You might also like

- Subestación José Felix Ribas Subestación José Felix Ribas: BP Ii BP IiDocument2 pagesSubestación José Felix Ribas Subestación José Felix Ribas: BP Ii BP IiailynNo ratings yet

- 6 Ebt120 2 PDFDocument62 pages6 Ebt120 2 PDFfararNo ratings yet

- Road Map For The Near Term Performance of The Economy: 50 South Lasalle Chicago, Illinois 60603Document7 pagesRoad Map For The Near Term Performance of The Economy: 50 South Lasalle Chicago, Illinois 60603International Business TimesNo ratings yet

- Advanced Financial Reporting 1.PDF Nov 2011 1Document12 pagesAdvanced Financial Reporting 1.PDF Nov 2011 1Prof. OBESENo ratings yet

- Sra Note 2103Document12 pagesSra Note 2103Tố NiênNo ratings yet

- (Chnarrrseaiel:, Iipit:1, G1Ndhi VishwavidyalayaDocument4 pages(Chnarrrseaiel:, Iipit:1, G1Ndhi VishwavidyalayaDhananjay SinghNo ratings yet

- Comparative Balance SheetDocument13 pagesComparative Balance SheetMelvin Hann RoyanNo ratings yet

- Peta Jaring AntariksaDocument8 pagesPeta Jaring Antariksaaditya kevinNo ratings yet

- Slo Ddo Cadre Strength CLNPDocument6 pagesSlo Ddo Cadre Strength CLNPDurga Prasad SeerapuNo ratings yet

- ژورنال بررسی ارز روزانهDocument26 pagesژورنال بررسی ارز روزانهMobin ZkrNo ratings yet

- a10 - ͼֽ1210 - ё±±ѕDocument39 pagesa10 - ͼֽ1210 - ё±±ѕAnisa SripianaNo ratings yet

- Allocation of Ice-Lined Vaccine Refrigerators 4Th Quarter 2018Document4 pagesAllocation of Ice-Lined Vaccine Refrigerators 4Th Quarter 2018charmaine gallanoNo ratings yet

- Technical Performance Data: Standard ConditionsDocument1 pageTechnical Performance Data: Standard ConditionsfelipeffcNo ratings yet

- Tybcom - A - Group No. - 5Document10 pagesTybcom - A - Group No. - 5Mnimi SalesNo ratings yet

- HIV Testing Training (M&E Part)Document21 pagesHIV Testing Training (M&E Part)Fikerte ZerihunNo ratings yet

- Stowage Plan (L) Ths2Document1 pageStowage Plan (L) Ths2An BùiNo ratings yet

- 6th Schedule Amended Upto 30.06.2020Document65 pages6th Schedule Amended Upto 30.06.2020PATCO PARCNo ratings yet

- Ratios (Summary) : Ratios (Summary) Current Ratio Quick Ratio Cash RatioDocument42 pagesRatios (Summary) : Ratios (Summary) Current Ratio Quick Ratio Cash RatioГая ЗимрутянNo ratings yet

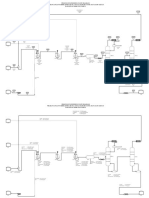

- Process Engineering Flow Diagram Prarancangan Pabrik Kimia Butil Asetat Dari Butanol Dan Asam Asetat Kapasitas 30.000 Ton/TahunDocument2 pagesProcess Engineering Flow Diagram Prarancangan Pabrik Kimia Butil Asetat Dari Butanol Dan Asam Asetat Kapasitas 30.000 Ton/Tahunmuhammad afdalNo ratings yet

- Process Engineering Flow Diagram Prarancangan Pabrik Kimia Butil Asetat Dari Butanol Dan Asam Asetat Kapasitas 30.000 Ton/TahunDocument2 pagesProcess Engineering Flow Diagram Prarancangan Pabrik Kimia Butil Asetat Dari Butanol Dan Asam Asetat Kapasitas 30.000 Ton/Tahunmuhammad afdalNo ratings yet

