You might also like

- New Jersey Complete Business Registration PacketDocument47 pagesNew Jersey Complete Business Registration PacketWen' George BeyNo ratings yet

- Tax Sales for Rookies: A Beginner’s Guide to Understanding Property Tax SalesFrom EverandTax Sales for Rookies: A Beginner’s Guide to Understanding Property Tax SalesNo ratings yet

- VatDocument274 pagesVatzaneNo ratings yet

- Value Added TaxationDocument76 pagesValue Added Taxationxz wyNo ratings yet

- Tax 2Document14 pagesTax 2Nash Ortiz LuisNo ratings yet

- Sales Tax GuideDocument6 pagesSales Tax GuideakhileshkantNo ratings yet

- E595E Tax Exempt FormDocument4 pagesE595E Tax Exempt FormstockfaceNo ratings yet

- Financial Reporting (FR) : Practice & Revision KitDocument396 pagesFinancial Reporting (FR) : Practice & Revision KitSanket Barai100% (4)

- Tax Vat Week4Document73 pagesTax Vat Week4Neil FrangilimanNo ratings yet

- Comprehensive VAT TAXATION (3!31!14)Document166 pagesComprehensive VAT TAXATION (3!31!14)dereckriveraNo ratings yet

- VAT - GuidenotesDocument14 pagesVAT - GuidenotesNardz AndananNo ratings yet

- Tax - Vat GuidenotesDocument13 pagesTax - Vat GuidenotesNardz AndananNo ratings yet

- NJ Sales and Use Tax Guide Su4Document26 pagesNJ Sales and Use Tax Guide Su4kylebassettNo ratings yet

- GNotes2 VAT 2018 With TRAIN AmendmentsDocument31 pagesGNotes2 VAT 2018 With TRAIN AmendmentsKristine Bucu100% (4)

- Commissioner of Internal Revenue vs. Seagate Technology (Philippines), 451 SCRA 132, February 11, 2005Document2 pagesCommissioner of Internal Revenue vs. Seagate Technology (Philippines), 451 SCRA 132, February 11, 2005idolbondocNo ratings yet

- Tax 2 Notes Finals 4Document36 pagesTax 2 Notes Finals 4Boom ManuelNo ratings yet

- Notes On VATDocument15 pagesNotes On VATErnest Benz Sabella DavilaNo ratings yet

- A Guide To Rotational Molding 5717Document16 pagesA Guide To Rotational Molding 5717EngineeringTopChannelNo ratings yet

- CIR vs. Seagate Technology (Phils)Document1 pageCIR vs. Seagate Technology (Phils)kaira marie carlosNo ratings yet

- Screenshot 2023-09-03 at 10.02.47 PMDocument8 pagesScreenshot 2023-09-03 at 10.02.47 PMgajiparaalpeshNo ratings yet

- Vat Tax CasesDocument24 pagesVat Tax CasesEller-JedManalacMendozaNo ratings yet

- 2019 Taxation Law Bar Q and ADocument12 pages2019 Taxation Law Bar Q and AKasurog CopsNo ratings yet

- Xebia Test ResultDocument16 pagesXebia Test ResultBalbhim ThoratNo ratings yet

- St120 Fill inDocument2 pagesSt120 Fill inUber NewNo ratings yet

- New Jersey Sales Tax Guide: ImportantDocument33 pagesNew Jersey Sales Tax Guide: ImportantGanda PrajaNo ratings yet

- Resale Certificate: Purchaser InformationDocument2 pagesResale Certificate: Purchaser InformationGlendaNo ratings yet

- Resale CertificateDocument2 pagesResale CertificateRobertaVasconcelosNo ratings yet

- WV TEC InstructionsDocument4 pagesWV TEC InstructionsnareshkumharNo ratings yet

- General Resale Certificate FormDocument2 pagesGeneral Resale Certificate Formm4r4nzn0No ratings yet

- Resale Certificate: Purchaser InformationDocument2 pagesResale Certificate: Purchaser InformationjesbmnNo ratings yet

- Kansas PLR, P-2011-008 (Kan DOR Sept. 22, 2011)Document2 pagesKansas PLR, P-2011-008 (Kan DOR Sept. 22, 2011)Paul MastersNo ratings yet

