You might also like

- 10 Job Order CostingDocument5 pages10 Job Order CostingAllegria AlamoNo ratings yet

- Cost Accounting Cost Control FinalsDocument12 pagesCost Accounting Cost Control FinalsCindy Dela CruzNo ratings yet

- Midterm - Quiz - AEC6Document4 pagesMidterm - Quiz - AEC6aprilNo ratings yet

- JOB ORDER COSTING Practice SetDocument5 pagesJOB ORDER COSTING Practice SetGoogle UserNo ratings yet

- Process CostingDocument18 pagesProcess CostingCheliah Mae ImperialNo ratings yet

- LMSDocument4 pagesLMSJohn Carlo LorenzoNo ratings yet

- Job Order Costing SeatworkDocument7 pagesJob Order Costing SeatworksarahbeeNo ratings yet

- WDocument9 pagesWSamantha CabugonNo ratings yet

- Production Departments Direct Labor Rate Manufacturing Overhead Application RatesDocument10 pagesProduction Departments Direct Labor Rate Manufacturing Overhead Application RatesSano ManjiroNo ratings yet

- 2 - Classroom ExercisesDocument4 pages2 - Classroom ExercisesHannah Jane ToribioNo ratings yet

- Cost Acctg 1617 2ndsem CE AKDocument10 pagesCost Acctg 1617 2ndsem CE AKanon_684731700% (1)

- AFAR Pre-Board - Set B Overhead Costing ProblemsDocument11 pagesAFAR Pre-Board - Set B Overhead Costing ProblemsRence Gonzales0% (2)

- Afar Job Order Costing Spoilage DefectiveDocument4 pagesAfar Job Order Costing Spoilage DefectiveKaye Angelie UsogNo ratings yet

- Cost Accounting MidtermDocument4 pagesCost Accounting MidtermMieryle DioctonNo ratings yet

- ACCTG 201 Group 1 TTH 6 To 9Document12 pagesACCTG 201 Group 1 TTH 6 To 9Joyce BusaNo ratings yet

- Quiz No. 3 Job-Order Costing QuestionsDocument14 pagesQuiz No. 3 Job-Order Costing QuestionsEdi wow WowNo ratings yet

- ARS Webinar Handout 10292023Document3 pagesARS Webinar Handout 10292023johnafar998No ratings yet

- 1st Half Quiz 5finalDocument2 pages1st Half Quiz 5finalLauNo ratings yet

- Accounting For Production Losses in A Job Order CostingDocument2 pagesAccounting For Production Losses in A Job Order CostingMARYGRACE FERRER100% (1)

- VIRGEN MILAGROSA UNIVERSITY COST ACCOUNTING QUIZDocument4 pagesVIRGEN MILAGROSA UNIVERSITY COST ACCOUNTING QUIZMary Joanne Tapia33% (3)

- Cost Final Exam ReviewerDocument8 pagesCost Final Exam ReviewerAlliana CunananNo ratings yet

- Job Order Costing Spoilage Defective - StudentDocument4 pagesJob Order Costing Spoilage Defective - StudentVince Christian PadernalNo ratings yet

- Cost Accounting & Control Midterm ExaminationDocument7 pagesCost Accounting & Control Midterm ExaminationFerb CruzadaNo ratings yet

- 05.16.2023 ASSIGNMENT Activity Problem With Theories-Process Costing and JOB Order Costing - With ANSWER KEYDocument11 pages05.16.2023 ASSIGNMENT Activity Problem With Theories-Process Costing and JOB Order Costing - With ANSWER KEYAngel Cil RuleteNo ratings yet

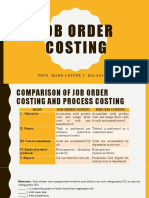

- Job Order Costing: Prof. Mark Lester T. Balasa, CpaDocument24 pagesJob Order Costing: Prof. Mark Lester T. Balasa, CpaNah HamzaNo ratings yet

- Cost Accounting Midterm Examdocx PDF FreeDocument5 pagesCost Accounting Midterm Examdocx PDF FreeHannah Denise BatallangNo ratings yet

- Midterm ExamDocument8 pagesMidterm ExamKryss Clyde TabliganNo ratings yet

- Advance Financial Accounting and Reporting: Additional InformationDocument4 pagesAdvance Financial Accounting and Reporting: Additional InformationRoxell CaibogNo ratings yet