- Process Engineering Flow Diagram Prarancangan Pabrik Kimia Butil Asetat Dari Butanol Dan Asam Asetat Kapasitas 30.000 Ton/TahunDocument2 pagesProcess Engineering Flow Diagram Prarancangan Pabrik Kimia Butil Asetat Dari Butanol Dan Asam Asetat Kapasitas 30.000 Ton/Tahunmuhammad afdalNo ratings yet

- OTC107201 OptiX OSN 380068008800 Optical Power CalculationDocument40 pagesOTC107201 OptiX OSN 380068008800 Optical Power CalculationSery ArthurNo ratings yet

- Ion Ion: KWH KWH Measurement F1 Measurement F2Document9 pagesIon Ion: KWH KWH Measurement F1 Measurement F2jorge luis ondarcuhuNo ratings yet

- H1 2010 NCM Market Report - Proshare - 020710Document169 pagesH1 2010 NCM Market Report - Proshare - 020710ProshareNo ratings yet

- Wednesday, 11 November 2020 - Afternoon Component 1: Studies in Depth Non-British Study in Depth 1H. The USA: A Nation of Contrasts, 1910-1929Document16 pagesWednesday, 11 November 2020 - Afternoon Component 1: Studies in Depth Non-British Study in Depth 1H. The USA: A Nation of Contrasts, 1910-1929GENUINE 17No ratings yet

- Toyota Financial 2011Document19 pagesToyota Financial 2011Lioubov BodnyaNo ratings yet

- Project 3Document1 pageProject 3MhmdÁbdóNo ratings yet

- Guzelyurt TMY ExtractedDocument366 pagesGuzelyurt TMY ExtractedYazan HarbNo ratings yet

- Adv - MT (Tech) - 2020Document9 pagesAdv - MT (Tech) - 2020bhaihello015No ratings yet

- PTO ToyotaDocument1 pagePTO ToyotaJose Leandro Neves FerreiraNo ratings yet

- TVM Complete TemplateDocument17 pagesTVM Complete TemplateAlok RajNo ratings yet

- QHLV 5 I 45 Am 1 DLK 5504 Kvtyqp 20070504153616Document10 pagesQHLV 5 I 45 Am 1 DLK 5504 Kvtyqp 20070504153616Praveen Balaji K RNo ratings yet

- CT National Report 2Q10Document16 pagesCT National Report 2Q10amy_schenkNo ratings yet

- Schematic1 - Page1Document1 pageSchematic1 - Page1Sarang PurnayeNo ratings yet

- Senate Initialed ResultsDocument10 pagesSenate Initialed ResultsElizabeth BenjaminNo ratings yet

- Financialsummary: Toyota Motor CorporatlonDocument33 pagesFinancialsummary: Toyota Motor Corporatlon007salmanNo ratings yet

- General Mills India Private Limited (CIN: U15510MH1995PTC094741)Document8 pagesGeneral Mills India Private Limited (CIN: U15510MH1995PTC094741)Anshul RanaNo ratings yet

- Time Table JAN 2010Document14 pagesTime Table JAN 2010meabhishek2006No ratings yet

- FY2012 Financial ForecastsDocument12 pagesFY2012 Financial ForecastsdeepflukeNo ratings yet

- BS2011Document39 pagesBS2011mnbvcxzqwerNo ratings yet

- 2011.6.30 HyeDocument81 pages2011.6.30 HyehsdumpNo ratings yet

- SAP T-Code FormDocument1 pageSAP T-Code FormSudarshan DawNo ratings yet

- SAP T-Code FormDocument1 pageSAP T-Code FormSudarshan DawNo ratings yet

- Gantt de Inversion GeneralDocument6 pagesGantt de Inversion GeneralJORGE MACHADONo ratings yet

- 1H F2023 Results Presentation Final 09.03Document39 pages1H F2023 Results Presentation Final 09.03JEAN MICHEL ALONZEAUNo ratings yet

