You might also like

- Admiralty Law for the Maritime ProfessionalFrom EverandAdmiralty Law for the Maritime ProfessionalRating: 1 out of 5 stars1/5 (1)

- Shipping Practice - With a Consideration of the Law Relating TheretoFrom EverandShipping Practice - With a Consideration of the Law Relating TheretoNo ratings yet

- Limited liability of shipowners for cargo loss upon total loss of vesselDocument4 pagesLimited liability of shipowners for cargo loss upon total loss of vesselNFNLNo ratings yet

- CasesDocument10 pagesCasesJhay Jhay Tugade AquinoNo ratings yet

- Chua Yek Hong Vs IacDocument3 pagesChua Yek Hong Vs IacAnonymous geq9k8oQyONo ratings yet

- Optional AssignmentDocument183 pagesOptional AssignmentJim ClarkNo ratings yet

- Aboitiz Shipping Corporation vs. Court of AppealsDocument20 pagesAboitiz Shipping Corporation vs. Court of AppealsAilein GraceNo ratings yet

- Chua Yek Hong vs. IACDocument2 pagesChua Yek Hong vs. IACMae Navarra100% (4)

- Compilation of Case Digests - Admiralty - SecbDocument148 pagesCompilation of Case Digests - Admiralty - SecbMitchi Jerez100% (2)

- Chua Yek Hong vs. Intermediate Appellate Court (1988)Document1 pageChua Yek Hong vs. Intermediate Appellate Court (1988)Teff QuibodNo ratings yet

- Transpo Cases Chapter 1Document196 pagesTranspo Cases Chapter 1AngelicaAldayMacasadiaNo ratings yet

- Francisco D. Estrada For Petitioner. Purita Hontanosas-Cortes For Private RespondentsDocument3 pagesFrancisco D. Estrada For Petitioner. Purita Hontanosas-Cortes For Private RespondentsJose Ramir LayeseNo ratings yet

- 7.aboitiz Shipping Corporation V New IndiaDocument4 pages7.aboitiz Shipping Corporation V New IndiaKeangela LouiseNo ratings yet

- Transpo - Chua Yek Hong v. IacDocument2 pagesTranspo - Chua Yek Hong v. IacJulius Geoffrey TangonanNo ratings yet

- 133229-1988-Chua Yek Hong v. Intermediate Appellate CourtDocument6 pages133229-1988-Chua Yek Hong v. Intermediate Appellate CourtKrizel BianoNo ratings yet

- Aboitiz Shipping Corporation Vs New India Assurance Company, LTD. - GR 156978 - May 2, 2006Document4 pagesAboitiz Shipping Corporation Vs New India Assurance Company, LTD. - GR 156978 - May 2, 2006juillien isiderioNo ratings yet

- Chua Yek Hong Vs IacDocument2 pagesChua Yek Hong Vs IacERWINLAV2000No ratings yet

- 01&94. Chua Yek Hong v. IAC, GR 74811Document3 pages01&94. Chua Yek Hong v. IAC, GR 74811Austin Viel Lagman MedinaNo ratings yet

- Maritime Agencies & Services, Inc.,Vs. Court of AppealsDocument3 pagesMaritime Agencies & Services, Inc.,Vs. Court of AppealsMa. Princess CongzonNo ratings yet

- Chua Yek Hong Vs IACDocument2 pagesChua Yek Hong Vs IACmei atienzaNo ratings yet

- Supreme Court: Francisco D. Estrada For Petitioner. Purita Hontanosas-Cortes For Private RespondentsDocument69 pagesSupreme Court: Francisco D. Estrada For Petitioner. Purita Hontanosas-Cortes For Private Respondentsthree_peaceNo ratings yet

- Majeure. It Was Also Elevated To SC and Was Sustained. Hence, Court Needs To Reconcile TheDocument6 pagesMajeure. It Was Also Elevated To SC and Was Sustained. Hence, Court Needs To Reconcile TheI.G. Mingo MulaNo ratings yet

- Aboitiz Shipping v. New India AssuranceDocument1 pageAboitiz Shipping v. New India AssuranceConie Novela100% (1)

- Case Digest TranspoDocument8 pagesCase Digest TranspoBryan Nartatez BautistaNo ratings yet

- Digest - Monarch Insurance Co., Et - Al. vs. CADocument2 pagesDigest - Monarch Insurance Co., Et - Al. vs. CAPaul Vincent Cunanan100% (2)

- Singa Ship Management Phils Vs NLRCDocument34 pagesSinga Ship Management Phils Vs NLRCRhows BuergoNo ratings yet

- Aboitiz Shipping Vs General Accident Fire and Life AssuranceDocument3 pagesAboitiz Shipping Vs General Accident Fire and Life AssuranceGlenn Rey D. AninoNo ratings yet