- Valid Tax InvoiceDocument3 pagesValid Tax InvoicenadiadubuqueNo ratings yet

- Reseller CertificateDocument2 pagesReseller CertificateKatherine KilcullenNo ratings yet

- Sales TaxDocument52 pagesSales TaxSavan DesaiNo ratings yet

- NJ Exemption CertificatesDocument19 pagesNJ Exemption CertificatesKeith LeeNo ratings yet

- Taxn03b Vat IntroDocument20 pagesTaxn03b Vat IntroTrishamae legaspiNo ratings yet

- Central Sales TaxDocument3 pagesCentral Sales TaxRahul JainNo ratings yet

- Module 3 Donor's Tax and Business Tax (Part 2)Document32 pagesModule 3 Donor's Tax and Business Tax (Part 2)Venice Marie ArroyoNo ratings yet

- New Jersey Tax Guide: Buying or Selling A Home in New JerseyDocument9 pagesNew Jersey Tax Guide: Buying or Selling A Home in New Jerseynour abdallaNo ratings yet

- 1 Basics of Value Added TaxDocument58 pages1 Basics of Value Added TaxHazel Andrea Garduque LopezNo ratings yet

- Close or End A BusinessDocument2 pagesClose or End A BusinessquellopNo ratings yet

- CIR v. Seagate Technology PhilsDocument6 pagesCIR v. Seagate Technology PhilsL.A. ManlangitNo ratings yet

- NYS Resale CertificateDocument1 pageNYS Resale CertificateVanessa HernandezNo ratings yet

- Debit Note & Credit NoteDocument9 pagesDebit Note & Credit NoteconciliataxesNo ratings yet

- Tax Goods: of Excise or A Special Tax) Is CommonlyDocument6 pagesTax Goods: of Excise or A Special Tax) Is Commonlyrachit2383No ratings yet

- Characteristic of Vat-Business TaxationDocument8 pagesCharacteristic of Vat-Business TaxationAthena LouiseNo ratings yet

- Axation Law Bar Examination 2019 QuestionsDocument14 pagesAxation Law Bar Examination 2019 QuestionslexNo ratings yet

- TAXATIONDocument2 pagesTAXATIONsarahjanemontalban26No ratings yet

- Business and Tax Laws: INC Guntur Puttu Guru PrasadDocument28 pagesBusiness and Tax Laws: INC Guntur Puttu Guru PrasadPUTTU GURU PRASAD SENGUNTHA MUDALIARNo ratings yet

- VAT ReportDocument32 pagesVAT ReportNoel Christopher G. BellezaNo ratings yet

- SteelfixerDocument15 pagesSteelfixerJohn Albert BaltazarNo ratings yet

- Charging VAT: For A Full List of Exempt Goods and Services Please Click On This LinkDocument4 pagesCharging VAT: For A Full List of Exempt Goods and Services Please Click On This LinkZita BerniceNo ratings yet

- October 12,: Vat Zero-Rated Sale of Service (Labor Aspect)Document6 pagesOctober 12,: Vat Zero-Rated Sale of Service (Labor Aspect)LaBron JamesNo ratings yet

- Assignmnet No:01 Sales TaxDocument3 pagesAssignmnet No:01 Sales TaxFatima TurkNo ratings yet

- D. VAT Registration and Compliance Requirements FinalDocument34 pagesD. VAT Registration and Compliance Requirements FinalNatalie SerranoNo ratings yet

- 8VATDocument70 pages8VATNoelNo ratings yet

- CIR Vs Seagate Technology PhilippinesDocument2 pagesCIR Vs Seagate Technology Philippineskaira marie carlosNo ratings yet

- GST Sem Material PDFDocument6 pagesGST Sem Material PDFObaid AhmedNo ratings yet

- 1 Understanding VAT For BusinessesDocument6 pages1 Understanding VAT For BusinessesBensonNo ratings yet

- Q. What Is Value Added Tax (VAT) ?Document8 pagesQ. What Is Value Added Tax (VAT) ?Akhilesh SinghNo ratings yet

