You might also like

- Investments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsFrom EverandInvestments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsNo ratings yet

- Chapter 4 SDocument17 pagesChapter 4 SLê Đăng Cát NhậtNo ratings yet

- 2.PPT On Intangible AssetsDocument10 pages2.PPT On Intangible AssetsBhuvaneswari karuturiNo ratings yet

- 6) Ias-38Document15 pages6) Ias-38manvi jainNo ratings yet

- Audit of Item of FS Notes by CA Kapil GoyalDocument9 pagesAudit of Item of FS Notes by CA Kapil GoyalAbhimanyu Kumar ranaNo ratings yet

- Week 4 - Intangible AssetsDocument28 pagesWeek 4 - Intangible AssetsJeremy BreggerNo ratings yet

- Intangible Assets Slides - FinalDocument28 pagesIntangible Assets Slides - FinalAbhiNo ratings yet

- PAS 38 Intangible Assets: Lecture AidDocument18 pagesPAS 38 Intangible Assets: Lecture Aidwendy alcosebaNo ratings yet

- Intangible Assets Slides - FinalDocument28 pagesIntangible Assets Slides - FinalKirei MinaNo ratings yet

- Intagible Asset 1 1Document13 pagesIntagible Asset 1 1Trina Rose FandiñoNo ratings yet

- Accounting For Assets, Impairments and GrantsDocument21 pagesAccounting For Assets, Impairments and GrantsSajid Iqbal100% (1)

- Lecture Week 4Document48 pagesLecture Week 4朱潇妤No ratings yet

- Lecture Week 4Document48 pagesLecture Week 4朱潇妤No ratings yet

- Study Session 8 - Long Lived Assets - SharedDocument55 pagesStudy Session 8 - Long Lived Assets - SharedIhuomacumehNo ratings yet

- SBRIAS38 TutorSlidesDocument27 pagesSBRIAS38 TutorSlidesDipesh MagratiNo ratings yet

- Audit of Intangible AssetsDocument8 pagesAudit of Intangible AssetsMikaela Graciel AnneNo ratings yet

- 10.11 AS 26 Intangible AssetsDocument5 pages10.11 AS 26 Intangible AssetsAnakin SkywalkerNo ratings yet

- Intangible Assets Slides - FinalDocument24 pagesIntangible Assets Slides - FinaldaisyNo ratings yet

- Intangibles: ACC/ACF3100 Advanced Financial AccountingDocument42 pagesIntangibles: ACC/ACF3100 Advanced Financial Accountingharoon nasirNo ratings yet

- 04 Ias 38Document4 pages04 Ias 38Irtiza AbbasNo ratings yet

- Intangible AssetsDocument3 pagesIntangible Assetsgreat angelNo ratings yet

- IAS 38 - Intangible AssetsDocument27 pagesIAS 38 - Intangible AssetsArshad BhuttaNo ratings yet

- Topic 4: Balance Sheet: B/S UsefulnessDocument27 pagesTopic 4: Balance Sheet: B/S UsefulnessabiNo ratings yet

- Handout Fin Man 2305Document7 pagesHandout Fin Man 2305Sheena Gallentes LeysonNo ratings yet

- Intangibles PDFDocument5 pagesIntangibles PDFBryan PiañarNo ratings yet

- CH7-Intangible Assets and Goodwill: HSCS Training & ConsultingDocument2 pagesCH7-Intangible Assets and Goodwill: HSCS Training & ConsultingKhaled SherifNo ratings yet

- Financial Feasibility Study (Theoretical Part) : Q (1) : What Is Meant by Project Economics??Document5 pagesFinancial Feasibility Study (Theoretical Part) : Q (1) : What Is Meant by Project Economics??Mariam YasserNo ratings yet

- Substantive Test of Intangible Assets, Prepaid Expenses (Autosaved)Document38 pagesSubstantive Test of Intangible Assets, Prepaid Expenses (Autosaved)Mej AgaoNo ratings yet

- IAS 38 Intangible Assets 0Document9 pagesIAS 38 Intangible Assets 0Eric Agyenim-BoatengNo ratings yet

- Chapter 11 Intangible AssetsDocument4 pagesChapter 11 Intangible AssetsAngelica Joy ManaoisNo ratings yet

- #23 Intangible Assets (Notes For 6208)Document6 pages#23 Intangible Assets (Notes For 6208)jaysonNo ratings yet

- 22.intangible Assets - 2011-BWDocument24 pages22.intangible Assets - 2011-BWlampug5023No ratings yet

- Chapter 9 - Intangible Asset & Chapter 10 - Impairment of AssetDocument24 pagesChapter 9 - Intangible Asset & Chapter 10 - Impairment of AssetAli JoomunNo ratings yet