- Court Rules on Cargo Shipping Dispute Involving Shortlanded Bags of UreaDocument7 pagesCourt Rules on Cargo Shipping Dispute Involving Shortlanded Bags of UreaAndrei Anne PalomarNo ratings yet

- IV Transpo Digests CharterDocument57 pagesIV Transpo Digests CharterPJ SLSRNo ratings yet

- Roque Vs IacDocument6 pagesRoque Vs IacRhei BarbaNo ratings yet

- Lastimoso v. DolienteDocument3 pagesLastimoso v. DolienteMikkaEllaAncla100% (1)

- Sinking of M/V P. Aboitiz ship discussed in Supreme Court rulingDocument7 pagesSinking of M/V P. Aboitiz ship discussed in Supreme Court rulingmyreen reginioNo ratings yet

- Transpo Week 15 Cases-1Document148 pagesTranspo Week 15 Cases-1ColBenjaminAsiddaoNo ratings yet

- Eastern Shipping Lines vs. Court of Appeals ruling on carrier liabilityDocument60 pagesEastern Shipping Lines vs. Court of Appeals ruling on carrier liabilityAngelica Joyce DyNo ratings yet

- 4th Set Digests FINALDocument15 pages4th Set Digests FINALLouiegie Thomas San JuanNo ratings yet

- 3 - Aboitiz v. General Accident, GR No. 100446Document1 page3 - Aboitiz v. General Accident, GR No. 100446Juvial Guevarra BostonNo ratings yet

- Court rules negligence voids limited liabilityDocument2 pagesCourt rules negligence voids limited liabilityZazaNo ratings yet

- Maritime LawDocument11 pagesMaritime LawMALALA MALALANo ratings yet

- La Razon Social vs. Union Insurance Society of Canton G.R. No. 13983 Sept. 1, 1919Document6 pagesLa Razon Social vs. Union Insurance Society of Canton G.R. No. 13983 Sept. 1, 1919JayNo ratings yet

- Transpo Case DigestsDocument5 pagesTranspo Case DigestsChelzea ObarNo ratings yet

- Roque v. IAC, G.R. No. L 66935, Nov. 11, 1985Document9 pagesRoque v. IAC, G.R. No. L 66935, Nov. 11, 1985Kharol EdeaNo ratings yet

- Diligence - QuintosDocument37 pagesDiligence - QuintosCharlene Joy Bumarlong QuintosNo ratings yet

- Second Division G.R. No. 74811, September 30, 1988: Supreme Court of The PhilippinesDocument5 pagesSecond Division G.R. No. 74811, September 30, 1988: Supreme Court of The PhilippinesBiancaDiwaraNo ratings yet

- Magsaysay Vs AganDocument3 pagesMagsaysay Vs AganAnonymous geq9k8oQyONo ratings yet

- 5 Aboitiz Shipping Corporation Vs General Accident Fire and Life Assurance CorporationDocument3 pages5 Aboitiz Shipping Corporation Vs General Accident Fire and Life Assurance Corporationmei atienzaNo ratings yet

- Aboitiz Shipping v. General Accident Fire and Life Assurance Corporation Ltd.Document3 pagesAboitiz Shipping v. General Accident Fire and Life Assurance Corporation Ltd.Mitchi Barranco100% (1)

- 04 - Roque Vs IACDocument7 pages04 - Roque Vs IACthelawanditscomplexitiesNo ratings yet

- Loadstar Shipping Co., Inc. vs. Court of Appeals (1999)Document14 pagesLoadstar Shipping Co., Inc. vs. Court of Appeals (1999)Angelette BulacanNo ratings yet

- Eastern Shipping Lines, Inc. v. IAC, G.R. No. L-69044 and L-71478, May 29, 1987, 150 SCRA 463Document11 pagesEastern Shipping Lines, Inc. v. IAC, G.R. No. L-69044 and L-71478, May 29, 1987, 150 SCRA 463Melle EscaroNo ratings yet

- Aboitiz Shipping Corp. v. General Accident Fire and Life Assurance Corp., LTDDocument2 pagesAboitiz Shipping Corp. v. General Accident Fire and Life Assurance Corp., LTDsophiaNo ratings yet

- Insurance CasesDocument4 pagesInsurance CasesJillen SuanNo ratings yet

- Eastern Shipping Lines Inc Vs Nisshin Fire & Marine InsuranceDocument10 pagesEastern Shipping Lines Inc Vs Nisshin Fire & Marine InsurancemcsumpayNo ratings yet

- Eastern ShippingDocument10 pagesEastern ShippingAlyssa Mae BasalloNo ratings yet

- Transportation Law NotesDocument13 pagesTransportation Law Notesmaricar_rocaNo ratings yet