- 2019A QE Strategic Cost Management FinalDocument5 pages2019A QE Strategic Cost Management FinalJam Crausus100% (1)

- Instructions:: La Salle University College of Business and AccountancyDocument5 pagesInstructions:: La Salle University College of Business and Accountancykateangel ellesoNo ratings yet

- Form Two Cost AccountingDocument6 pagesForm Two Cost AccountingBernard DarkwahNo ratings yet

- Please Write The Letter of Your Answer Beside Each NumberDocument8 pagesPlease Write The Letter of Your Answer Beside Each NumbershengNo ratings yet

- MAS_3104_Standard_Costing_and_Variance_Analysis___MCQDocument6 pagesMAS_3104_Standard_Costing_and_Variance_Analysis___MCQmonicafrancisgarcesNo ratings yet

- Job Order Costing Spoilage and Rework QuizDocument3 pagesJob Order Costing Spoilage and Rework Quizela kikayNo ratings yet

- Factory OverheadDocument2 pagesFactory OverheadKeanna Denise GonzalesNo ratings yet

- D. Depends On The Significance of The Amount.: Cost Accounting Comprehensive Examination 1Document14 pagesD. Depends On The Significance of The Amount.: Cost Accounting Comprehensive Examination 1Ferb CruzadaNo ratings yet

- Advanced Accounting ExamDocument10 pagesAdvanced Accounting ExamMendoza Ron NixonNo ratings yet

- Quiz 1 Intro and Cost BehaviorsDocument3 pagesQuiz 1 Intro and Cost BehaviorsaaromeroNo ratings yet

- ACECOSTDocument6 pagesACECOSTXyne FernandezNo ratings yet

- Job Order Costing QuizDocument6 pagesJob Order Costing QuizAllen Hendrick SantiagoNo ratings yet

- Epektos Part 1Document4 pagesEpektos Part 1Melvin MendozaNo ratings yet

- Chapter 2 SeatworkDocument7 pagesChapter 2 Seatworkrhiz cyrelle calanoNo ratings yet

- Michael John C. Ode, CPA: AfarDocument3 pagesMichael John C. Ode, CPA: AfarYojec RollonNo ratings yet

- Cost Accounting & Control Quiz No. 1Document8 pagesCost Accounting & Control Quiz No. 1Ferb CruzadaNo ratings yet

- JOBCOSTINGDocument4 pagesJOBCOSTINGkakaoNo ratings yet

- Cost Accounting and ManagementDocument7 pagesCost Accounting and ManagementCris Tarrazona CasipleNo ratings yet

- Test I. True-False Direction: Write T If The Statement Is Correct and F If It Is Wrong BesideDocument8 pagesTest I. True-False Direction: Write T If The Statement Is Correct and F If It Is Wrong BesideXingYang KiSada0% (1)

- Final Examination - Management AccountingDocument13 pagesFinal Examination - Management AccountingJoshua UmaliNo ratings yet

- University of Caloocan City Cost Accounting & Control Quiz No. 1Document8 pagesUniversity of Caloocan City Cost Accounting & Control Quiz No. 1Mikha SemañaNo ratings yet

- This Study Resource WasDocument4 pagesThis Study Resource WasNhel AlvaroNo ratings yet

- Job Order Assignment PDFDocument3 pagesJob Order Assignment PDFAnne Marie100% (1)

- KA SET A Cost Accounting and ControlDocument11 pagesKA SET A Cost Accounting and ControlMicah ErguizaNo ratings yet

- Job Order Costing Quiz QuestionsDocument25 pagesJob Order Costing Quiz QuestionsWed CornelNo ratings yet

- TOS Cost AssessmentDocument41 pagesTOS Cost AssessmentHNo ratings yet

- MODULE 3 Job Order Costing PDFDocument9 pagesMODULE 3 Job Order Costing PDFjay mhonsaint100% (1)

- MCP TutorialDocument3 pagesMCP TutorialPaola HuyongNo ratings yet

- Long Test Midterm Coverage - QDocument6 pagesLong Test Midterm Coverage - QMark IlanoNo ratings yet

- Quiz1 AdvcostDocument8 pagesQuiz1 AdvcostPatOcampo100% (3)

- Production and Maintenance Optimization Problems: Logistic Constraints and Leasing Warranty ServicesFrom EverandProduction and Maintenance Optimization Problems: Logistic Constraints and Leasing Warranty ServicesNo ratings yet