- Week 5 - Chapter 4Document45 pagesWeek 5 - Chapter 4AJNo ratings yet

- Module 7 - IAS 38 Intangible Assets Presentation 1st ClassDocument33 pagesModule 7 - IAS 38 Intangible Assets Presentation 1st ClassMartia NongNo ratings yet

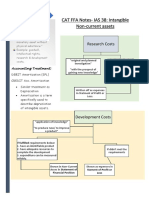

- IAS 38: Intangible NCA: CAT FFA Notes-IAS 38: Intangible Non-Current AssetsDocument1 pageIAS 38: Intangible NCA: CAT FFA Notes-IAS 38: Intangible Non-Current AssetsStargazingNo ratings yet

- 3 Non-Current Assets TopicDocument43 pages3 Non-Current Assets TopicpesseNo ratings yet

- Attempted IntermediatedDocument22 pagesAttempted IntermediatedMAGOMU DAN DAVIDNo ratings yet

- MCS May22 - Aug22 F2 AppliedDocument61 pagesMCS May22 - Aug22 F2 Appliednav7No ratings yet

- Comprehensive CaseDocument39 pagesComprehensive CasePratiwi NingsihNo ratings yet

- Pas 38 - Intangible AssetsDocument21 pagesPas 38 - Intangible AssetsMa. Franceska Loiz T. RiveraNo ratings yet

- Business Valuation: Chapter Learning ObjectivesDocument20 pagesBusiness Valuation: Chapter Learning ObjectivesDINEO PRUDENCE NONGNo ratings yet

- FAC3702 Learning Unit 4 Intangible AssetsDocument5 pagesFAC3702 Learning Unit 4 Intangible Assetssnvywpgq55No ratings yet

- 02 Audit of Mining Entities PDFDocument12 pages02 Audit of Mining Entities PDFelaine piliNo ratings yet

- Intangible AssetDocument38 pagesIntangible AssetRimissha Udenia 2No ratings yet

- Topic 5Document12 pagesTopic 5huongkhue9aNo ratings yet

- 12 Handout 1 Pas 38, Pas 40, and Pfrs 1Document10 pages12 Handout 1 Pas 38, Pas 40, and Pfrs 12DMitchNo ratings yet

- Intangible For Non-Current AssetsDocument55 pagesIntangible For Non-Current AssetsChitta LeeNo ratings yet

- Intangible AssetsDocument6 pagesIntangible AssetsChris tine Mae MendozaNo ratings yet

- Creating Value For ShareholdersDocument8 pagesCreating Value For Shareholders18ITR028 Janaranjan ENo ratings yet

- Intangible AssetsDocument35 pagesIntangible Assetsapi-309065812No ratings yet

- Pocket Reference Card BlankDocument8 pagesPocket Reference Card BlankgoerginamarquezNo ratings yet

- Ias 38 - TSVHDocument37 pagesIas 38 - TSVHHồ Đan ThụcNo ratings yet

- A220 - Midterm RequirementDocument7 pagesA220 - Midterm RequirementDianna Lynn MolinaNo ratings yet

- Introduction To MeDocument30 pagesIntroduction To MeAman SinghNo ratings yet

- Non-Current Asse TS: Session 22Document14 pagesNon-Current Asse TS: Session 22Abdullah EjazNo ratings yet

- SBI Nfo - Baf LeafletDocument4 pagesSBI Nfo - Baf LeafletAvijith ChandramouliNo ratings yet

- Summary Notes in Intangible Assets PDFDocument5 pagesSummary Notes in Intangible Assets PDFJohn Kenneth100% (1)

- 2.2 Intangible Assets Lecture 2 2023Document46 pages2.2 Intangible Assets Lecture 2 2023Karlapotgieter20No ratings yet

- TOPIC 26 IAS 38 Intangible AssetsDocument7 pagesTOPIC 26 IAS 38 Intangible AssetsNameNo ratings yet

- IAS 23 Borrowing CostDocument4 pagesIAS 23 Borrowing CostVikky BehNo ratings yet

- REIN (Preliminaries)Document3 pagesREIN (Preliminaries)Vikky BehNo ratings yet

- Goba Brothers SDN BHDDocument3 pagesGoba Brothers SDN BHDVikky BehNo ratings yet

- CONTACTA (Preliminaries)Document2 pagesCONTACTA (Preliminaries)Vikky BehNo ratings yet

- Audit Supporting Notes - Reference For Exam - Batch 1Document12 pagesAudit Supporting Notes - Reference For Exam - Batch 1Vikky BehNo ratings yet

- Plastictenic SDN BHDDocument2 pagesPlastictenic SDN BHDVikky BehNo ratings yet

- IFRS 2 Share Based PaymentDocument19 pagesIFRS 2 Share Based PaymentVikky BehNo ratings yet