- EASTERN SHIPPING LINES, INC. vs. INTERMEDIATE APPELLATE COURTDocument3 pagesEASTERN SHIPPING LINES, INC. vs. INTERMEDIATE APPELLATE COURTlouis jansenNo ratings yet

- Warranty of Seaworthiness in Marine Cargo InsuranceDocument2 pagesWarranty of Seaworthiness in Marine Cargo InsuranceRoger Pascual CuaresmaNo ratings yet

- Transportation Cases Set 2Document86 pagesTransportation Cases Set 2Ber Sib JosNo ratings yet

- Monarch Insurance Co Inc. v. CADocument6 pagesMonarch Insurance Co Inc. v. CAMikee Rañola100% (1)

- United States Court of Appeals, Fifth CircuitDocument11 pagesUnited States Court of Appeals, Fifth CircuitScribd Government DocsNo ratings yet

- Loadstar Shipping Co Vs Pioneer Asia Insurance - G.R. No. 157481. January 24, 2006Document5 pagesLoadstar Shipping Co Vs Pioneer Asia Insurance - G.R. No. 157481. January 24, 2006Ebbe DyNo ratings yet

- Enrique M. Fernando For Petitioner. Dominador D. Dayot For RespondentDocument2 pagesEnrique M. Fernando For Petitioner. Dominador D. Dayot For RespondentJoshua BorresNo ratings yet

- Joshua G. Borres JD 1-C Case ProblemDocument2 pagesJoshua G. Borres JD 1-C Case ProblemJoshua BorresNo ratings yet

- 65 - Rentokil Philippines, Inc. v. SanchezDocument2 pages65 - Rentokil Philippines, Inc. v. SanchezJoshua BorresNo ratings yet

- 71 - Association of Non-Profit Club, Inc. v. BIRDocument2 pages71 - Association of Non-Profit Club, Inc. v. BIRJoshua BorresNo ratings yet

- Executive Order No. 292Document26 pagesExecutive Order No. 292Joshua BorresNo ratings yet

- 37 - Securities and Exchange Commission v. Universal Rightfield Property Holding, Inc.Document3 pages37 - Securities and Exchange Commission v. Universal Rightfield Property Holding, Inc.Joshua BorresNo ratings yet

- 30 - Abella v. Civil Service CommissionDocument2 pages30 - Abella v. Civil Service CommissionJoshua BorresNo ratings yet

- 58 - DLSU v. CADocument3 pages58 - DLSU v. CAJoshua BorresNo ratings yet

- 23 - SEC v. Interport Resources CorporationDocument3 pages23 - SEC v. Interport Resources CorporationJoshua BorresNo ratings yet

- Belgica, Et. Al. vs. Ochoa, Et. Al., G.R. No. 208566Document5 pagesBelgica, Et. Al. vs. Ochoa, Et. Al., G.R. No. 208566Joshua BorresNo ratings yet

- Mactan-Cebu International Airport Authority (MCIAA) v. City of Lapu-Lapu and PacaldoDocument2 pagesMactan-Cebu International Airport Authority (MCIAA) v. City of Lapu-Lapu and PacaldoJoshua Borres100% (1)

- 2 - ABAKADA Vs PurisimaDocument4 pages2 - ABAKADA Vs PurisimaJoshua BorresNo ratings yet

- 4 Lacson-Magallanes v. PanoDocument2 pages4 Lacson-Magallanes v. PanoJoshua BorresNo ratings yet

- 3 AMIN Party-List Group v. Executive SecretaryDocument2 pages3 AMIN Party-List Group v. Executive SecretaryJoshua BorresNo ratings yet

- Belgica, Et. Al. vs. Ochoa, Et. Al., G.R. No. 208566Document5 pagesBelgica, Et. Al. vs. Ochoa, Et. Al., G.R. No. 208566Joshua BorresNo ratings yet

- 3 AMIN Party-List Group v. Executive SecretaryDocument2 pages3 AMIN Party-List Group v. Executive SecretaryJoshua BorresNo ratings yet

- 2 - ABAKADA Vs PurisimaDocument4 pages2 - ABAKADA Vs PurisimaJoshua BorresNo ratings yet

- Phil. Airlines vs. CIR, G.R. No. 198759, July 1, 2013Document8 pagesPhil. Airlines vs. CIR, G.R. No. 198759, July 1, 2013Lou Ann AncaoNo ratings yet

- Coombs Vs CastanedaDocument5 pagesCoombs Vs CastanedaJoshua BorresNo ratings yet

- Supapo Vs de JesusDocument12 pagesSupapo Vs de JesusJoshua BorresNo ratings yet

- PBC Vs CADocument7 pagesPBC Vs CAJoshua BorresNo ratings yet

- Land Dispute Over Naval ReservationDocument11 pagesLand Dispute Over Naval ReservationJennifer ArcadioNo ratings yet