- FRT-TT 4tatet (7.T.) : H4T7/T. / 2022/102 FahitDocument9 pagesFRT-TT 4tatet (7.T.) : H4T7/T. / 2022/102 FahitNAVEEN BAISNo ratings yet

- For Student 15Document15 pagesFor Student 15sunil kumarNo ratings yet

- Portugal, Spain, and The Implications For The Hybrid ModelDocument14 pagesPortugal, Spain, and The Implications For The Hybrid ModelGandhi Jenny Rakeshkumar BD20029No ratings yet

- Process Engineering Flow Diagram Prarancangan Pabrik Kimia Butil Asetat Dari Butanol Dan Asam Asetat Kapasitas 30.000 Ton/TahunDocument2 pagesProcess Engineering Flow Diagram Prarancangan Pabrik Kimia Butil Asetat Dari Butanol Dan Asam Asetat Kapasitas 30.000 Ton/Tahunmuhammad afdalNo ratings yet

- Process Engineering Flow Diagram Prarancangan Pabrik Kimia Butil Asetat Dari Butanol Dan Asam Asetat Kapasitas 30.000 Ton/TahunDocument2 pagesProcess Engineering Flow Diagram Prarancangan Pabrik Kimia Butil Asetat Dari Butanol Dan Asam Asetat Kapasitas 30.000 Ton/Tahunmuhammad afdalNo ratings yet

- General Ledger ORACLEDocument5 pagesGeneral Ledger ORACLEBala RanganathNo ratings yet

- Process Engineering Flow Diagram Prarancangan Pabrik Kimia Butil Asetat Dari Butanol Dan Asam Asetat Kapasitas 30.000 Ton/TahunDocument2 pagesProcess Engineering Flow Diagram Prarancangan Pabrik Kimia Butil Asetat Dari Butanol Dan Asam Asetat Kapasitas 30.000 Ton/Tahunmuhammad afdalNo ratings yet

- Mughal Rule Muslin, Silk Pearl India Pakistan: TH THDocument19 pagesMughal Rule Muslin, Silk Pearl India Pakistan: TH THDigonto DasNo ratings yet

- Corporate PDFDocument16 pagesCorporate PDFRenuka PrasadNo ratings yet

- CD - Non CD Oct-2023Document5 pagesCD - Non CD Oct-2023sureshsaketh17No ratings yet

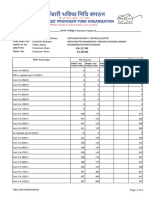

- LNL Iklcqd /: Employee Share Employer Share Employee Share Employer ShareDocument4 pagesLNL Iklcqd /: Employee Share Employer Share Employee Share Employer ShareSayan SarkarNo ratings yet

- Japan's Financial Crisis: Institutional Rigidity and Reluctant ChangeFrom EverandJapan's Financial Crisis: Institutional Rigidity and Reluctant ChangeNo ratings yet

- Ficha Tecnica RV-5000Document6 pagesFicha Tecnica RV-5000Rolando CerezoNo ratings yet

- A5E43455517 6 76 - MANUAL - SITOP Manager - en USDocument252 pagesA5E43455517 6 76 - MANUAL - SITOP Manager - en USdasdNo ratings yet

- Migrant Nurses Ausi Integrative ReviewDocument7 pagesMigrant Nurses Ausi Integrative ReviewBony Yunaria TanuNo ratings yet

- Unit 7 Assessment Guidance 2021-2022Document13 pagesUnit 7 Assessment Guidance 2021-2022JonasNo ratings yet

- A Model Estimating Bike Lane DemandDocument9 pagesA Model Estimating Bike Lane DemandachiruddinNo ratings yet

- Rtu2020 SpecsDocument16 pagesRtu2020 SpecsYuri Caleb Gonzales SanchezNo ratings yet

- Useful Relations in Quantum Field TheoryDocument30 pagesUseful Relations in Quantum Field TheoryDanielGutierrez100% (1)