- Law and OrderDocument11 pagesLaw and OrderVikky BehNo ratings yet

- Algebraic FractionsDocument2 pagesAlgebraic FractionsVikky BehNo ratings yet

- ACCA Strategic Business Reporting (SBR) Achievement Ladder Step 4 Questions & AnswersDocument10 pagesACCA Strategic Business Reporting (SBR) Achievement Ladder Step 4 Questions & AnswersAdam MNo ratings yet

- Financial Analysis GlossaryDocument6 pagesFinancial Analysis GlossarySergio OlarteNo ratings yet

- IAS 38 - Intangible AssetsDocument8 pagesIAS 38 - Intangible AssetsEric Agyenim-BoatengNo ratings yet

- Ifrs 6Document4 pagesIfrs 6Bill LiNo ratings yet

- Ias 38 QuestionsDocument5 pagesIas 38 QuestionsFrank AlexanderNo ratings yet

- FA - FFA Syllabus and Study Guide 2020-21 FINAL PDFDocument17 pagesFA - FFA Syllabus and Study Guide 2020-21 FINAL PDFShah SujitNo ratings yet

- Elpl 2009 10Document43 pagesElpl 2009 10kareem_nNo ratings yet

- Intangible AssetsDocument87 pagesIntangible AssetsNoor fatimaNo ratings yet

- US GAAP Vs IFRS TelecommDocument52 pagesUS GAAP Vs IFRS Telecommludin00100% (1)

- Warmth Home Comfort Case Analysis RoleDocument3 pagesWarmth Home Comfort Case Analysis RolexsnoweyxNo ratings yet

- Solution Manual For International Accounting 5th DoupnikDocument28 pagesSolution Manual For International Accounting 5th DoupnikChristopherCollinsifwq100% (43)

- Bsa 2101 Cfas Finals PDFDocument11 pagesBsa 2101 Cfas Finals PDF수지No ratings yet

- Ia Test Bank 20 PGDocument20 pagesIa Test Bank 20 PGzee abadillaNo ratings yet

- IFA-I Assignment PDFDocument3 pagesIFA-I Assignment PDFNatnael AsfawNo ratings yet

- Interview Related QuestionsDocument8 pagesInterview Related QuestionsAnshita GargNo ratings yet

- 6941 - Multiple Choice - SMEsDocument5 pages6941 - Multiple Choice - SMEsAljur Salameda0% (3)

- Solution Manual CH 08 FInancial Accounting Reporting and Analyzing Long-Term AssetsDocument54 pagesSolution Manual CH 08 FInancial Accounting Reporting and Analyzing Long-Term AssetsSherry AstroliaNo ratings yet

- Financial Statement Analysis: K.R. SubramanyamDocument37 pagesFinancial Statement Analysis: K.R. Subramanyamtiex hereNo ratings yet

- Amazon V IRS - IRS Opening BriefDocument143 pagesAmazon V IRS - IRS Opening BriefDaniel BallardNo ratings yet

- Equity Research Report - Dabur India LimitedDocument7 pagesEquity Research Report - Dabur India LimitedShubhamShekharSinhaNo ratings yet

- FRS 102 Intangible AssetsDocument3 pagesFRS 102 Intangible AssetsRabia UmerNo ratings yet

- Advanced Accounting: Business CombinationsDocument42 pagesAdvanced Accounting: Business Combinations19-Geby Agnes LG100% (1)

- Module 12 PAS 36Document6 pagesModule 12 PAS 36Jan JanNo ratings yet

- Quiz 1 Finals BSA2102 With SolutionDocument6 pagesQuiz 1 Finals BSA2102 With SolutionJohn ryan Del RosarioNo ratings yet

- CH 12Document56 pagesCH 12julietNo ratings yet

- The Procter & Gamble Company Consolidated Statements of EarningsDocument5 pagesThe Procter & Gamble Company Consolidated Statements of EarningsJustine Maureen AndalNo ratings yet

- Business Combination Statutory Mergers and Statutory Consolidations Theories PDF FreeDocument22 pagesBusiness Combination Statutory Mergers and Statutory Consolidations Theories PDF FreerogealynNo ratings yet

- The Institute of Chartered Accountants of PakistanDocument3 pagesThe Institute of Chartered Accountants of PakistanFaizan KhanNo ratings yet

- D16 DipIFR Answers PDFDocument8 pagesD16 DipIFR Answers PDFAnonymous QtUcPzCANo ratings yet

- Chapter 7: Audit of Intangibles and Other Assets: Internal Control Over IntangiblesDocument28 pagesChapter 7: Audit of Intangibles and Other Assets: Internal Control Over IntangiblesUn knownNo ratings yet