ratings yet

- Industrial Securities MarketDocument16 pagesIndustrial Securities MarketNaga Mani Merugu100% (3)

- Issue: Whether The Legal Interest Rate For A Judgment Involving Damages To Property Is 12%Document2 pagesIssue: Whether The Legal Interest Rate For A Judgment Involving Damages To Property Is 12%Vance CeballosNo ratings yet

- Types of Risk in MicrofinanceDocument9 pagesTypes of Risk in Microfinancevish100% (1)

- XdocmulationDocument4 pagesXdocmulationKuthe Prashant GajananNo ratings yet

- Personal Finance Chapter 1Document3 pagesPersonal Finance Chapter 1Brittany Jablonski WilliamsNo ratings yet

- GST Compliance in Statutory Bank Branch Audit: Ca. Vineet RathiDocument46 pagesGST Compliance in Statutory Bank Branch Audit: Ca. Vineet Rathianon_127497276No ratings yet

- EBCL - Adv Chirag Chotrani, YES Academy, PuneDocument611 pagesEBCL - Adv Chirag Chotrani, YES Academy, PuneTathagat AdalatwaleNo ratings yet

- (6-2) Interest Rate Levels CH Answer: B MEDIUMDocument9 pages(6-2) Interest Rate Levels CH Answer: B MEDIUMMohsin2k100% (1)

- Case Study On Vnacs: PrashantDocument5 pagesCase Study On Vnacs: PrashantPrashant BagdiaNo ratings yet

- Assignment SampleDocument16 pagesAssignment SamplejgukykNo ratings yet

- Financial Literacy PowerpointDocument17 pagesFinancial Literacy Powerpointapi-40190669833% (3)

- 0452 s15 QP 22Document20 pages0452 s15 QP 22zuzoyopiNo ratings yet

- Final Banking Law OutlineDocument95 pagesFinal Banking Law OutlineQuinton JohnsonNo ratings yet

- ASE20091 June 2021 Question PaperDocument20 pagesASE20091 June 2021 Question PaperMusthari KhanNo ratings yet

- A. 1a Problem 4Document1 pageA. 1a Problem 4shuzoNo ratings yet

- Kendriya Vidyalaya No.1 Kunjaban, Agartala Tripura: Submitted By: Aboya DebbarmaDocument12 pagesKendriya Vidyalaya No.1 Kunjaban, Agartala Tripura: Submitted By: Aboya Debbarmaakash debbarmaNo ratings yet

- 27 Agent Sales Report Host Solo Datos Sales SummaryDocument3 pages27 Agent Sales Report Host Solo Datos Sales SummaryjjprietojNo ratings yet

- 7 Different Types of Journal in Accounting With ExamplesDocument8 pages7 Different Types of Journal in Accounting With ExamplesHaroon YousafNo ratings yet

- Chapter 2 Case 2 Sole Proprietors-1Document1 pageChapter 2 Case 2 Sole Proprietors-1almacen chrisNo ratings yet

- Multinational Corporations: Some of Characteristics of Mncs AreDocument7 pagesMultinational Corporations: Some of Characteristics of Mncs AreMuskan KaurNo ratings yet

- The Negotiable Instruments Act, 1881Document55 pagesThe Negotiable Instruments Act, 1881meghna_mg8780% (5)