- What Is Research: Presented By: Anam Nawaz CheemaDocument13 pagesWhat Is Research: Presented By: Anam Nawaz CheemamahiftiNo ratings yet

- L2 AND L3 Switch DifferenceDocument6 pagesL2 AND L3 Switch DifferenceVivek GhateNo ratings yet

- User Manual HP Officejet 8210Document95 pagesUser Manual HP Officejet 8210ponidiNo ratings yet

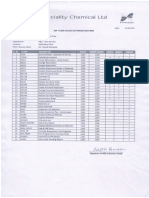

- Test Certificate: CM/L-NO:5530357Document10 pagesTest Certificate: CM/L-NO:5530357TARUNKUMARNo ratings yet

- Introducing The True Ekklesia of Jesus ChristDocument5 pagesIntroducing The True Ekklesia of Jesus ChristRamil Moreno SumangilNo ratings yet

- Assignment Operational BudgetDocument4 pagesAssignment Operational BudgetBona HirkoNo ratings yet

- Google Maps Places Scraper 19 Jul 2022Document16 pagesGoogle Maps Places Scraper 19 Jul 2022K. SanjuNo ratings yet

- Imaginefx How To Draw and Paint Anatomy Volume 2Document116 pagesImaginefx How To Draw and Paint Anatomy Volume 2tofupastaNo ratings yet

- UG190239 - Avaneesh NatarajaDocument21 pagesUG190239 - Avaneesh NatarajaAvaneesh NatarajaNo ratings yet

- Clinical Profile of Patient With Dengue Fever in A Tertiary Care Teaching HospitalDocument4 pagesClinical Profile of Patient With Dengue Fever in A Tertiary Care Teaching HospitalnovtaNo ratings yet

- SrsDocument13 pagesSrsSantoshkumar ShaliNo ratings yet

- The Main Factors Influencing Consumer Behavior Towards Bershka Store in KazakhstanDocument5 pagesThe Main Factors Influencing Consumer Behavior Towards Bershka Store in KazakhstanIJEMR JournalNo ratings yet

- MTH 212 OdeDocument18 pagesMTH 212 OdeJames ojochegbNo ratings yet

- Indo Africa Indianparticipants-09Document870 pagesIndo Africa Indianparticipants-09Guruprasad T JathanNo ratings yet

- CSF1P0Document17 pagesCSF1P0alfbiokNo ratings yet

- CH-8 - Rise of Indian NationalismDocument3 pagesCH-8 - Rise of Indian NationalismdebdulaldamNo ratings yet

- Goal and Scope of PsychotherapyDocument4 pagesGoal and Scope of PsychotherapyJasroop Mahal100% (1)

- Goulish, Matthew - 39 Microlectures in Proximity of PerformanceDocument225 pagesGoulish, Matthew - 39 Microlectures in Proximity of PerformanceBen Zucker100% (2)

- Quantum Mechanics The Key To Understanding MagnetismDocument17 pagesQuantum Mechanics The Key To Understanding Magnetismnicusor.iacob5680No ratings yet

- PMP Lite Mock Exam 2 QuestionsDocument16 pagesPMP Lite Mock Exam 2 QuestionsJobin John100% (1)

- NOAH STANTON - 3.1.3 and 3.1.4 Creating Graphs and Finding SolutionsDocument7 pagesNOAH STANTON - 3.1.3 and 3.1.4 Creating Graphs and Finding SolutionsSora PhantomhiveNo ratings yet

- Oil Shows Description: (I) Sample Under Microscope (Under White Light)Document1 pageOil Shows Description: (I) Sample Under Microscope (Under White Light)deyaa SadoonNo ratings yet

- Most Underrated Skills That'll Make You A Rockstar in The Staffing Agency IndustryDocument2 pagesMost Underrated Skills That'll Make You A Rockstar in The Staffing Agency Industrygalairae40100% (1)