- MATHEMATICAL ECONOMICSDocument54 pagesMATHEMATICAL ECONOMICSCities Normah0% (1)

- TILE FIXING GUIDEDocument1 pageTILE FIXING GUIDEStavros ApostolidisNo ratings yet

- Project Report On AdidasDocument33 pagesProject Report On Adidassanyam73% (37)

- Travis Walton Part 1 MUFON Case FileDocument346 pagesTravis Walton Part 1 MUFON Case FileClaudio Silva100% (1)

- Smoktech Vmax User ManualDocument9 pagesSmoktech Vmax User ManualStella PapaNo ratings yet

- PropensityModels PDFDocument4 pagesPropensityModels PDFSarbarup BanerjeeNo ratings yet

- Casestudy3 Hbo MaDocument2 pagesCasestudy3 Hbo Ma132345usdfghjNo ratings yet

- Business Analysis FoundationsDocument39 pagesBusiness Analysis FoundationsPriyankaNo ratings yet

- Admission Procedure For International StudentsDocument8 pagesAdmission Procedure For International StudentsAndreea Anghel-DissanayakaNo ratings yet

- L Williams ResumeDocument2 pagesL Williams Resumeapi-555629186No ratings yet

- Final Annotated BibiliographyDocument4 pagesFinal Annotated Bibiliographyapi-491166748No ratings yet

- Service Parts List: 54-26-0005 2551-20 M12™ FUEL™ SURGE™ 1/4" Hex Hydraulic Driver K42ADocument2 pagesService Parts List: 54-26-0005 2551-20 M12™ FUEL™ SURGE™ 1/4" Hex Hydraulic Driver K42AAmjad AlQasrawi100% (1)

- BOQ - Hearts & Arrows Office 04sep2023Document15 pagesBOQ - Hearts & Arrows Office 04sep2023ChristianNo ratings yet

- Cyber Security 2017Document8 pagesCyber Security 2017Anonymous i1ClcyNo ratings yet

- 4 TheEulerianFunctions - 000 PDFDocument16 pages4 TheEulerianFunctions - 000 PDFShorouk Al- IssaNo ratings yet

- Internal Peripherals of Avr McusDocument2 pagesInternal Peripherals of Avr McusKuldeep JashanNo ratings yet

- Vincent Ira B. Perez: Barangay Gulod, Calatagan, BatangasDocument3 pagesVincent Ira B. Perez: Barangay Gulod, Calatagan, BatangasJohn Ramsel Boter IINo ratings yet

- Class 7thDocument24 pagesClass 7thPriyaNo ratings yet

- Soal Kelas 4 IIDocument5 pagesSoal Kelas 4 IIes tougeNo ratings yet

- Act 1&2 and SAQ No - LawDocument4 pagesAct 1&2 and SAQ No - LawBududut BurnikNo ratings yet

- 96 Amazing Social Media Statistics and FactsDocument19 pages96 Amazing Social Media Statistics and FactsKatie O'BrienNo ratings yet

- (PDF) Biochemistry and Molecular Biology of Plants: Book DetailsDocument1 page(PDF) Biochemistry and Molecular Biology of Plants: Book DetailsArchana PatraNo ratings yet

- Circuit AnalysisDocument98 pagesCircuit Analysisahtisham shahNo ratings yet

- Proposed Panel Antenna: Globe Telecom ProprietaryDocument2 pagesProposed Panel Antenna: Globe Telecom ProprietaryJason QuibanNo ratings yet

- Quick Reference - HVAC (Part-1) : DECEMBER 1, 2019Document18 pagesQuick Reference - HVAC (Part-1) : DECEMBER 1, 2019shrawan kumarNo ratings yet

- Winkens Et Al 2009Document8 pagesWinkens Et Al 2009Marta SanchezNo ratings yet

- Stellar Structure and EvolutionDocument222 pagesStellar Structure and Evolutionjano71100% (2)

- Liquid Analysis v3 Powell-Cumming 2010 StanfordgwDocument28 pagesLiquid Analysis v3 Powell-Cumming 2010 StanfordgwErfanNo ratings yet

- Organizational Behaviour Group Assignment-2Document4 pagesOrganizational Behaviour Group Assignment-2Prateek KurupNo ratings yet

- Service Positioning and DesignDocument3 pagesService Positioning and DesignSaurabh SinhaNo ratings yet