- VAT Concepts Tax 321Document28 pagesVAT Concepts Tax 321justineNo ratings yet

- RESEARCH - DOF Directive To BIR On Tax Leakage From Online SellersDocument10 pagesRESEARCH - DOF Directive To BIR On Tax Leakage From Online SellersKrizia ReamicoNo ratings yet

- TaxationDocument38 pagesTaxationEphraim LopezNo ratings yet

- BCD001 Standard Purchase Costs DisclosureDocument4 pagesBCD001 Standard Purchase Costs DisclosureConveyancers DirectoryNo ratings yet

- MBBS CourseDocument2 pagesMBBS CourseNagaraja SNo ratings yet

- Cultivation of HerbsDocument38 pagesCultivation of HerbsNagaraja SNo ratings yet

- Admission January2022Document1 pageAdmission January2022Nagaraja SNo ratings yet

- User Manual DomesticDocument8 pagesUser Manual DomesticNagaraja SNo ratings yet

- 11 An Economic Analysis of MSMEs-2343197Document5 pages11 An Economic Analysis of MSMEs-2343197palak GuptaNo ratings yet

- Newspapers Listed in Emigrate S. No. List of NewspapersDocument1 pageNewspapers Listed in Emigrate S. No. List of NewspapersMohammedNo ratings yet

- List of Applications For The Post of Office Assistant - 0Document236 pagesList of Applications For The Post of Office Assistant - 0Nagaraja SNo ratings yet

- How Does Tiic Help First Generation EntrepreneursDocument5 pagesHow Does Tiic Help First Generation EntrepreneursNagaraja SNo ratings yet

- Mortgageloanorig Licensee Download 01012018Document724 pagesMortgageloanorig Licensee Download 01012018Nagaraja SNo ratings yet

- SCGC Brochure Roto Molding CompressedDocument8 pagesSCGC Brochure Roto Molding CompressedNagaraja SNo ratings yet

- Sales and Use Taxes New JerseyDocument21 pagesSales and Use Taxes New JerseyNagaraja SNo ratings yet

- How To Apply For Loan Through TiicDocument2 pagesHow To Apply For Loan Through TiicNagaraja SNo ratings yet

- Chinese Companies On US Stock ExchangesDocument19 pagesChinese Companies On US Stock ExchangesNagaraja SNo ratings yet

- Page Attachments NCUSCR 2020 Annual ReportDocument13 pagesPage Attachments NCUSCR 2020 Annual ReportNagaraja SNo ratings yet

- SolvixSkillDevelopment List CompaniesDocument10 pagesSolvixSkillDevelopment List CompaniesNagaraja SNo ratings yet

- Scrip List 111418Document6 pagesScrip List 111418Nagaraja SNo ratings yet

- Su 4Document31 pagesSu 4Nagaraja SNo ratings yet

- IndustryviidaysDocument2 pagesIndustryviidaysNagaraja SNo ratings yet

- ROHS Reach SVHC Statement 2017Document1 pageROHS Reach SVHC Statement 2017Nagaraja SNo ratings yet

- NJFPA Member List As of 5 - 15 - 2022Document2 pagesNJFPA Member List As of 5 - 15 - 2022Nagaraja SNo ratings yet

- Terms and ConditionsDocument35 pagesTerms and ConditionsNagaraja SNo ratings yet

- FarmingsalesandusetaxguideDocument26 pagesFarmingsalesandusetaxguideNagaraja SNo ratings yet

- Vacancy AdvertisementDocument2 pagesVacancy AdvertisementNagaraja SNo ratings yet

- Modular Switches: List Price W.E.F. 9 Dec. 2019Document8 pagesModular Switches: List Price W.E.F. 9 Dec. 2019Nagaraja SNo ratings yet

- Charity UsaDocument226 pagesCharity UsaNagaraja SNo ratings yet

- Service Connection Within 15 Days For Industry Up To 112 KW: Connecting With ConfidenceDocument5 pagesService Connection Within 15 Days For Industry Up To 112 KW: Connecting With ConfidenceNagaraja SNo ratings yet

- MOB HBT THEFT Arrest Accu-May - 2018Document321 pagesMOB HBT THEFT Arrest Accu-May - 2018Nagaraja SNo ratings yet