- People vs. MapaDocument2 pagesPeople vs. MapaJoshua De Guzman BorresNo ratings yet

- 8 - PHILAM Vs HEUNG-ADocument3 pages8 - PHILAM Vs HEUNG-AJuvial Guevarra BostonNo ratings yet

- UntitledDocument14 pagesUntitledSanjeet HoraNo ratings yet

- 001 - PPT On BLRC Report1Document51 pages001 - PPT On BLRC Report1Ganesan RamanNo ratings yet

- 8 Alvin Patrimonio v. GutierrezDocument18 pages8 Alvin Patrimonio v. GutierrezChristiaan CastilloNo ratings yet

- Different Kinds of ObligationsDocument3 pagesDifferent Kinds of ObligationsmirayNo ratings yet

- ArgumentsDocument5 pagesArgumentsJajoria Vk50% (2)

- Case List 2 MBTC Vs Pascual, GR #163744, 29 Feb 2008Document2 pagesCase List 2 MBTC Vs Pascual, GR #163744, 29 Feb 2008Loren Delos SantosNo ratings yet

- CommercialDocument77 pagesCommercialGNo ratings yet

- Jurisdiction DisputeDocument2 pagesJurisdiction DisputeAnna L. Ilagan-MalipolNo ratings yet

- To sell agricultural land in the PhilippinesDocument3 pagesTo sell agricultural land in the PhilippinesHarrison RigorNo ratings yet

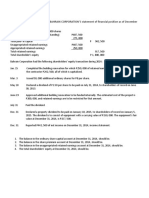

- The Shareholder's Equity Section BAHRAIN CORPORATION'S Statement of Financial Position As of December 31, 2013, Is As FollowsDocument4 pagesThe Shareholder's Equity Section BAHRAIN CORPORATION'S Statement of Financial Position As of December 31, 2013, Is As FollowsCyril John ReyesNo ratings yet

- Importance of DomicileDocument4 pagesImportance of DomicileJunneKhooNo ratings yet

- Law on Obligations and Contracts NotesDocument22 pagesLaw on Obligations and Contracts NotesLuhenNo ratings yet

- The Negotiable Instruments LawDocument15 pagesThe Negotiable Instruments LawGhatz CondaNo ratings yet

- Prescription Period for Obligations Created by LawDocument1 pagePrescription Period for Obligations Created by LawAlvin-Evelyn GuloyNo ratings yet

- FM Shah AliDocument2 pagesFM Shah AliJohn SnowNo ratings yet

- ABS CBN Vs CADocument1 pageABS CBN Vs CACamañanÍvyNo ratings yet

- The Concept of Partition Under Hindu Law With Special Reference To Dayabhaga and Mitakshara Schools of Hindu LawDocument15 pagesThe Concept of Partition Under Hindu Law With Special Reference To Dayabhaga and Mitakshara Schools of Hindu LawRadz RexaNo ratings yet

- Haumschild v. Continental Casualty CoDocument1 pageHaumschild v. Continental Casualty CoKaren Selina AquinoNo ratings yet

- TANGUILIG v. CA - Windmill Contract Dispute ResolvedDocument2 pagesTANGUILIG v. CA - Windmill Contract Dispute ResolvedNatalia ArmadaNo ratings yet

- Chapter 12 Quiz - Business LawDocument2 pagesChapter 12 Quiz - Business LawRayonneNo ratings yet

- Position Paper On The Transfer of Condominium PropertyDocument2 pagesPosition Paper On The Transfer of Condominium PropertyAl MarvinNo ratings yet

- Obli - Yason Vs ArciagaDocument4 pagesObli - Yason Vs ArciagaSyrine MallorcaNo ratings yet

- Civillaw 2015 EditedDocument98 pagesCivillaw 2015 EditedNadine Diamante100% (1)

- 3-1 國際銷售合約範例下載 (無註解版,可編輯)Document6 pages3-1 國際銷售合約範例下載 (無註解版,可編輯)Felix WuNo ratings yet

- Missionary of Lady of Fatima Sisters Vs AlzonaDocument6 pagesMissionary of Lady of Fatima Sisters Vs AlzonaPAMELA DOLINANo ratings yet

- Shriram Personal Accident Insurance Proposal FormDocument4 pagesShriram Personal Accident Insurance Proposal FormMohamed Ibrahim100% (1)

- Sales and Marketing Consultant AgreementDocument9 pagesSales and Marketing Consultant AgreementeliasNo ratings yet

- SC CaseDocument21 pagesSC CaseRitu Raj KumarNo ratings yet

- Adoption Agreement Release ContractDocument2 pagesAdoption Agreement Release ContractgumNo ratings yet