- Web DesignDocument492 pagesWeb DesignNagaraja SNo ratings yet

- Ctu 351 (Uitm)Document18 pagesCtu 351 (Uitm)afinaramziNo ratings yet

- Cash BudgetDocument8 pagesCash BudgetKei CambaNo ratings yet

- Rap Exam Question Paper Model 2Document28 pagesRap Exam Question Paper Model 2Hemant Dhande40% (10)

- Lampurginni (MGT 337)Document3 pagesLampurginni (MGT 337)Nasrullah Khan AbidNo ratings yet

- Gantt ChartDocument4 pagesGantt ChartJones PetersonNo ratings yet

- CIRIA Report PR62 - Fundamental Basis of Grout Injection For Ground TreatmentDocument58 pagesCIRIA Report PR62 - Fundamental Basis of Grout Injection For Ground TreatmentCJODoNo ratings yet

- Foreign Trade 4Document2 pagesForeign Trade 4Reyansh VermaNo ratings yet

- 206131-2017-Metropolitan Bank and Trust Co. v. Liberty20211014-12-CgooftDocument18 pages206131-2017-Metropolitan Bank and Trust Co. v. Liberty20211014-12-CgooftKobe Lawrence VeneracionNo ratings yet

- Delgado VS Alonso 44 Phil 739Document4 pagesDelgado VS Alonso 44 Phil 739kreistil weeNo ratings yet

- Akzonobel Report15 Entire, 146Document266 pagesAkzonobel Report15 Entire, 146jasper laarmansNo ratings yet

- Open Banking: Global State of PlayDocument16 pagesOpen Banking: Global State of PlayaldykurniawanNo ratings yet

- BC Question PaperDocument4 pagesBC Question PaperVVNA BhargaviNo ratings yet

- Damodaram Sanjivayya Sabbavaram, Visakhapatnam, Ap., India.: National Law UniversityDocument17 pagesDamodaram Sanjivayya Sabbavaram, Visakhapatnam, Ap., India.: National Law UniversityJahnavi GopaluniNo ratings yet

- Padma Multipurpose BridgeDocument10 pagesPadma Multipurpose BridgeMD. Mahamudul HasanNo ratings yet

- 01 PRMGT - Assignment Question Marking SchemeDocument6 pages01 PRMGT - Assignment Question Marking SchemeMichael TamNo ratings yet

- CESAB P200 1.4 - 2.5 Tonne Powered Pallet TruckDocument8 pagesCESAB P200 1.4 - 2.5 Tonne Powered Pallet TruckLinh NguyenNo ratings yet

- SimhaDocument14 pagesSimhaArunachalam ANo ratings yet

- Soal Dan Jawaban Tugas Lab 1 - Home Office and Branch OfficeDocument6 pagesSoal Dan Jawaban Tugas Lab 1 - Home Office and Branch OfficePUTRI YANINo ratings yet

- Approved Contractors .AjmanDocument22 pagesApproved Contractors .AjmanSahal AnsarNo ratings yet

- Ca Final: Paper 8: Indirect Tax LawsDocument499 pagesCa Final: Paper 8: Indirect Tax LawsMaroju Rajitha100% (1)

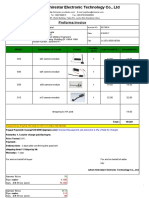

- Shenzhen Shirestar Electronic Technology Co., LTD: Proforma InvoiceDocument3 pagesShenzhen Shirestar Electronic Technology Co., LTD: Proforma InvoicepintoNo ratings yet

- CrisisDocument6 pagesCrisishabibi 101No ratings yet

- Moto BillDocument1 pageMoto Billmyyes3994No ratings yet

- Influence of Social Sciences On Buyer BehaviorDocument5 pagesInfluence of Social Sciences On Buyer BehaviorRavindra Reddy ThotaNo ratings yet

- Constitutional Law Primer Bernas-1-258-276Document19 pagesConstitutional Law Primer Bernas-1-258-276Shaira Jean SollanoNo ratings yet

- CRM BCBLDocument60 pagesCRM BCBLHasnat ShakirNo ratings yet

- Wallstreetjournaleurope 20170815 TheWallStreetJournal-EuropeDocument34 pagesWallstreetjournaleurope 20170815 TheWallStreetJournal-EuropestefanoNo ratings yet